|

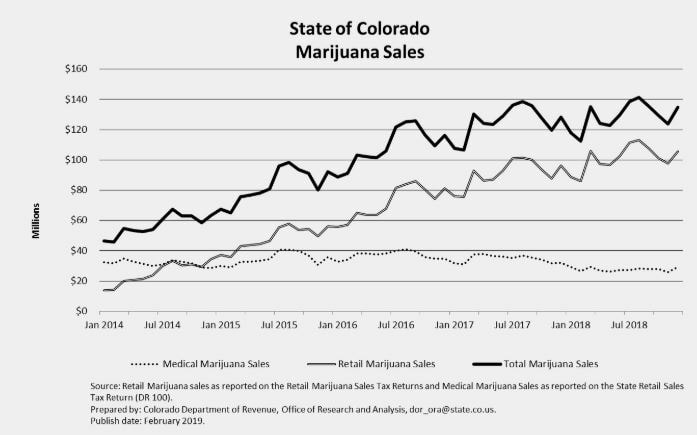

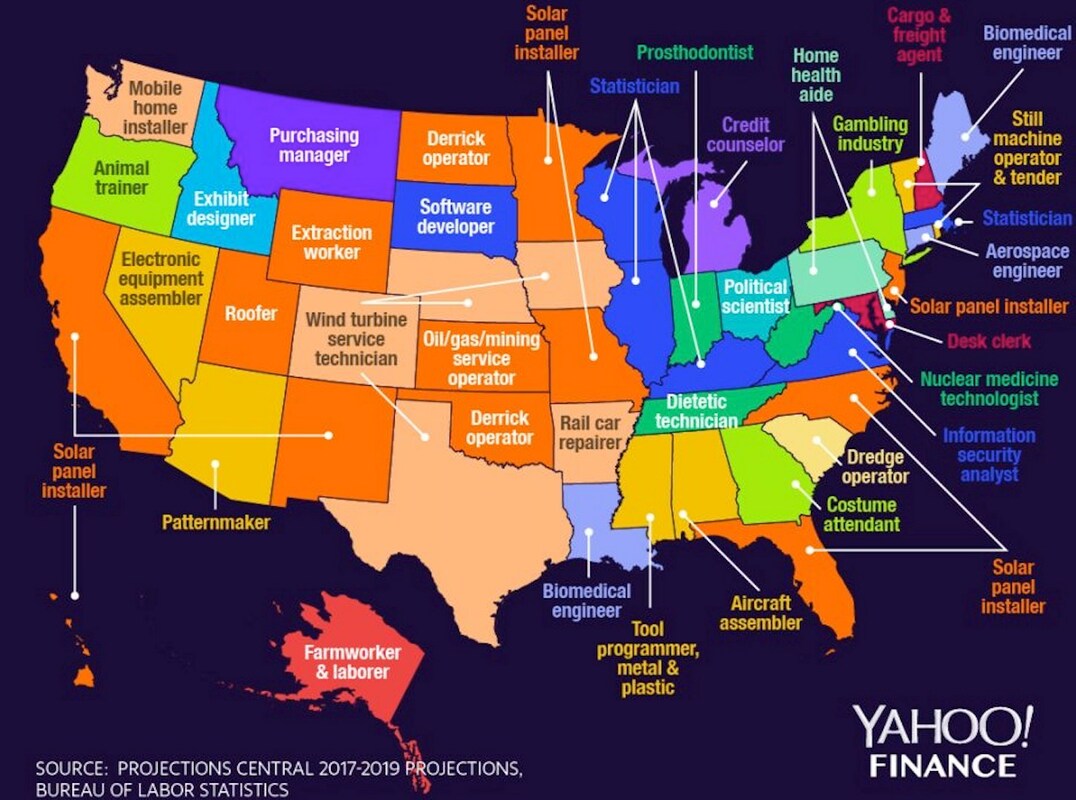

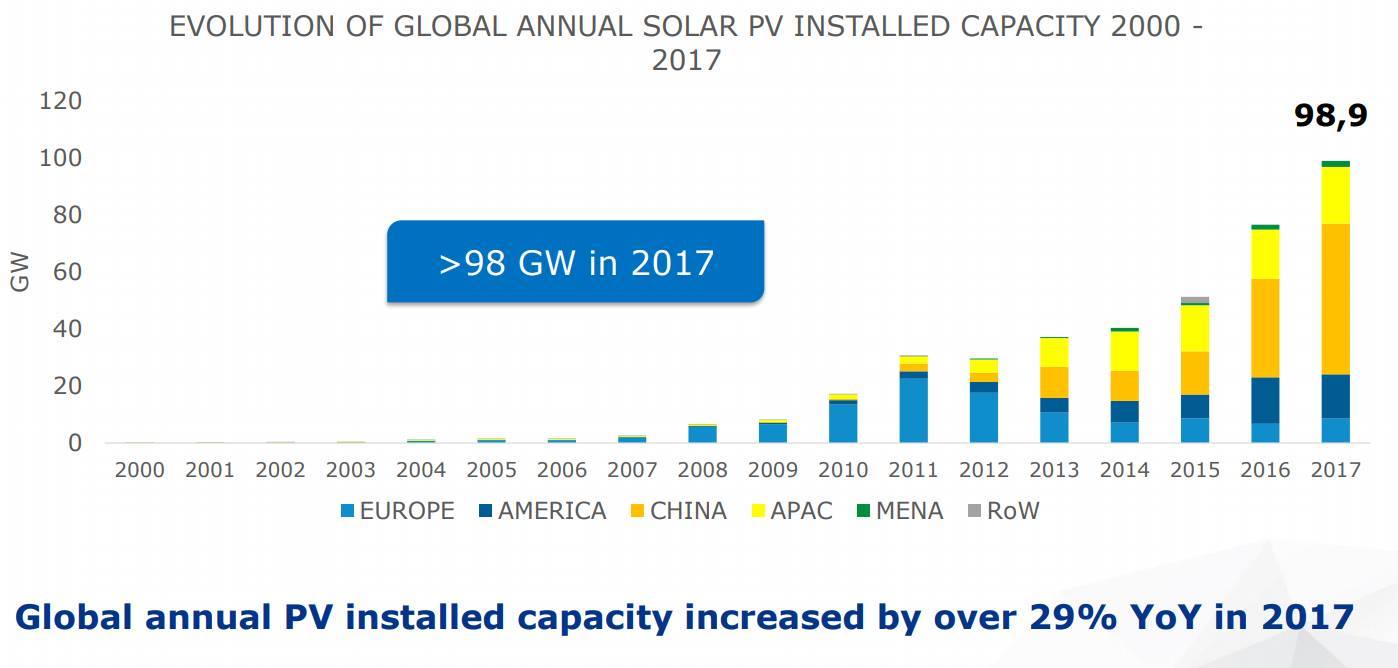

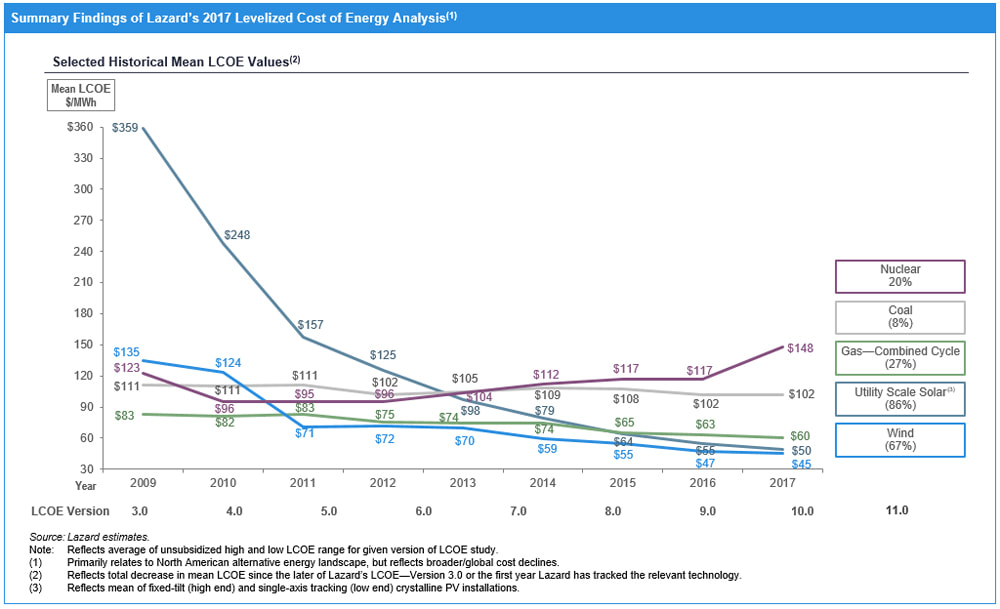

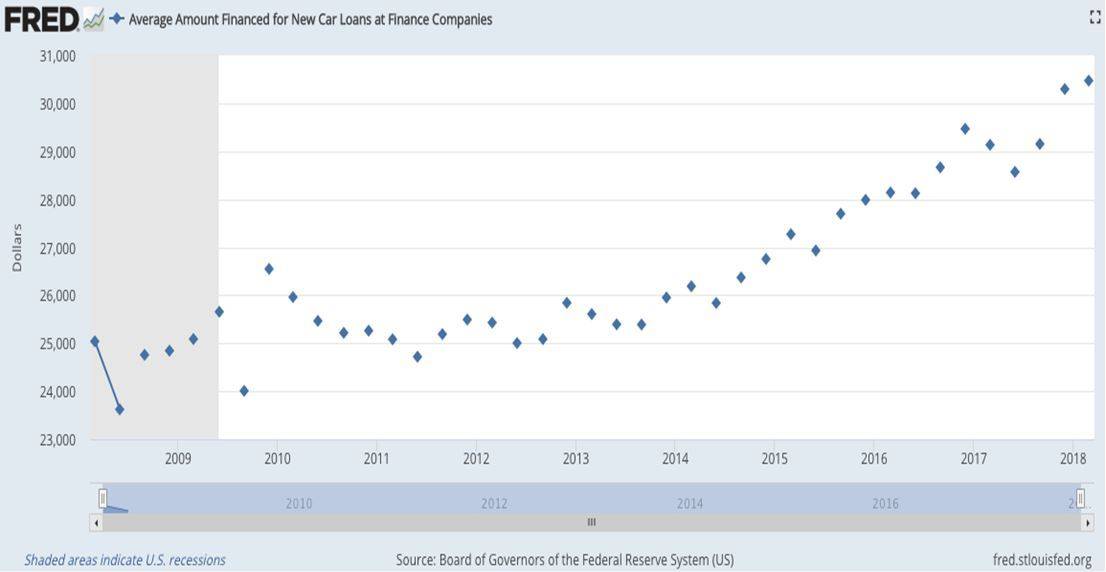

Over the course of my thirty-year career in the financial services industry I have seen and continue to hear many investment theses. Some brilliant, some not so much so. I have also witnessed a number of changes that in retrospect were obvious and inevitable. The personal computer revolution was one of the first. I recall there were many would be winners that vanished into dust, but some of the early players like Intel, Microsoft, and Cisco became the next generation of mega-cap companies. Likewise, with the internet boom. Companies came and went, but some like Amazon and Google became behemoths. Cell phones were the stuff of dreams in my youth, but the ability to access people and information, no matter where you are, was inevitable and although early participants like Nokia and Motorola have become footnotes, Apple and Samsung have had explosive growth and rewarded investors many times over. Recognizing inevitable change is only half of the battle for successfully profiting in new industries and market opportunities. Diversification and patience are more important long-term ingredients to financial success. If you put all your eggs in the Commodore computers basket you were a loser. The same for eToys.com or Lycos, or Palm Inc. Even if you recognized the inevitable, it was still much too easy to lose all or most of your investment. Perhaps, though you were bright enough or lucky enough to pick the winners. On 3/24/1980 you could have bought Intel for just $0.32 adjusted for splits. By 10/20/1980 it had already soared 56% to $0.50. A year later, the price had fallen about 48% to just $0.26 per share. Would you have held on? Would you still have faith that this was inevitable? It wasn’t until the second quarter of 1983 that Intel reached that $0.50 peak again. Today, no one gets very excited about Intel, but the stock price has reached $51 per share netting those long-term patient investors $100,000 for every $1,000 they invested nearly 40 years ago. So, although you can find inevitable investment opportunities, today the rush of the quick pop in price per share will not always be there. Sometimes, it is just waiting, and waiting, and waiting. With those words of warning, we will share with you four inevitable investment opportunities we feel all investors should be considering right now. Cannabis In January of 2012, marijuana became legal for medicinal and recreational use in Colorado. In 2018, it became legal for the entire country of Canada. Around the world attitudes toward “pot” are changing rapidly. We are now witnessing the birth of an entirely new industry. We believe the opportunity is akin to the liquor industry at the end of prohibition, and we are not alone. On November 1, 2018, Constellations Brands (STZ) closed a $5 billion investment in Canadian cannabis producer Canopy Growth (CGC). On August 1, 2018, Molson-Coors (TAP) announced a joint venture with Canadian cannabis company HEXO Corp. (HEXO) to develop non-alcoholic cannabis infused beverages. Additionally, in December of 2018, Philip Morris (PM) invested $2.4 billion in the Canadian cannabis company Cronos (CRON). What do these large multi-national companies see in the future of the cannabis market? Take a look at some of the numbers.  In four and a half years, total sales of cannabis have more than doubled in the state of Colorado, jumping from $683 million to over $1.5 billion. Colorado ranks 21st in the US by population with about 5.7 million residents. That works out to sales of about $263 per year per person. There are now ten states in the US where cannabis is legal for both medicinal and recreational use. This includes California, ranked number 1 by population and Michigan ranked number 10. These states in aggregate have a population of about 80 million. Throw in New Jersey and New York who are likely to follow suit and that means about one third of American’s live in states where cannabis is legal. Even if Colorado is an outlier and sales in other states are only say 70% as high (haha) or $184 per person that works out to a market of $14 billion. Maybe Constellation Brands and Molson-Coors envision a day when you stop by your local pub for a cannabis infused drink rather than a beer. For comparison, the US market for beer topped $35 billion in 2018. Like the acceptance of the lottery, there will be many states reluctant to join the party for moral reasons, but sooner or later acceptance is inevitable. Renewable EnergyNo, you don’t have to be a tree hugger to realize that renewable energy is inevitable. Take a look at this chart from Yahoo Finance showing the fastest growing jobs in every state.  In eight states, the fastest growing job is solar panel installer. In four states, the fastest growing job is wind turbine service technician. Climate change concerns aside, it is obvious renewable energy is becoming a much bigger deal both in the US and abroad. Although, starting from a low base the following chart from the Yale School of Forestry illustrates the beginnings of an explosive growth in solar energy production worldwide.  Much like the tipping point in software adoption, we believe solar installation will reach a critical mass that will one day lead to a distributed production model for energy use. With a large installed base of photovoltaic solar panels, today’s electric utility could evolve into a sort of common carrier like the Telcos, moving electricity from areas of high production to areas of high consumption. Your rooftop solar array and the arrays across the nation would provide power for homes and factories across the country. Rather than spending most of their capital on new power generation assets, they might spend more on upgrading and improving the efficiency of our electric grid instead. Both utility scale solar and wind systems currently provide the lowest power costs available. As photovoltaic systems improve, and manufacturing systems evolve, the price will head only one way – down, as illustrated in this chart from Lazard on levelized energy costs.  Autonomous VehiclesYou have likely heard about the Tesla (TSLA) cars with autopilot, or maybe Google’s Waymo division. The first generation of self-driving vehicles is nearly here, and it means big change for the entire transportation industry. It will change the way automobiles are used, change the ways roads are built, and change the way freight is shipped. Like most people in America, you own a car that sits parked in your garage or at your place of employment 90% of the time. Cars are expensive. There was a time when the average family could buy a vehicle and pay for that vehicle with three-year financing. Today dealers are stretching that financing out to six or even seven years to make ownership possible.  Imagine getting up in the morning and using a smartphone app, you summon your ride to work. On the way you are free to check your email, read the news, or even just nap because you are not driving the vehicle - it is driving itself. In 2018, the average payment for a new car in the US was $523 per month. That doesn’t include insurance, fuel, or maintenance. It is easy to guess that the total cost of car ownership to be around $700 per month. With autonomous vehicles, you would pay only for the time you are using the vehicle and various companies would own fleets of vehicles around the country. They would pay for the maintenance and insurance, you would just rent a ride. Again, once critical mass is reached with autonomous vehicle adoption, our roads would become safer, parking garages would go the way of payphones, and travel becomes less frustrating. How many traffic jams would be eliminated if crashes were rare and rubbernecking were eliminated? Shipping freight will change radically as well. Without the need for human drivers, shipping companies would program their trucks for fuel efficiency rather than speed. Trucks would travel the highways 24/7. If you have ever been on an interstate highway in the wee hours of the morning, you know there is almost no one using the highway. This becomes prime time for shippers, resulting in less congested roads and decreased need for new road construction. For all these reasons and more, we see autonomous vehicles as an inevitable change. The Wilshire 5000 Yep, it’s as simple as that. History has shown that investing is common stocks for the long run inevitably creates wealth. Markets go down but they do not stay down. You don’t have to be a genius or a prognosticator to participate and profit from the inevitable growth generated by a group of great American companies. Back to our question about Intel. Did you buy it? Did you hold it? The Wilshire Index did. Same for Apple, Netflix, Tesla, and many other great and not so great companies. Some companies that were in the index disappeared, but the growth of market value marched on anyway.  The Wilshire 5000 Index is a market cap weighted index of all the actively traded stock on all the US exchanges. Originally named the 5000 because when the index was first constructed in 1977, there were about 5,000 companies actively traded in the US. As of June 30, 2018, there were 3,486 companies in the index. You will find the components of all the inevitable trends we covered here, and some that we may not be aware of included in the index. If new companies come to market in the future, they will be added too. The companies in the index are updated monthly to include IPOs and corporate spinoffs and also to remove companies that move to the pink sheets or cease to trade actively.

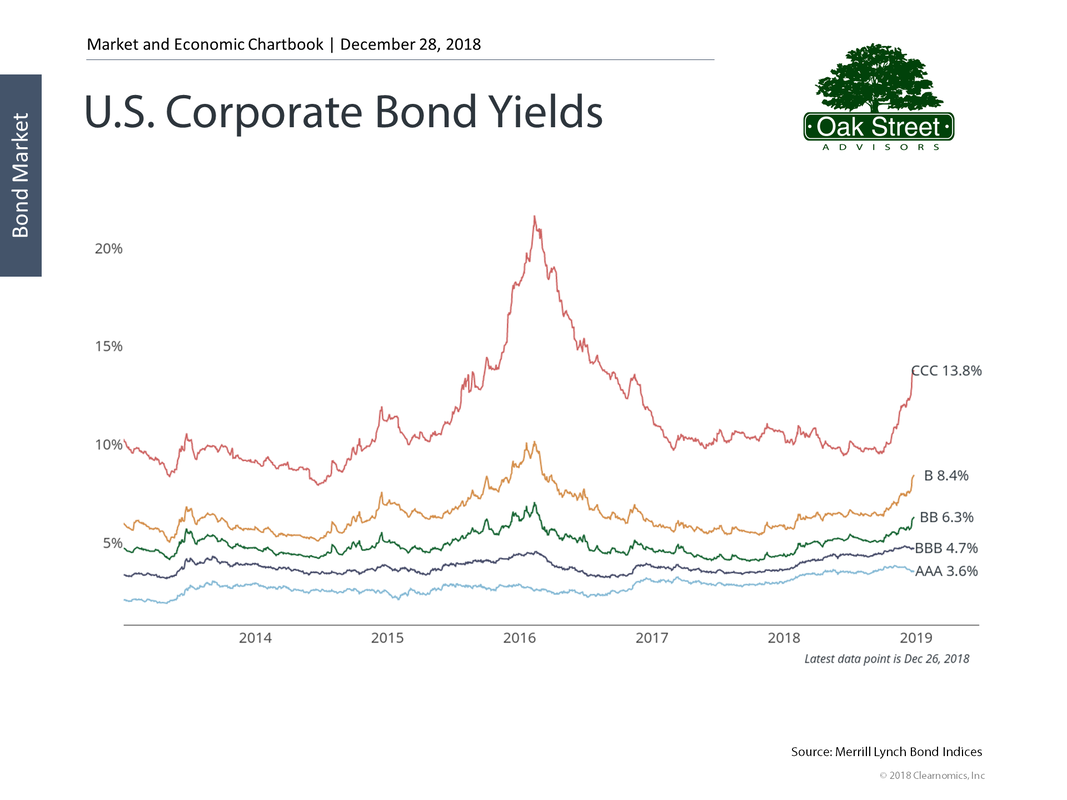

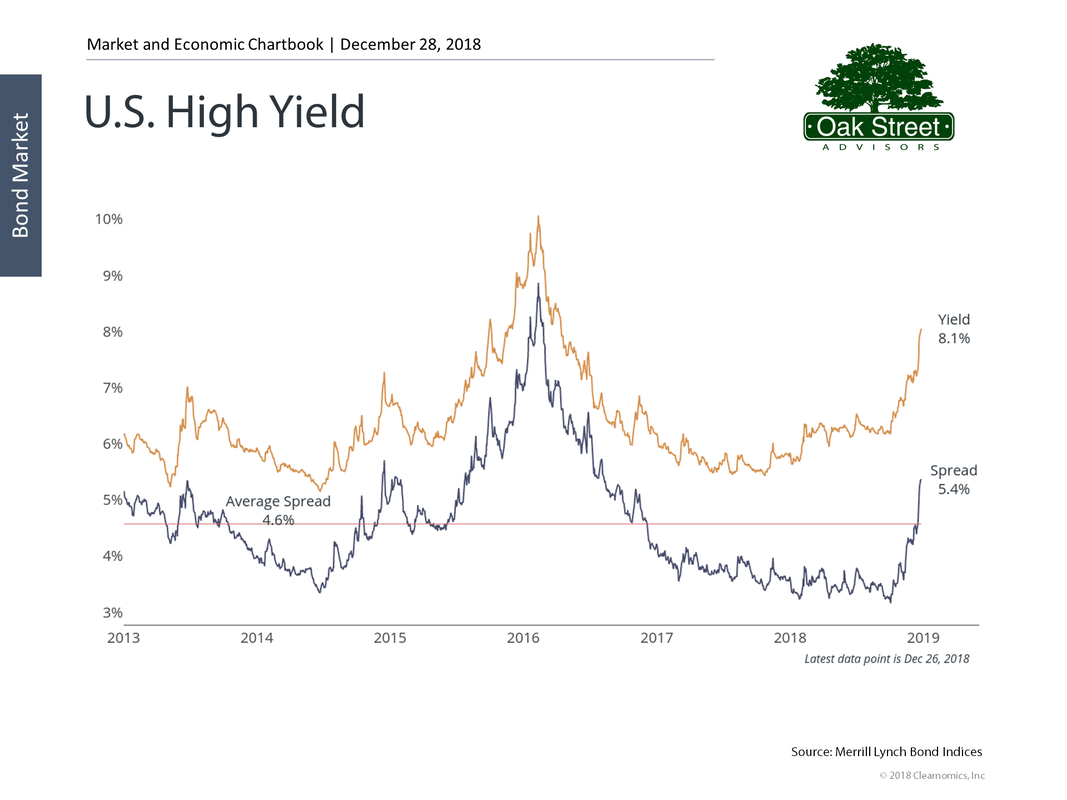

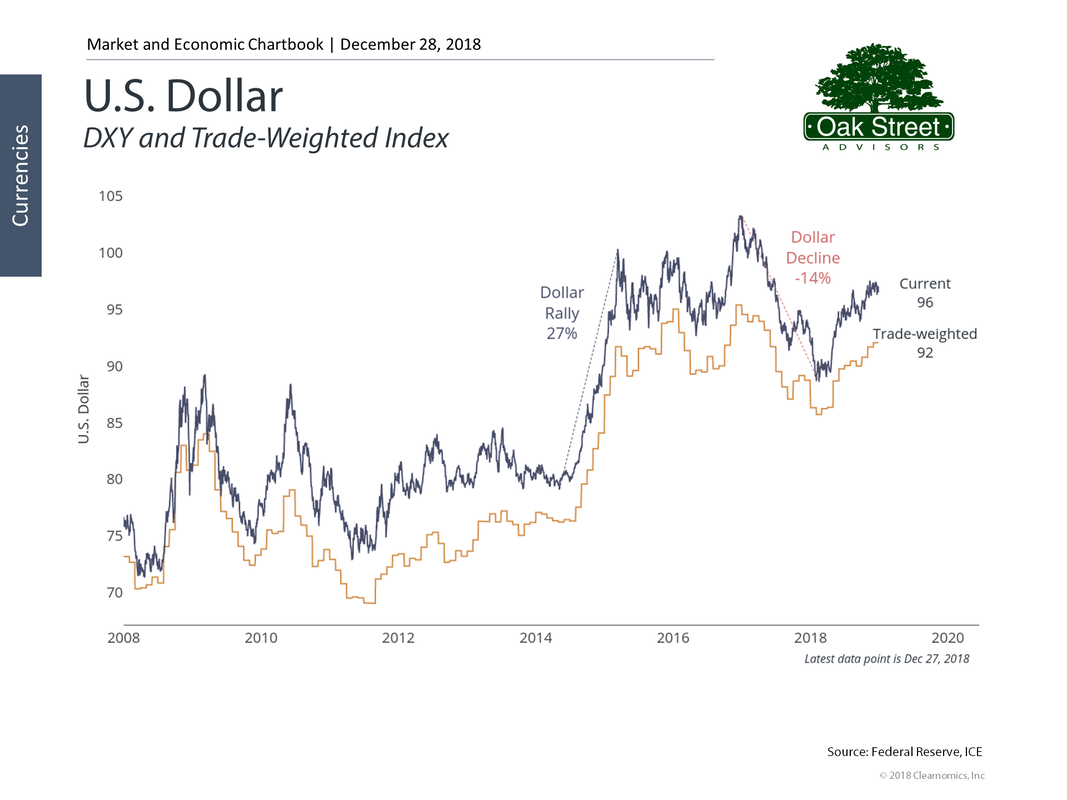

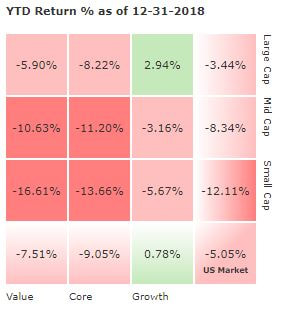

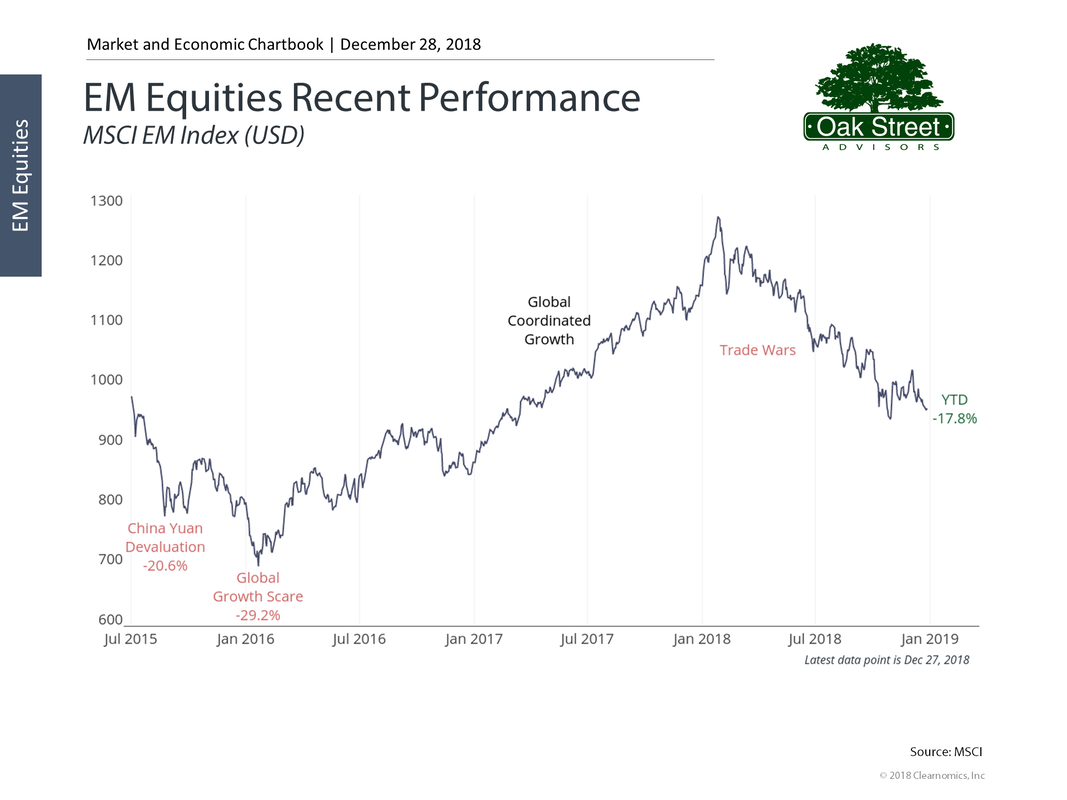

The 6th Financial Commandment for Millennials: When it's (Not) Smart to Max Out Your Retirement Plan1/17/2019

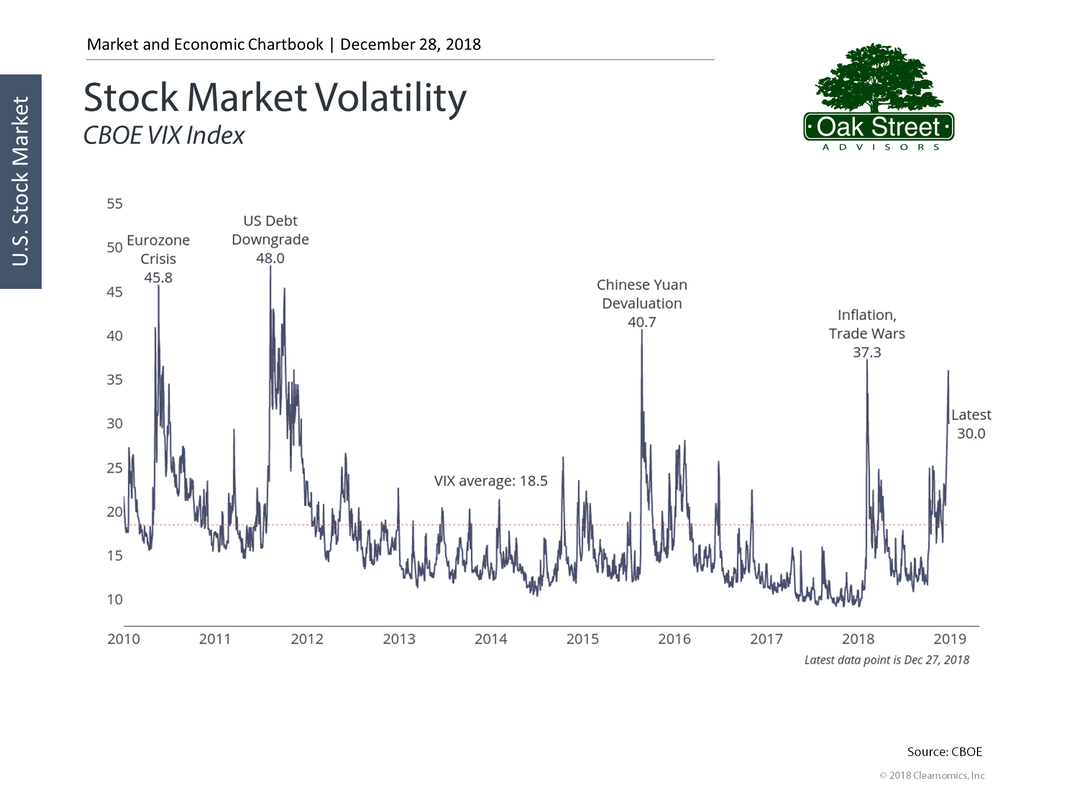

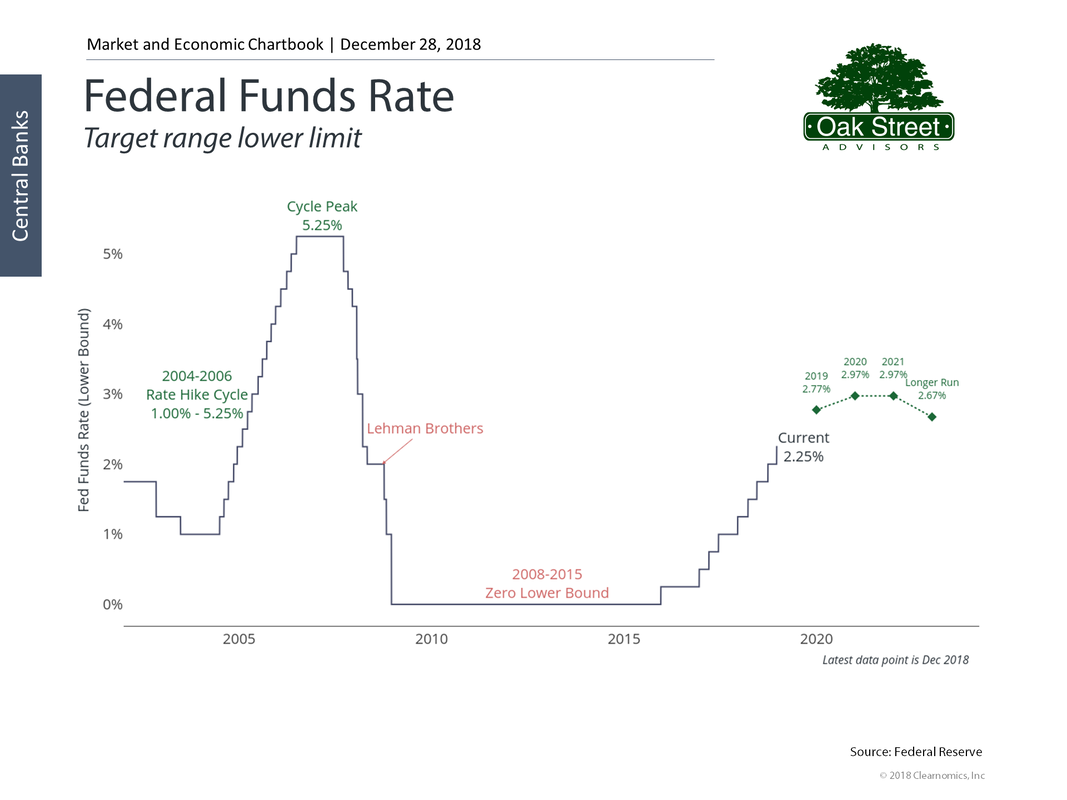

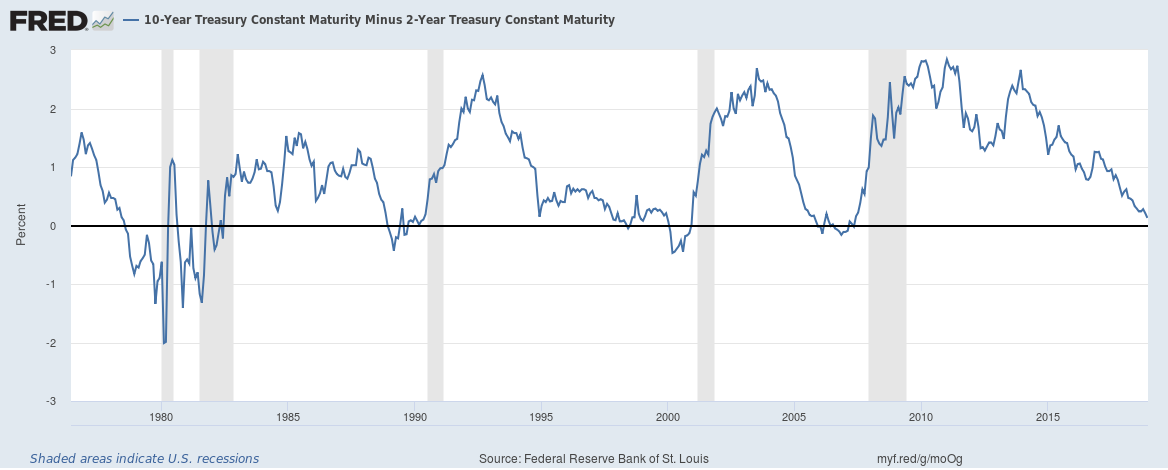

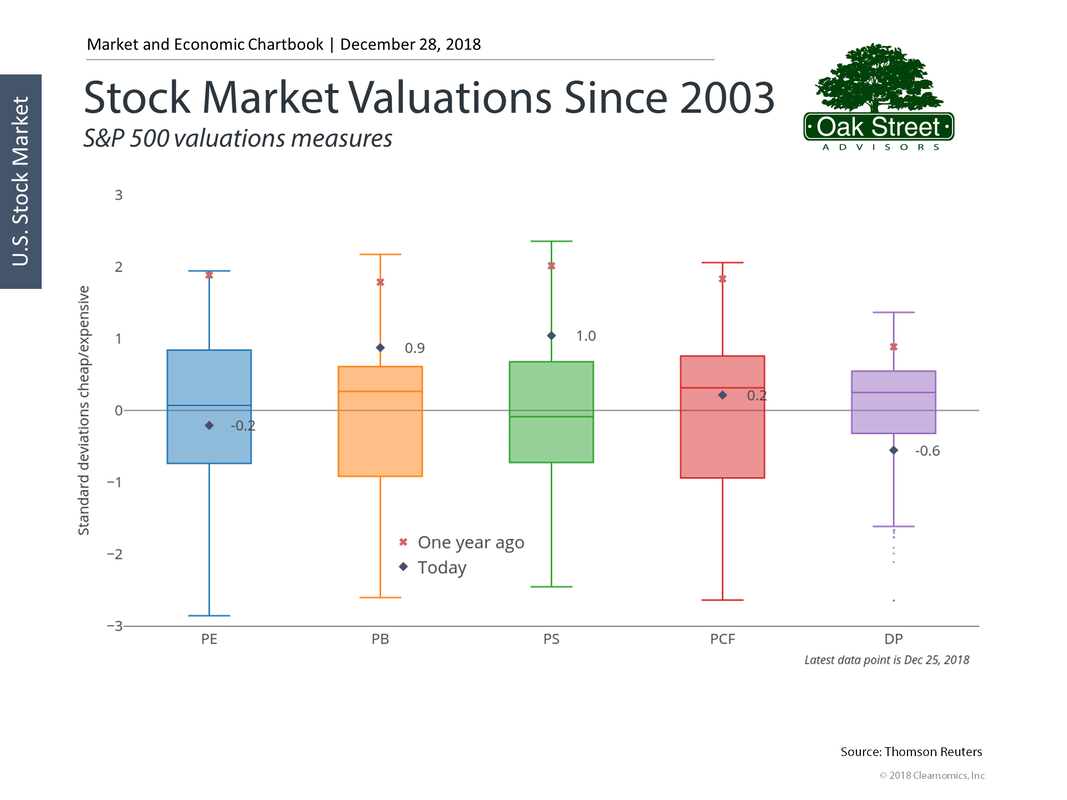

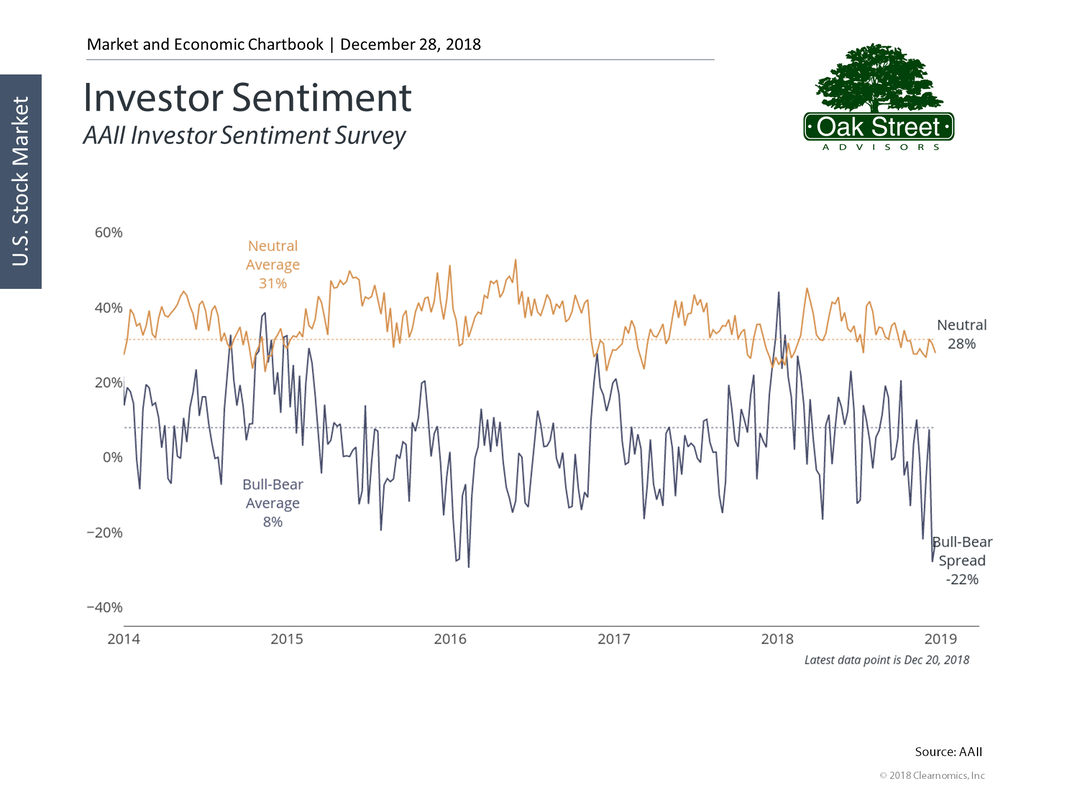

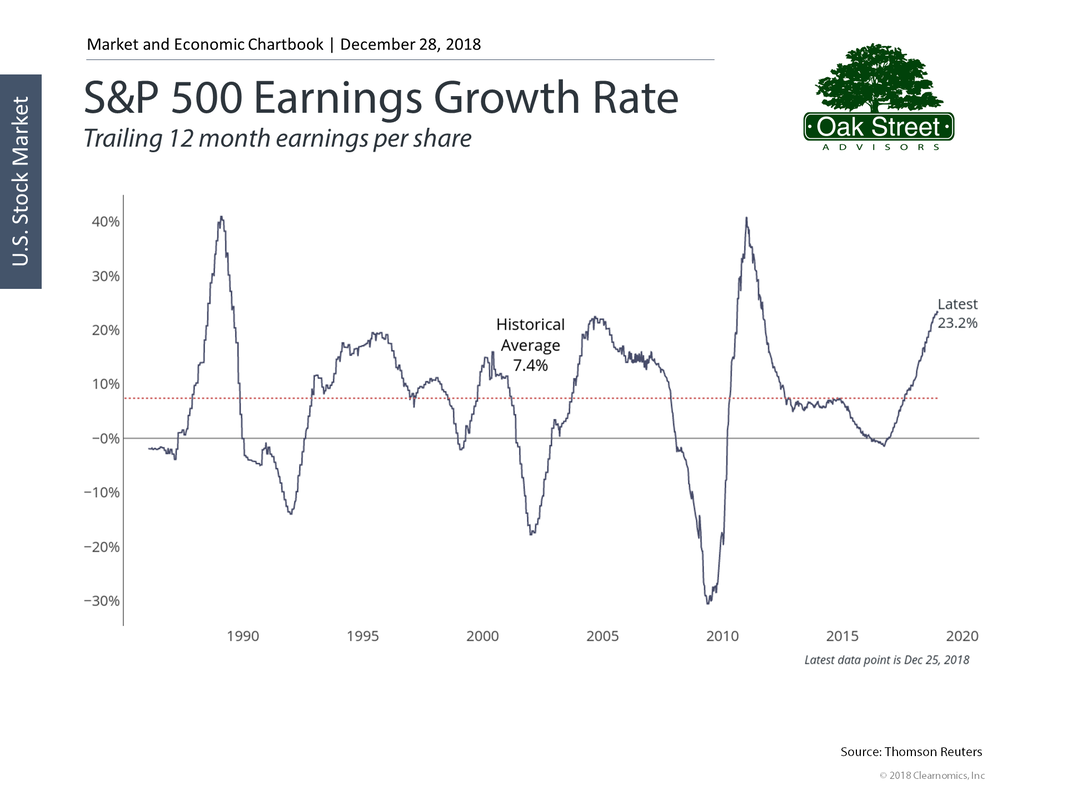

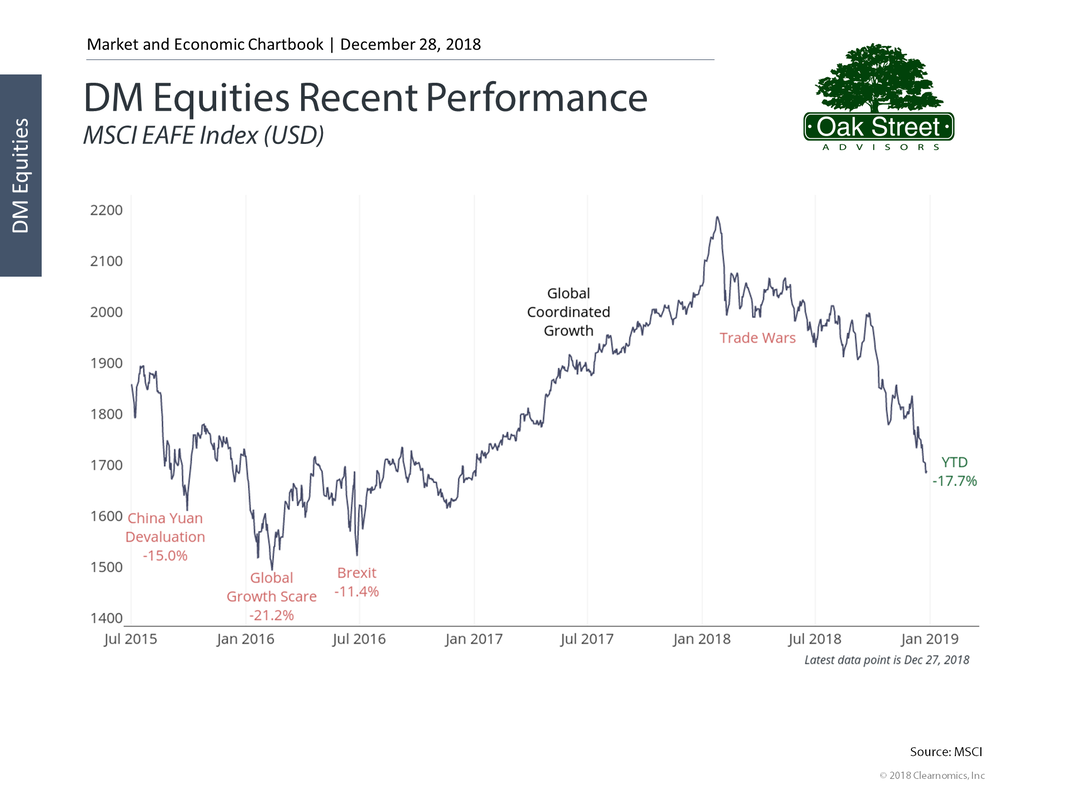

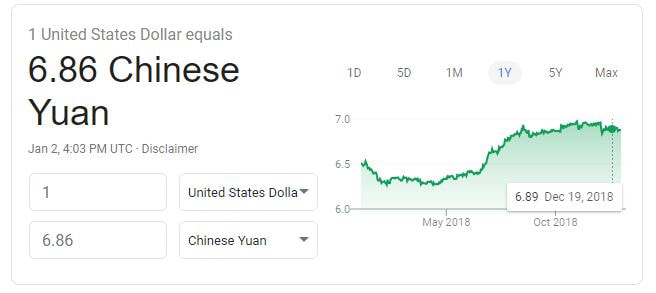

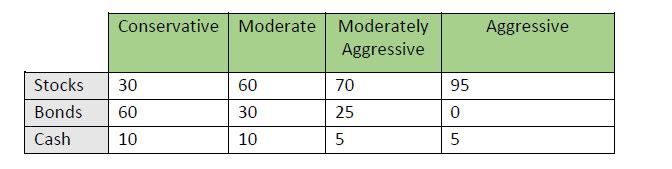

Whether you’re enrolled in an employer retirement plan like a 401k, are self-employed and can utilize a SEP or Solo 401k, or are forced to brave it alone and contribute to a personal IRA – and you’ve completed the previous Financial Commandments for Millennials it's time to start making the maximum contributions to these plans. First things first, regardless of how your 401k or other employer plan’s investments and fees are structured, investors should always contribute enough to their employer retirement plans to receive the full employer matching…aka the free money. After that, don’t max out your contributions blindly. There are a number of factors that should be considered when determining where your savings should be invested, and an employer retirement plan should be analyzed just as thoroughly as any other investment vehicle. For example, a low earner with access to a poorly constructed and expensive 401k plan may find it more advantageous to only contribute enough to receive the full employer matching (free money), while making the remainder of their contributions to a Traditional or Roth IRA that offers full diversification with lower fees; at least until they reach maximum IRA contributions. If the same investor is a high earner, eating those high expenses might be worth it. Inherently, these investors have more excess income to be deferred in the first place. If they’re in the 32% tax bracket currently, they may want to defer income until they retire in a few years and their tax bracket drops to 22%. In this scenario, the tax savings may outweigh the high costs of the 401k plan.  The bottom line is that everyone’s circumstances are different and investors need to be aware that just because they have access to a 401k plan doesn’t mean it’s always the best investment option. Ideally, you’d want to see total expenses equal to or less than 1%; anything near or above 1.5% should give you cause for concern. You can also reach out to a fee-only financial advisor who can help you determine your plan’s fees and the best investment strategy for your personal situation. You could also ask for a copy of your plan’s 408(b)(2) and 405(a)5 fee disclosures and fund expense breakdown to find out. Once you determine the best vehicle(s) to make your contributions, how should you invest it? You can refer to last month’s article Asset Allocation and Risk Tolerance or you can access Oak Street Advisors’ 401k Like a Boss employer plan investment strategy workbook as a starting point.  Volatility Wow! 2018 went out with a huge rise in volatility as stocks swung from a small gain for the year to nearly reaching bear market territory, before rebounding yet again to end the year down 4.38% as measured by the S&P 500 index  For 2019, you should expect volatility to remain high. Markets will continue to gyrate as we face increasing political uncertainty. The government shutdown will likely become an extended event, as neither side is likely to move much, and negotiating with the executive branch is like trying to eat Jell-O with chopsticks; it wiggles all over the place. While some may find these tactics a refreshing change to the way our government usually works, the markets are likely to be confused by the new normal and react with wild swings based on the latest news cycle. The unpredictability of the current administration will continue to promote volatility as markets react to a constant barrage of headlines and unconventional political tactics. Interest Rates The Federal Reserve raised rates 4 times in 2018, moving the benchmark short-term rate from 1.25% to 2.25%. This resulted in a difficult year for bond investors as fixed income indices fell for the first time since 2013.  There is also concern about the yield curve. While the yield curve has not inverted yet, it is dangerously close to doing so. The chart below shows the 10-year treasury yield minus the 2-year treasury yield, going back to the 1970s. The shaded areas represent recessions. Historically, an inverted yield curve has presaged recessions and Fed economist David Andolfatto recently argued that an inverted yield curve could actually cause recessions. Regardless of whether an inverted yield curve is a leading indicator or a contributing factor to recessions, being on the cliff’s edge as we are now adds to the uncertainty surrounding markets going into 2019.  With worries about a possible recession on investors minds, credit quality spreads are finally normalizing after years of compression following the credit crunch of 2008-2009.  2019 may be the year we finally find some value in high-yield bonds after nearly a decade of tightened credit quality spreads.  Rising interest rates also leads to a stronger dollar. This makes US produced goods more expensive for foreign buyers and can dampen the earnings of US exporters.  Equity Markets After a fast start in early 2018, the equity markets fell hard in the 4th quarter of the year. Nearly every subcategory of the market ended 2018 in the red.  But compared to one year ago, equity valuations have fallen, based on many metrics.  Have equity valuations fallen enough to make stocks a compelling value? No one knows for sure, but investors should keep in mind that their default position should always be to remain fully invested. Remember, the price of the long-term gains historically inherent in the equity markets is the short-term pain caused by corrections along the way. Investor sentiment remains muted, offering more good news for contrarian investors.  Earnings among the companies in the S&P 500 continues to grow at a torrid pace. Lower corporate tax rates have fueled stock buyback programs that allow corporate earnings per share to grow faster than the economic growth generated by normal business operations. I would expect to see a slowdown in the rate of earnings growth later in 2019, as year over year comparisons get tougher, and interest rate increases continue to take a toll on earnings growth. That does not mean we expect earnings to fall, just that the rate of growth will moderate as 2019 progresses.  2018 was also something of a dud for foreign stock investors. Developed markets produced even lower returns for US investors than did the domestic market.  And emerging markets were equally as disappointing.  For 2019, we expect both trends to continue. Higher interest rates will generally lead to a stronger dollar and a stronger headwind for non-dollar denominated investments. In 2018, the dollar rose by about 3.5% versus the Euro and about 5% versus the Chinese Yuan. That means investors in the Eurozone needed a 3.5% gain to remain even when they convert their Euro based investments back to US dollars and investors in Chinese companies had a 5% hurdle to clear.   Conclusions At this point we believe investors should focus on US based companies and remain fully invested. Bond durations should remain short, at least for the first half of 2019, as Fed policy is still unclear. If the yield curve does invert, we would take that as a sign to lengthen bond maturities and perhaps reduce our equity holding a bit. You should expect volatility to remain elevated and look at dips as an opportunity. Important: This is not intended as investment advice. We share this so that our clients and prospective clients can understand some of the factors we consider as we implement their investment strategy. Any predictions of future events should be viewed with a skeptical eye.  Asset Allocation & Risk Tolerance Part of Oak Street Advisors’ 10 Financial Commandments for Millennials series, understanding risk tolerance, asset allocation, and their relationship, is the foundation of modern portfolio theory. Implementing the proper asset allocation to minimize risk, while still achieving your long-term goals, is crucial to your success and peace of mind. Asset allocation means: how much…of what asset. What are Asset Classes? There are 3 basic Asset Classes

You could add real estate, commodities, alternatives, and other investments to this list, but for simplicity we’ll stick with these main 3 classes. Asset allocation refers to the weight of each of these asset classes in a portfolio. Here’s a generic look at how we currently allocate the different asset classes: For example, at Oak Street Advisors we use the following asset allocation for someone who has a Moderate Risk Tolerance: Stocks = 60% Bonds = 30% Cash = 10% This asset allocation leaves a good portion of weight to bonds and cash; which is less risky than an Aggressive Risk Tolerance: Stocks = 95% Bonds = 0% Cash = 5% As you can see, with 95% stocks, and stocks being riskier than bonds and cash positions, the latter allocation is much riskier than the former. The reason for using asset allocation is to manage risk inside your portfolio. The more stocks you own, the more volatility your portfolio will experience. The more stock you own, the higher your return has historically been. We add bonds and cash to the mix to make the short-term swings in the overall portfolio value smaller, but in doing this we also reduce the potential returns provided by the portfolio as well. We use asset allocation to allow ourselves to stay invested for the long-term gains while sleeping well at night during times when stocks temporarily fall. Your personal asset allocation will reflect your Risk Tolerance, which can be viewed as the point where you can stay invested for the long-term gains, without making the big mistake of selling in a panic.  For some of our clients, we provide them with a short Risk Tolerance Scorecard. While brief and simplified, it gives investors a start on their comfort with investment risk. Once a risk tolerance score is determined, investors can select the appropriate asset allocation based on their individual or combined familial results. While you’re here, why don’t you determine a base-line risk tolerance by answering the following:  Grading Your Risk Tolerance: Starting from the top down, assign the number of points from 5 to 1. EXAMPLE: What is your current age? Less Than 45 = 5 Points 45 to 55 = 4 Points 56 to 65 = 3 Points 66 to 75 = 2 Points Older than 75 = 1 Point Each question is graded the same, 5 points for the first answer, 4 points for the second answer, 3 points for the third, 2 points for the fourth, and 1 point for the last. Write all your points down, then add them together. An idea of your risk tolerance is estimated from the sum of your points as follows: 1-14 = Conservative 15-21 = Moderate 22-28 = Moderately Aggressive 29-35 = Aggressive Remembering the asset allocations from above, you can select the corresponding allocation. Inside those asset classes is an investment manager’s secret sauce, but any investor can achieve these general allocations via indexed ETFs. One last point I want to present is the fact that yes, you can determine a proper asset allocation based on your personal risk tolerance; however, is that level of risk going to produce the returns necessary to meet your long-term goals? Sometimes investors must take more risk than they may be quantifiably comfortable with in order to achieve the desired outcome.  The 10 Financial Commandments for Millennials 4th Commandment: Establishing an Emergency Fund12/4/2018

The Emergency Fund: Why, How Much, & Where Part of Oak Street Advisors’ 10 Financial Commandments for Millennials series, determining the correct amount, picking a high-yield account, and saving for an Emergency Fund is critical in establishing a solid financial foundation for millennial investors. Before you start investing, you still need to complete one other, vital, step; and that’s saving enough for a properly funded emergency fund. An emergency fund is a savings account dedicated to bailing you out when unforeseen financial troubles arise. This fund is for repairing your HVAC unit, fixing your car, unexpected medical bills, and loss of wages. Your emergency fund shouldn’t be so small that you aren’t able to cover a financial crisis without going into debt; but not so large that you have too much capital allocated in cash. General savings guidelines call for 3 months of expenses for two incomes, 6 months of expenses with one income- for both single and married investors. This is a baseline, but your Emergency Fund should be dictated by your individual circumstances. You and your financial planner should collaborate to determine the amount that is right for you. Or, you can head back over to our Personal Budget Template to calculate a personal number. Once the proper amount is determined, your emergency fund should be moved into a high yield savings account. Most of us keep our savings at a big bank and receive terrible interest rates for parking our money there. While it may not seem like a lot of extra money, going from an account producing 0.01% interest vs. 2.0% interest just makes sense. Why not let your money earn the most it can for you? For example, say you have $10,000 in your Emergency Fund: Bank A Bank B Interest Rate 0.01% 2.0% Amount You Earn/Year $10 $200   Mistakenly, many believe that they do not have enough assets to worry about estate planning. With today’s $5.6 million exclusion per individual and simplified portability that raises a couple’s exclusion to $11.2 million, estate taxes may not be an overbearing concern. But there are many estate planning steps everyone with heirs and assets should take. A financial plan would be incomplete without a review of the basics of estate planning. As a fiduciary, your advisor should cover this important topic. Just be sure to work with a fee-only advisor to avoid being sold high commission and high expense insurance products you might not need under the guise of estate planning.

How Assets Transfer After Your Death Transfer by Will Assets that transfer by will are assets you specifically list in your will to any designated beneficiary. If you don’t have a will, the state you reside in has one for you. While the state's method of distributing your assets may not be what you would wish for and could lead to serious problems for your heirs, your assets will be distributed to someone. Without a will an asset could be passed under state law to your heirs as an undivided interest in a home or other real estate. This presents a problem if the asset needs to be liquidated to evenly divide and title the property. Because all parties must agree to the terms of any sale and beneficiaries may have differing opinions as to the value, holding an undivided interest can make final disposition very difficult. Sometimes sentiment will stand in the way of liquidating the asset, causing friction among family members and leaving some susceptible to emotional blackmail or simply leaving all with a claim to property that in essence has no remainder value. Another common mistake in drafting a will is to misunderstand how some assets transfer and the hierarchy of the transfer. If an asset transfers by contract, that is, if there is a named beneficiary of an IRA or insurance product, the contract takes precedent and that asset will not be available to transfer through your will. It is inappropriate to transfer certain retirement plan assets through your will. IRA and 401k type assets lose their tax advantaged status and result in needless income tax leakage for your estate. Items transferred through your will are also subject to the delays and costs of probate. Probate costs vary from state to state but it is the delay that is often the problem. If there is not enough liquidity in the estate, heirs could be hard pressed to carry the expenses of maintenance and taxes while the probate process proceeds. Another drawback to transferring assets through your will is that wills are all a matter of public record and must be filed with the county where the decedent last lived. That means your estate and its’ disposition is not a private matter. Anyone who is curious can learn about matters that you may have preferred to be private. Transfer by Contract You can also transfer assets to your heirs via contract. Contracts are private agreements and thus can preserve privacy. Assets that transfer by contract also will avoid the delays of the probate process. For example, the beneficiary of a life insurance contract will receive any funds soon after the required paperwork is completed and processed. IRA and other retirement accounts may also have a named beneficiary. Once the death certificate is presented to the custodian the distribution of those assets will begin. For this reason, it is important that you keep the beneficiary designations on assets that transfer by contract up to date. You should review your beneficiary forms regularly and any time there is a life changing event. A revocable living trust is another type of contract often used to transfer assets. Investment accounts, real estate, collectibles, and many other items can be owned by a revocable living trust. RLCs are a very popular alternative to wills. These trusts protect the privacy of your estate and your heirs and avoid the delays of probate. A common mistake in the use of a revocable living trust is forgetting to title assets in the trust name. Maybe you buy a vacation home, or you open a new investment account and forget to have it titled to the trust. You should regularly review your estate assets and be sure they are titled correctly. If you do not want to go to the expense and trouble of setting up a revocable living trust there are other tolls you can use to transfer assets via contract rather than through your will. An often-overlooked tool is called Transfer on Death (TOD). Many states have adopted laws that enable individuals to transfer assets by contract rather than by will, which greatly simplifies final distributions for heirs. For investment accounts the TOD designation allows you to specify beneficiaries for each account you may have that is registered in your name. You may specify a different percentage ownership for each beneficiary. Upon your death the assets in the TOD account will transfer to the named beneficiaries without the delay of probate and separate from other items in your will. You can make changes to the beneficiaries and their percentage participation whenever you choose. There is usually no additional charge for having the TOD designation added to your account, but not all institutions may offer this type of account, so be sure to ask. For banking accounts you should know about the Pay on Death designation which works in a similar fashion, and also avoids probate. Ask your banking institution if they offer this type of account. Per Stirpes Per Stirpes is a Latin term meaning "per branch". It indicates how property should be distributed in the event of a named beneficiary is deceased. For example let's say you have a son and daughter who each have two children of their own. You have an IRA which you wish to leave to your children in equal shares. If you have indicated this on the IRA beneficiary form you may think all is well. However, suppose your daughter is traveling with you when you both die in an automobile accident. What will happen to the assets in the IRA? Without the per stirpes indication the IRA will transfer Per Capita, meaning your son will inherit all the assets in the IRA, leaving your grandchildren from you daughter with no share. If, however, you included the per stirpes designation on the beneficiary form, your surviving son would inherit his half of the IRA, and your daughter’s heirs (the branch) would inherit the other half of the assets. This dramatic difference is due to those two small words - per stirpes. Durable Power of Attorney A Durable Power of Attorney is another estate planning must have. Many of us worry, with good reason, that we might one day become incapacitated and unable to attend to our own affairs. How can we be sure our bills are paid, our investments are managed, or our property sold if the need arises? A power of attorney is a document that delegates legal authority to another person. You may be familiar with a limited non-durable power of attorney from attending a property closing when one of the parties is absent. The Power of Attorney allows the principal (person granting the Power of Attorney) to name an Attorney in fact (the person to whom the legal authority is being delegated) to sign documents to effect a property closing on their behalf. Non-Durable Powers of Attorney can be granted for a wide variety of tasks, and they remain in effect until canceled by the Principal or until the Principal becomes incompetent or dies. A durable Power of Attorney is often granted between spouses or between a parent and a trusted child or other relative. The durable Power of Attorney as the name implies enables the Agent to act on the Principals behalf even if the Principal becomes mentally or physically incompetent. This is an important distinction. Should the Principal become incompetent through disease such as Alzheimer's or as the result of an accident or illness, there is someone in place who can make legal decisions, access funds, and pay bills on behalf of the Principal. As with non-durable POAs a durable Power of Attorney ends when revoked by the Principal or when the Principal dies. If you have not executed a Durable Power of Attorney and you become unable to handle your own affairs your family will probably have to go to court to have you declared incompetent - a very public airing of a very private matter. The court must then appoint someone, maybe not the person you would choose to handle your affairs. Sometimes a bond must be posted, an attorney or CPA hired to prepare detailed financial reports that must be filed with the court, and the court must give permission for certain transactions like the sale of real estate. All of this can be a long and expensive undertaking that can easily be avoided with proper planning. Healthcare Power of Attorney The healthcare power of attorney, sometimes called a healthcare proxy, is another estate planning necessity. It names an individual to make healthcare decisions on your behalf when you are incapable of making those decisions for yourself. Not to be confused with a healthcare directive, this document works much like a durable power of attorney except it is for medical care rather than financial assets. Usually it is granted to a spouse or close relative to grant them the authority to make healthcare decisions on your behalf. Healthcare directive While not a legal document a healthcare directive does inform your family of your wishes for end of life care. You should not subject your family to the agony of having to guess under what circumstances you would like medical care withheld. You should spell out the conditions under which you would like to not be revived or the treatments you would not want to be subjected to. If you do not want to be kept alive by feeding tubes or respirators at some point, you should spell out those circumstances and spare your family any potential guilt or heartache of having to make such hard decisions at what will be for them a very horrible time. Letter of Instruction Another non-legal document you should prepare is a simple letter telling your heirs who they should contact if you die and where they can find documents they will need as they close out your estate. Some of the items you should include are:

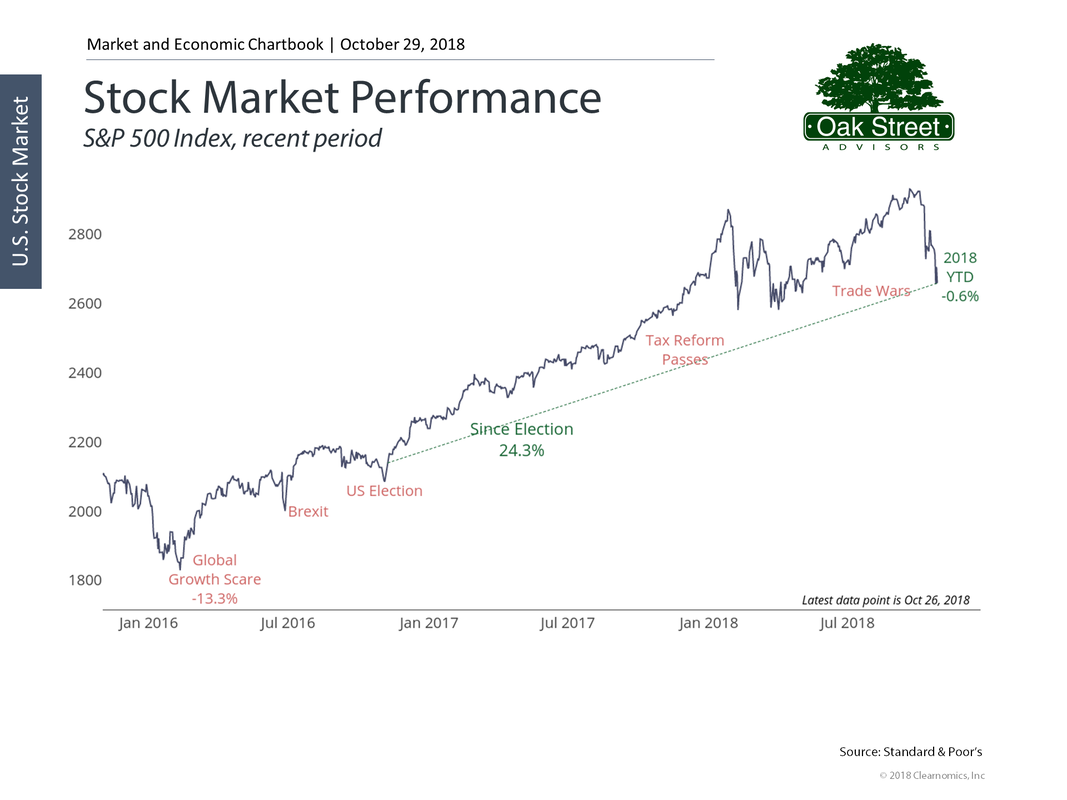

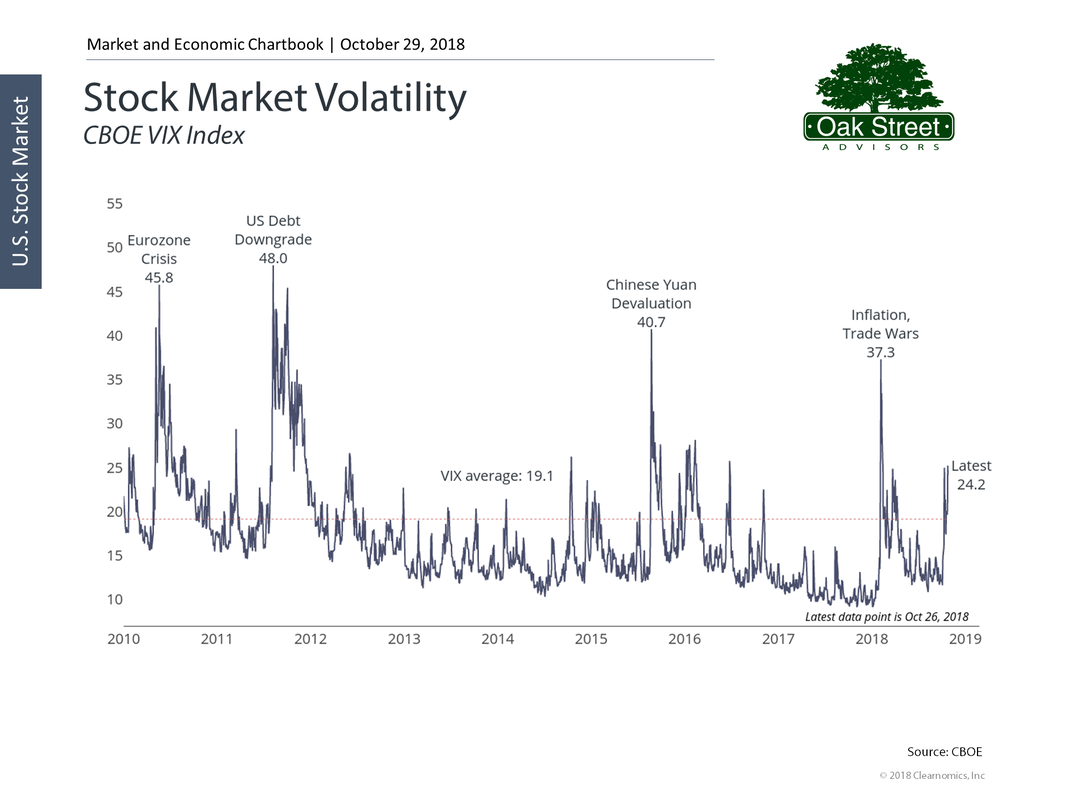

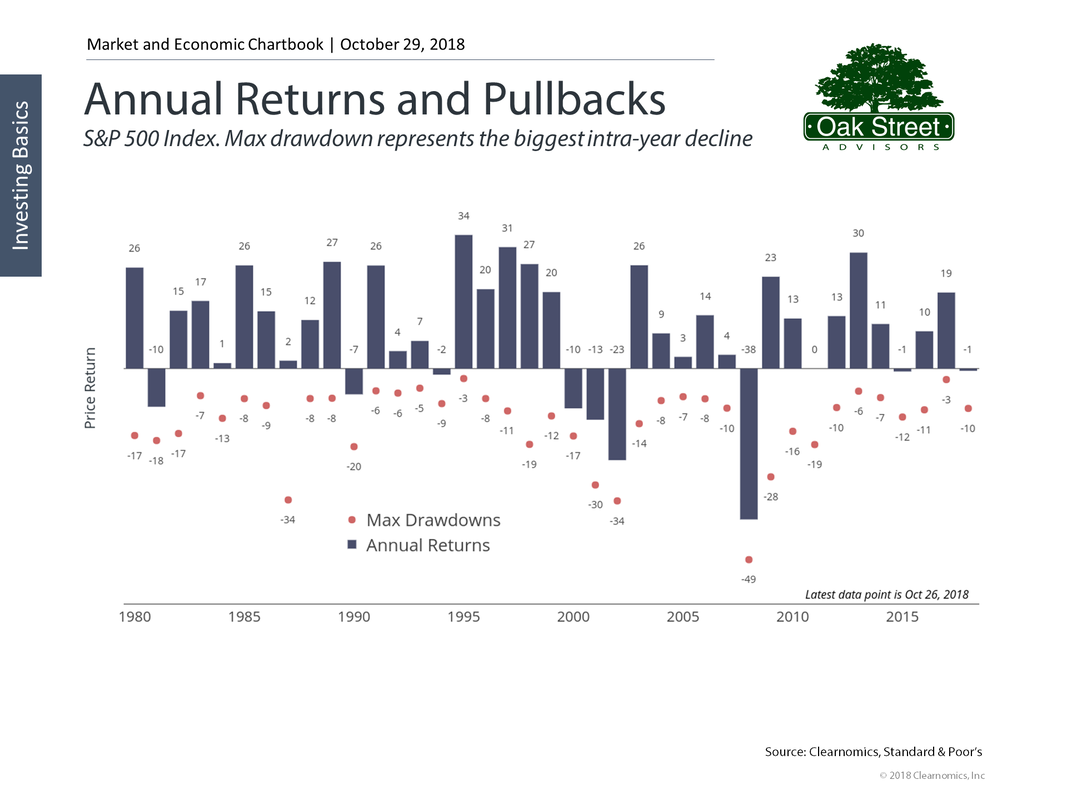

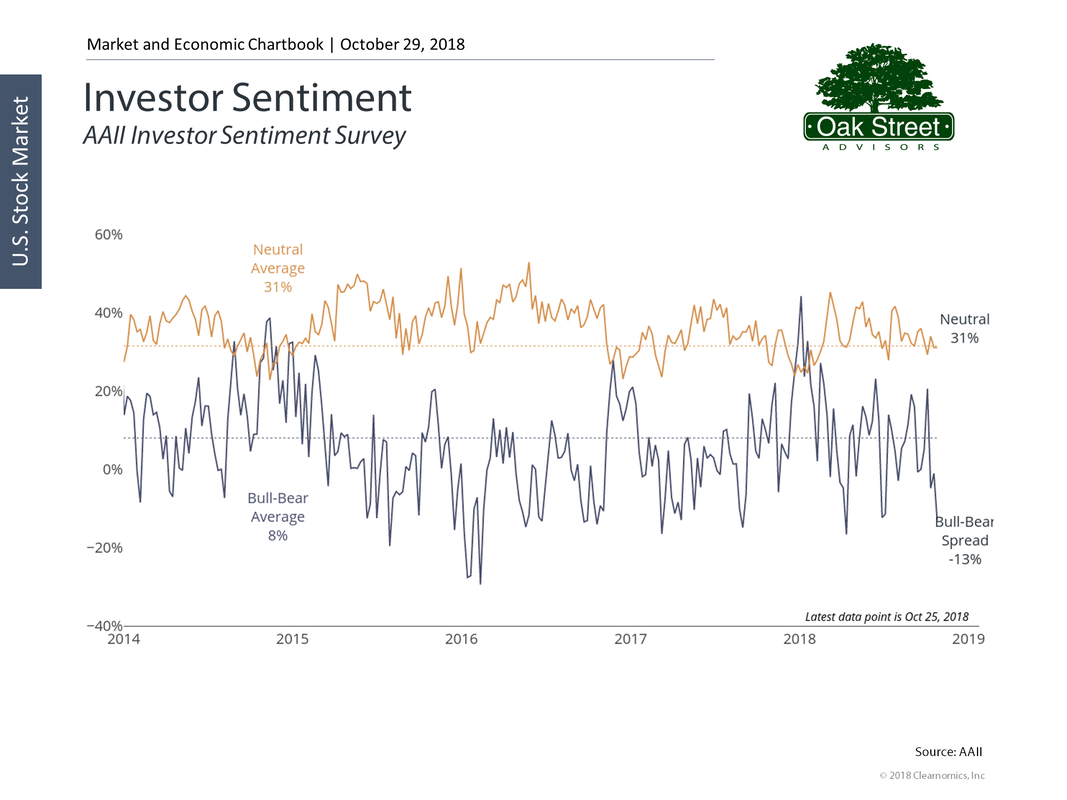

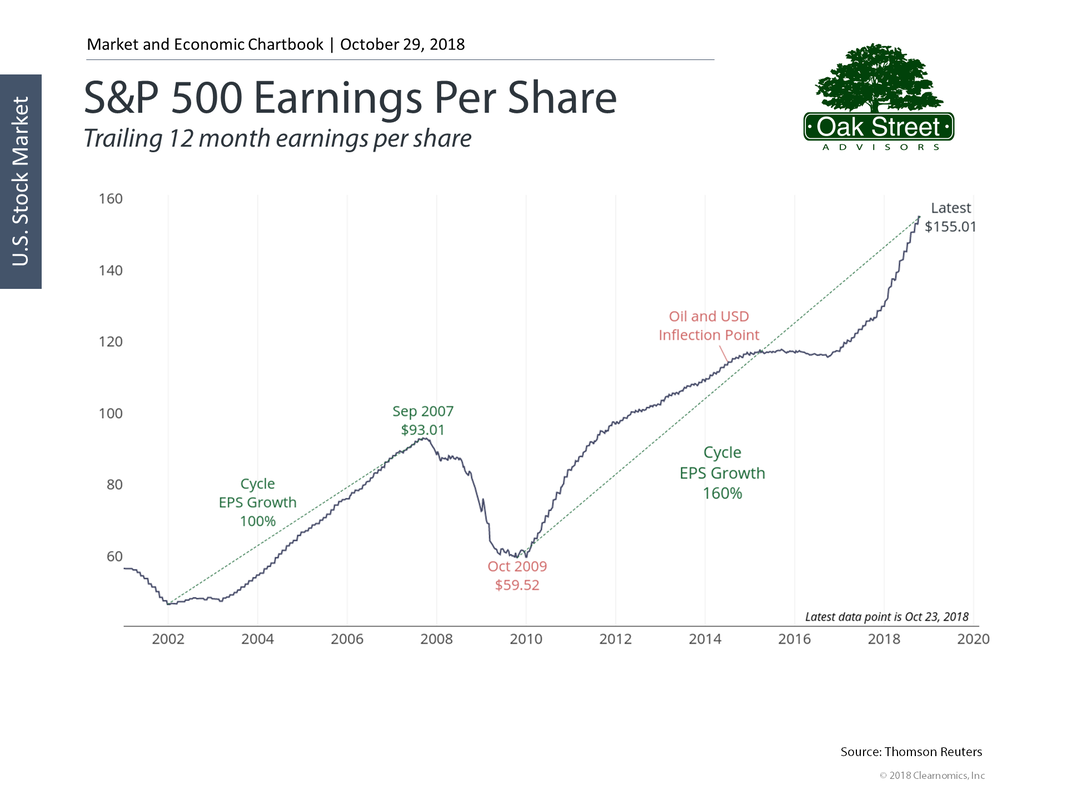

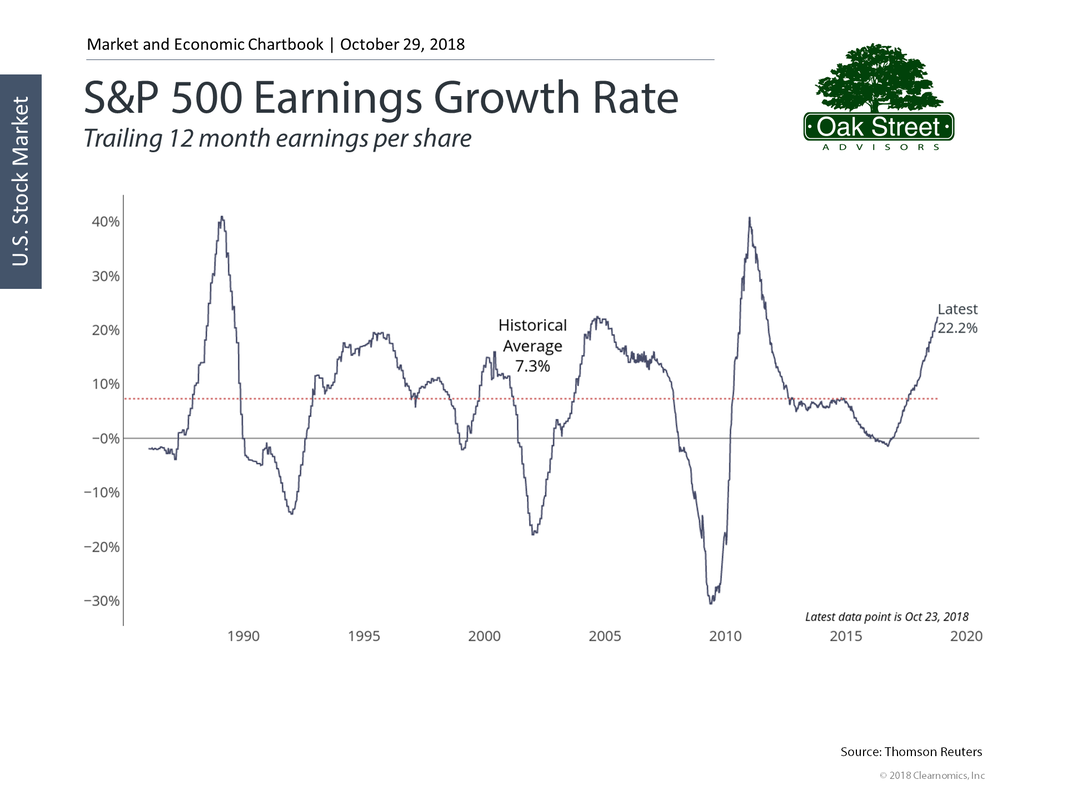

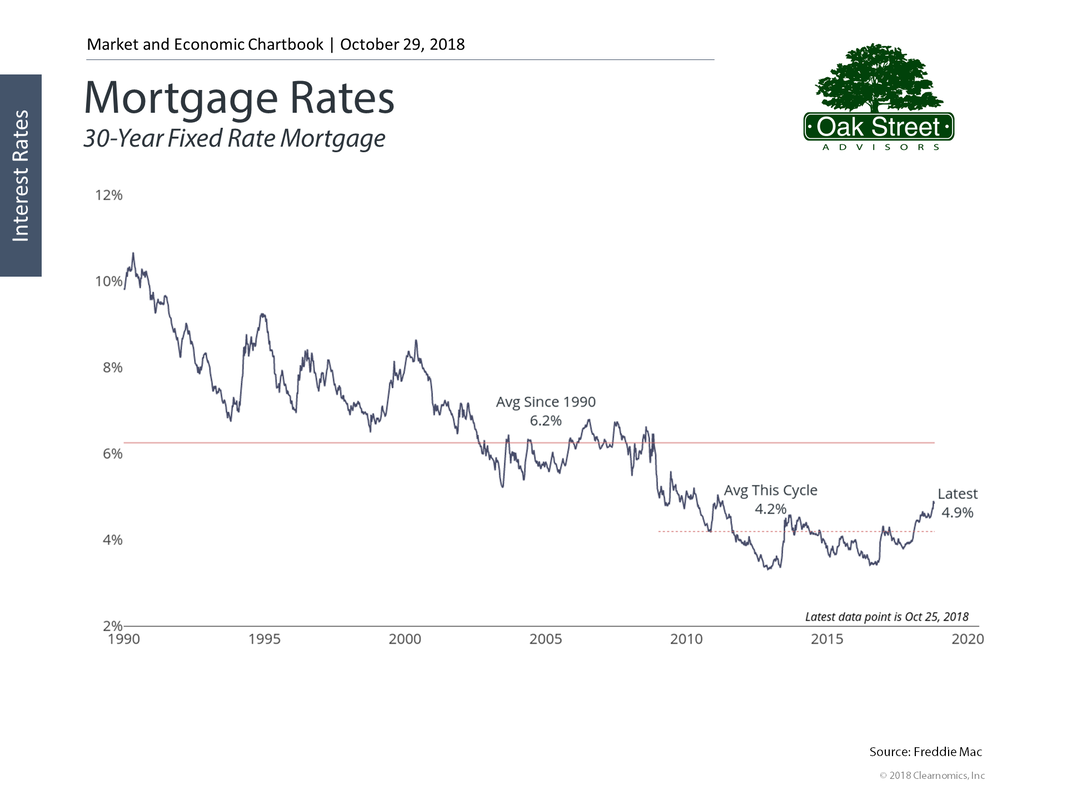

Scary Movie Part 2Just in time for Halloween the stock market has pulled back from its all-time highs and volatility has returned in the form of daily changes of more than 1%. After being up nearly 10% this year, the market- as measured by the S&P 500 index, is flat to slightly down as you read this.  Accompanied by a spike in the VIX Index  Pullbacks in the stock market are common with a linear regression best fit of about 7.5% each year.  Looking back to 1980, even in years where the market has ended down it has rebounded from the lowest point of the year before year end. With just two months to complete 2018, it is possible that we have already seen the lows for this year. So, despite the recent pullback in stock prices this may well be a lower risk entry point for new investments. If we have in fact seen the intra-year low of -10% (with the market currently down about 1% YTD) downside risk from this point could be minimal.  Investor sentiment is tilted slightly to the bearish side, indicating to contrarians that things may not really be so bad. It is unusual for markets to enter bear market territory when investors are negative. It is when you find exuberance for stocks that most of the danger lies. With that said, the earnings of S&P 500 companies have been rising at a torrid pace that is likely not sustainable. The slope of the earnings curve is steep by historical standards, the impact of lower corporate income tax rates will soon be apparent in year-over-year reporting, and rising interest rates tend to act as a brake on economic expansion. Look for S&P 500 earnings growth to continue, but for the pace to slow.   We will likely enter a period when good economic news is interpreted as bad for the stock market-- as unemployment continues to fall, wages finally begin to rise, and federal reserve interest rate increases put pressure on mortgage rates and in turn the housing market. Bonds will continue to be a dangerous place to invest your money as rising rates cause bond prices to fall, and marginal borrowers have trouble issuing new debt at sustainable levels.   So, as we enter the final two months of the year there are plenty of reasons to worry, but as usual, the long-term prognosis for US equities remains positive.

Like a scary movie you have seen before, conditions will look dire for the hero, but ultimately things will work out in the end. Insurance Coverage: Basic Concepts Part of Oak Street Advisors’ 10 Financial Commandments for Millennials series, basic insurance knowledge will help you get the coverage you need and help clarify some misconceptions. Health Employer group health insurance plans are the most common option for young investors. Often, you don’t have much say in the plan, but the pricing is generally much cheaper for at least the employee, if not their entire family, than paying for private insurance through the Healthcare Marketplace. If you do have a robust menu of options in your healthcare and supplemental plans, it’s best to sit down with your advisor or HR department to discuss how you can optimize these features. If you’re paying for private health insurance, you likely have a high deductible health care plan. Using a Health Savings Account (HSA) you can reduce your taxable income, experience tax-free growth, and make tax-free purchases on qualified medical expenses. Talk with your financial planner to discuss how to set an HSA up and an appropriate strategy if investing inside the account. Auto Auto insurance coverage can often be boiler-plate, but you should understand these concepts. First, you only need personal collision coverage up to the value of your car; other vehicle collision coverage should be at least $50,000 to cover damage to a more expensive vehicle while at fault. Second, make sure you have enough “under insured motorist coverage. This is different from “uninsured motorist coverage” where you are paying for people who are driving around uninsured all together. Under insured motorist coverage makes up the gap between someone who has the bare minimum auto insurance and the actual money needed to pay for collision damage and medical bills. It is important to remember this is further protection for you, not any other motorist.  Life Insurance The basics of life insurance are broad, but we have shortened it down for you HERE. You should purchase life insurance to cover your family debts and provide income to survivors, if needed. In your life insurance calculation make sure to insure your home mortgage, kids’ college expenses, any other outstanding debts, and your final burial expenses. Often investors can self-insure some of this with their current retirement savings, but rarely all. Here’s a quick way to determine how much insurance coverage you’ll need to replace employment income for your family: Every $1,000,000 can produce $50,000 of income at a safe withdrawal rate of 5%. So add $1 million for every $50,000 of annual income you need to provide, $500,000 for every $25,000 etc. In general, if you’re not married and do not have any children- there is little reason for you to purchase life insurance. If you do need life insurance, I strongly encourage you to purchase term. Term is much cheaper and does what it’s supposed to do- insure you if you die. If you like paying an extra premium for no reason just to invest your money, you can purchase a whole life policy. These are expensive and laden with commissions and fees which are a conflict of interest to the salespeople who will try to talk you into purchasing these. Umbrella Policy An umbrella policy bridges the gap between your standard home and auto coverages and catastrophic costs. If something goes terribly wrong that you are liable for, this policy will usually cover the difference between your policy maximum coverage limits and $1 million- and can cover even more if need be. These policies are typically $150-$300 per year for the $1million coverage. For anyone building or maintaining wealth this coverage is too cheap to pass up. There is a reason on the CFP® students are taught that when in doubt regarding an insurance policy, the answer is always “recommend an umbrella policy”.   I have heard debt defined as work you have yet to do. Thinking of debt in this way highlights the need to be debt free in retirement. If retirement is to be a time when you no longer exchange labor for a paycheck, then you do not want ‘work you haven’t done yet’ to be in the equation. Carrying consumer debt like credit cards and home equity loans is the biggest no-no. It is important to remember that the safest and easiest way to earn 12% to 18% on your money is to not pay 12% to 18% for your money. Home mortgages are not as bad as consumer debt since you are financing an asset that will likely appreciate, or at least keep even with inflation. However, if you can eliminate that monthly payment you will find you can sleep better when you reach your retirement years. The two most common objections I have run into when recommending clients pay off a mortgage are: 1) They like the mortgage interest deduction when they file their income tax return 2) They like the security of having a large balance in their savings accounts. To which I explain: 1) The mortgage interest deduction only reduces the effective interest rate you pay, it does not eliminate it. Plus, your marginal income tax rate is likely to be lower during your retirement years anyway. 2) You are likely earning less on your savings than you are paying in mortgage interest, and even if you invested the money, you then end up with more assets at risk to market fluctuations during a part of your life when lowering your exposure to risk makes sense. Having a reasonable budget and the discipline to live within it is equally critical to your happiness and peace of mind during both accumulation and retirement phases. Having no mortgage keeps your monthly expenses low and which makes living within your means during retirement much easier. If all you really have to worry about is paying taxes, insurance, utilities, and for food you will find less stress in your life. So, based on your anticipated retirement date, you should develop a plan to eliminate as much debt and monthly payments as possible. It is much easier to develop and implement a plan in the years leading up to retirement than it is to address these needs after you have retired. If you need help developing a debt elimination plan, then reach out to us here at Oak Street Advisors, we have decades of experience helping pre-retirees fine tune their finances to make retirement less stressful and more enjoyable. Get Out of Credit Card Debt: Stop Giving Away Your Money Part of Oak Street Advisors’ 10 Financial Commandments for Millennials series, getting out of credit card debt is a crucial component for younger investors to get ahead. Interest payments can absolutely destroy your personal finances while often draining a debtors’ mental well-being as well. When used responsively, credit cards can offer convenience, flexibility, and lucrative rewards. When used inappropriately they can lead to life-changing negative consequences including bankruptcy and divorce. Therefore, getting out of credit card debt is the second step in our 10 Financial Commandments for Millennials series. Americans topped $1 trillion in credit card debt in 2017. At a 15.5% average interest rate, you don’t need to even run the numbers to know that’s a lot of money paid to the credit card companies. Average credit card debt is around $6,500 and climbing. Needless to say, if you’re in an uncomfortable situation with credit card debt just know you’re certainly not alone. So, how do you start to dig your way out of credit card debt? First and foremost, move as much debt as you can to a 0% card or account. You may have to open two 0% APR cards to do so, but you want to ensure you pay the least amount of interest on this debt as possible. Preferably you can find a card or transfer offer that doesn’t include a balance transfer fee. However, if you have to pay that fee understand that the money you’ll save on interest payments alone will more than make up for the 3% or so balance transfer fee. If you’re able to move the debt to a 0% card then calculate how much you need to pay each month to pay off the card by the time the zero interest period ends. If you can’t pay off the card in the allotted time frame, you still may be able to roll that balance onto another 0% card in a year or two when your current card’s 0% introductory rate expires. If you can’t get everything moved to an interest free credit card, you’ll need to start paying down your debt the old-fashioned way: being disciplined in your spending and allocating as much monthly income to your credit cards as possible. To do so, you can choose from one of the following methods: 1) Avalanche Method This method is best mathematically. The Avalanche Method dictates you pay all the minimums on your credit cards. Next, you throw as much extra money as possible at the highest interest rate account. This saves you the most money over time, but often can take a long time to pay off a single account which can be mentally and emotionally taxing. If you’re dedicated to crushing debt, saving the most on interest payments and will be extremely disciplined in tackling this problem then the avalanche method should be considered. 1) Snowball Method This method suggests that you pay all your credit card minimums just as the previous strategy, only instead of paying everything you can towards the highest balance account you take all extra payments and send them to the smallest account balance. You will pay more interest than the latter method, but eliminating the little accounts first provides debtors with small mental and emotional victories when an account is paid in full. In our experience this leads to a more motivated client who gains momentum with every account that is erased. While mathematically inferior, our advisors recommend clients utilize the Snowball Method. The small mental victories really power people through their debt elimination strategy and generally tend to keep people better on track. Of course, you can sit down with an independent advisor at Oak Street Advisors to discuss the best option to achieve your personal financial goals. If you’re tired of dealing with credit card debt on your own you can also check out our Fiscal Checkup which can be focused on restructuring and then eliminating your credit card debt with a financial planner.  |

Archives

September 2023

Categories

All

|

RSS Feed

RSS Feed