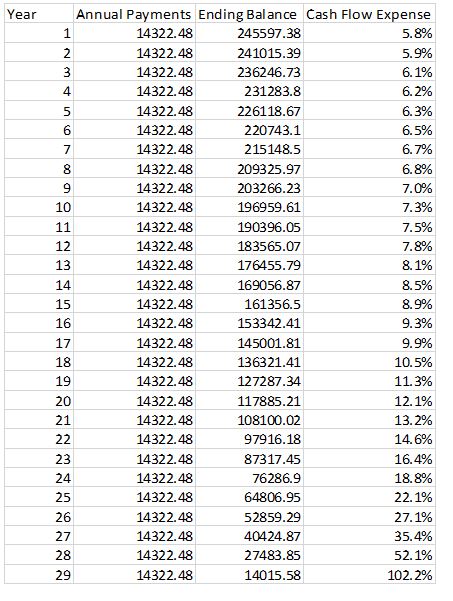

I have heard debt defined as work you have yet to do. Thinking of debt in this way highlights the need to be debt free in retirement. If retirement is to be a time when you no longer exchange labor for a paycheck, then you do not want ‘work you haven’t done yet’ to be in the equation. Carrying consumer debt like credit cards and home equity loans is the biggest no-no. It is important to remember that the safest and easiest way to earn 12% to 18% on your money is to not pay 12% to 18% for your money. Home mortgages are not as bad as consumer debt since you are financing an asset that will likely appreciate, or at least keep even with inflation. However, if you can eliminate that monthly payment you will find you can sleep better when you reach your retirement years. The two most common objections I have run into when recommending clients pay off a mortgage are: 1) They like the mortgage interest deduction when they file their income tax return 2) They like the security of having a large balance in their savings accounts. To which I explain: 1) The mortgage interest deduction only reduces the effective interest rate you pay, it does not eliminate it. Plus, your marginal income tax rate is likely to be lower during your retirement years anyway. 2) You are likely earning less on your savings than you are paying in mortgage interest, and even if you invested the money, you then end up with more assets at risk to market fluctuations during a part of your life when lowering your exposure to risk makes sense. Having a reasonable budget and the discipline to live within it is equally critical to your happiness and peace of mind during both accumulation and retirement phases. Having no mortgage keeps your monthly expenses low and which makes living within your means during retirement much easier. If all you really have to worry about is paying taxes, insurance, utilities, and for food you will find less stress in your life. So, based on your anticipated retirement date, you should develop a plan to eliminate as much debt and monthly payments as possible. It is much easier to develop and implement a plan in the years leading up to retirement than it is to address these needs after you have retired. If you need help developing a debt elimination plan, then reach out to us here at Oak Street Advisors, we have decades of experience helping pre-retirees fine tune their finances to make retirement less stressful and more enjoyable. Carrying mortgage debt can be a contentious subject among financial planners. Some look at the leverage as an opportunity to build net worth. Others see mortgage debt as merely a necessary evil. Often clients believe the mortgage interest deduction is valuable, but with the new income tax rules effective January 1, the deduction is limited for some and worth less for others. So when should you try to be mortgage free? Certainly, by the time you plan to retire. I have given this advice to everyone who has the means to do so, and to a person, they have always commented that it was the best advice they ever received. The reason has little to do with money, but everything to do with peace of mind. Not having the expense of a mortgage often reduces your need for significant cash flows. Being mortgage free also means that if push comes to shove, how much does it really take to live each month? Your basic expenses are then whittled down to food, energy, medical, and insurance expenses. Retirement is also the point in your life where growing your net worth takes a back seat to generating income. I explain to clients that the easiest and safest way to earn 4% on your money is to avoid paying 4% for your money. Paying off a mortgage can be compared to purchasing a bond with a yield equal to your mortgage interest rate. I like to illustrate the value of paying off your mortgage in a very simple way. Below is a chart of the annual payments for a $250,000 mortgage at 4% interest. We can ignore escrow amounts, because that covers expenses that will continue regardless of whether or not you pay off the mortgage debt.  Cash flow expense is simply the mortgage payments for the year divided by the payoff amount, or if you had the cash available to pay off the mortgage how much cash flow that money would have to produce to cover your mortgage payment.

You can see in this example that by year 15 the amount of money needed to pay off your mortgage would need to produce returns close to the historical equity market rates to be an even trade-off. By year 20 of a 30-year mortgage, or around the time many people are reaching retirement, the return on cash needed to make your mortgage payments has reached double digits. If you were retiring at that point and had $117,886 available in a taxable account I would encourage you to use that money to pay off your mortgage. With a cash on cash return of over 12% the odds of earning a higher return on that money is slim, and it gives you an extra ten years of a less stressful retirement. I once had a planning client come to me complaining that low CD rates were cutting into their lifestyle. The client felt they needed more income, but they were very risk averse. For them using the $100,000 to pay off their mortgage saved them from having $9,000 in annual expenses and did so without exposing them to any investment risk at all. Every situation is a bit different, but you should challenge your assumption that carrying mortgage debt in always a good strategy. |

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed