|

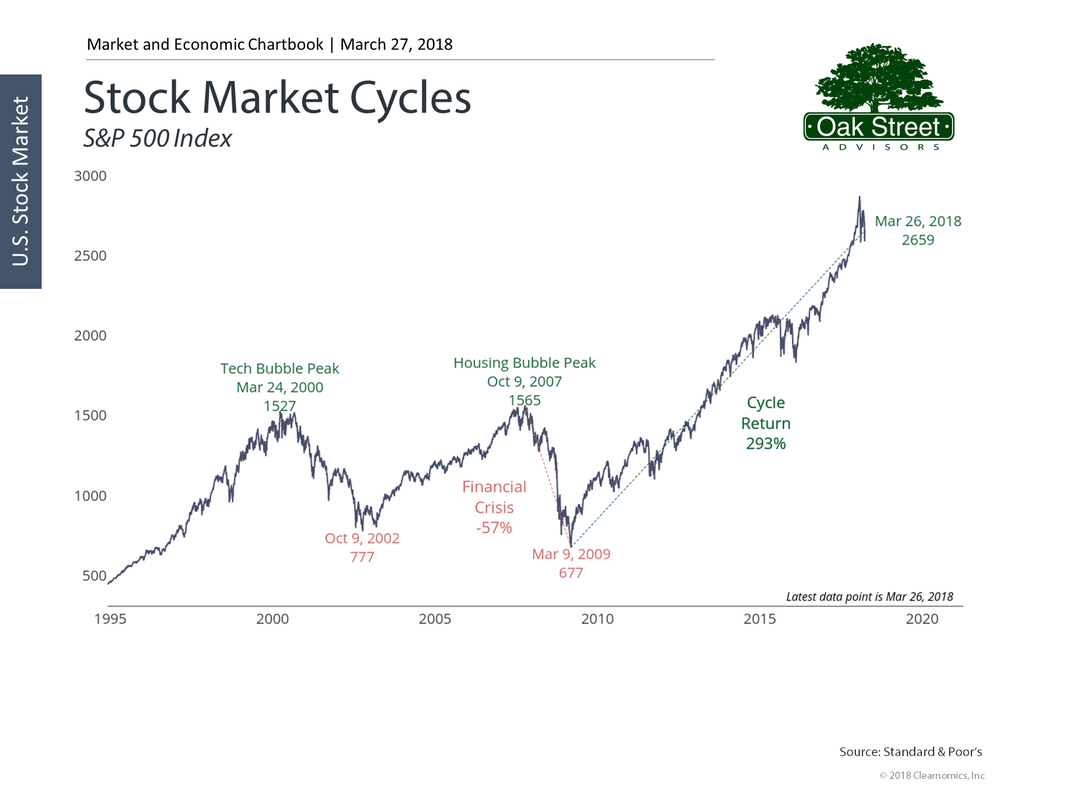

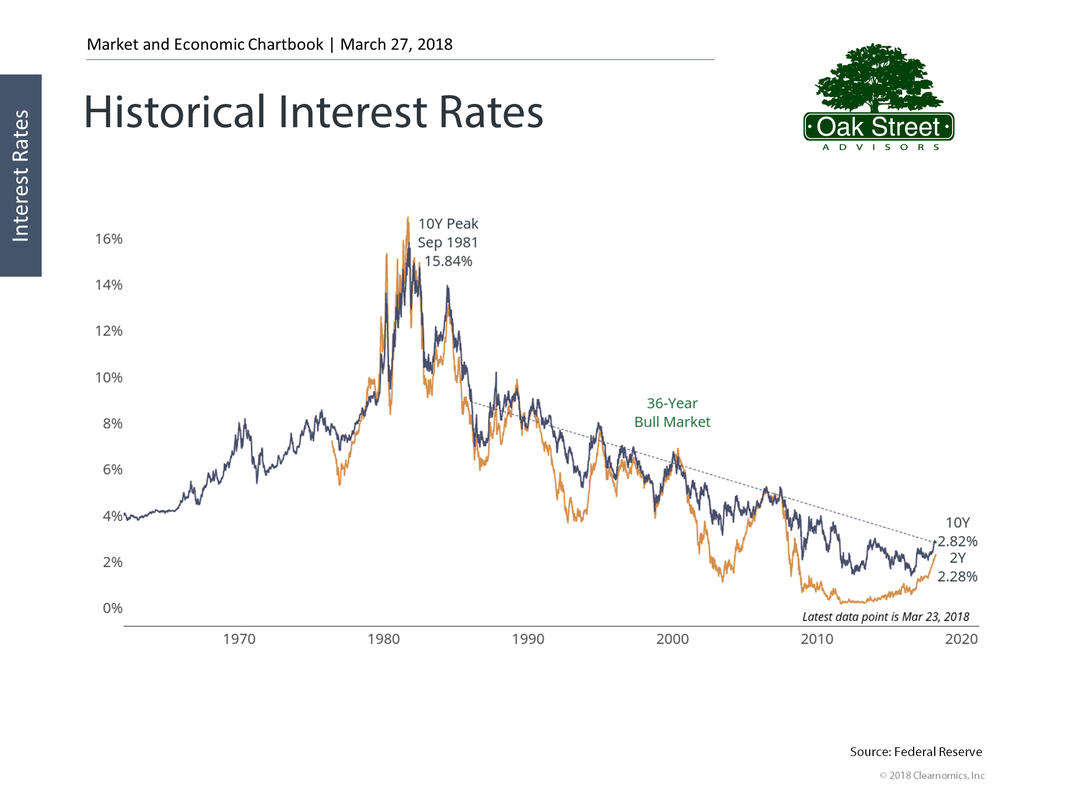

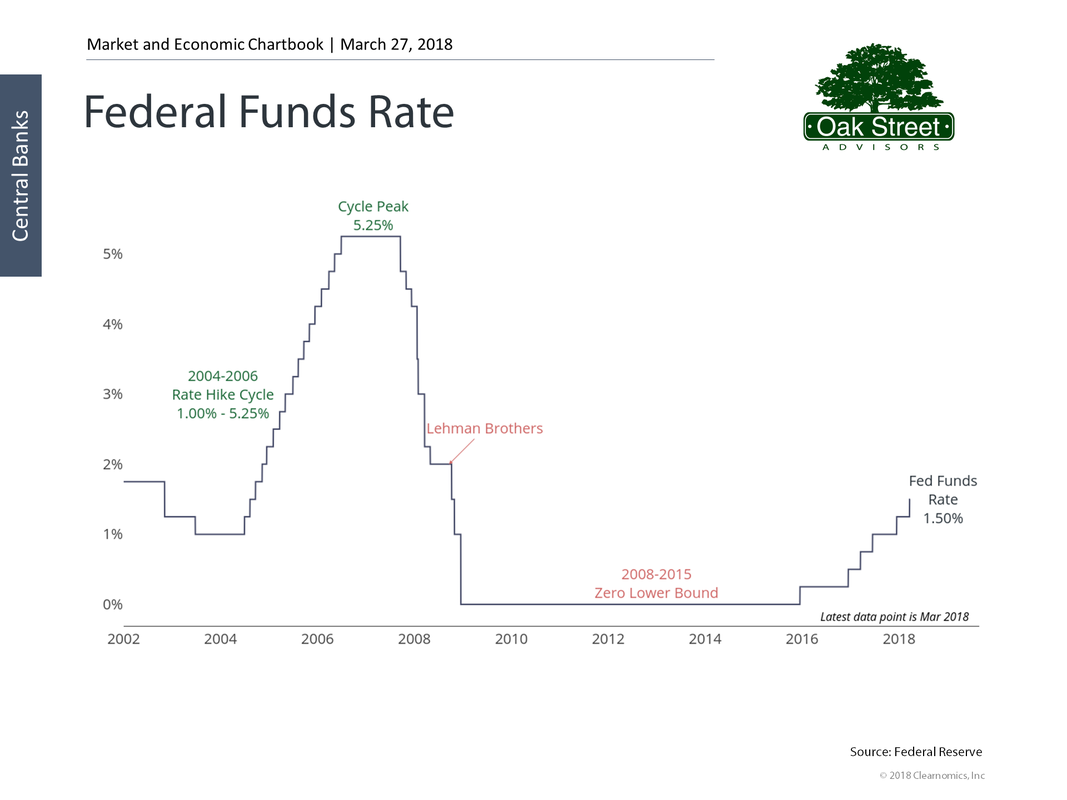

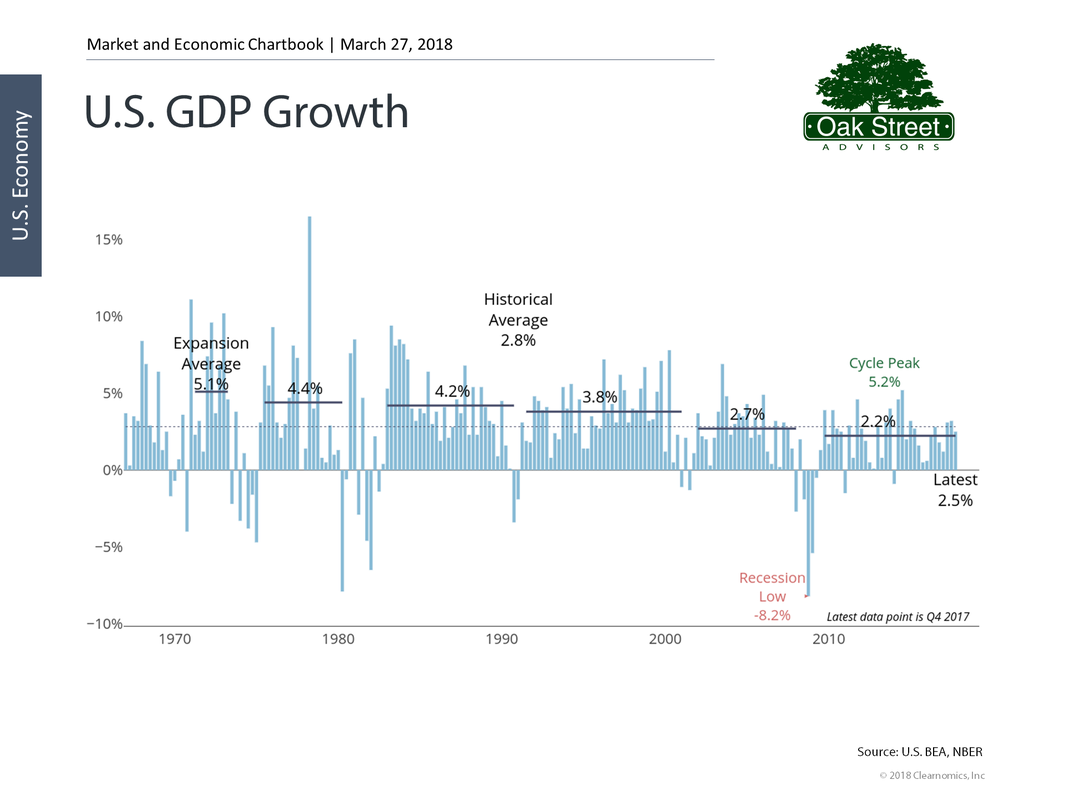

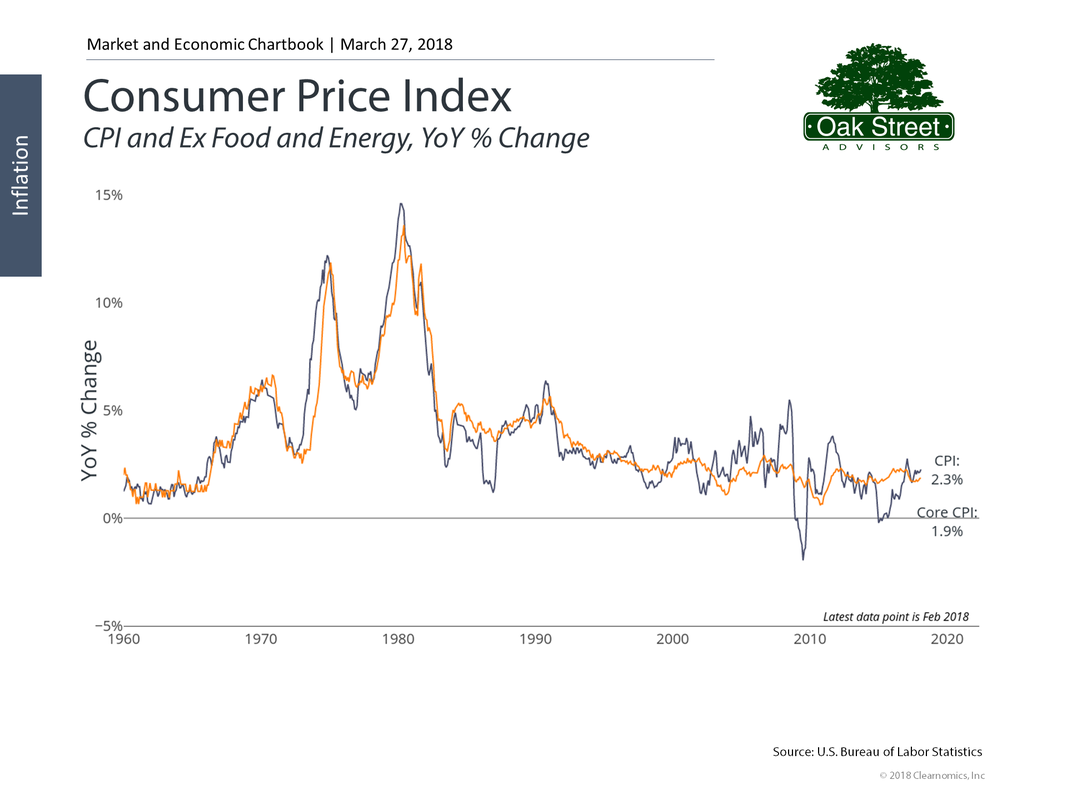

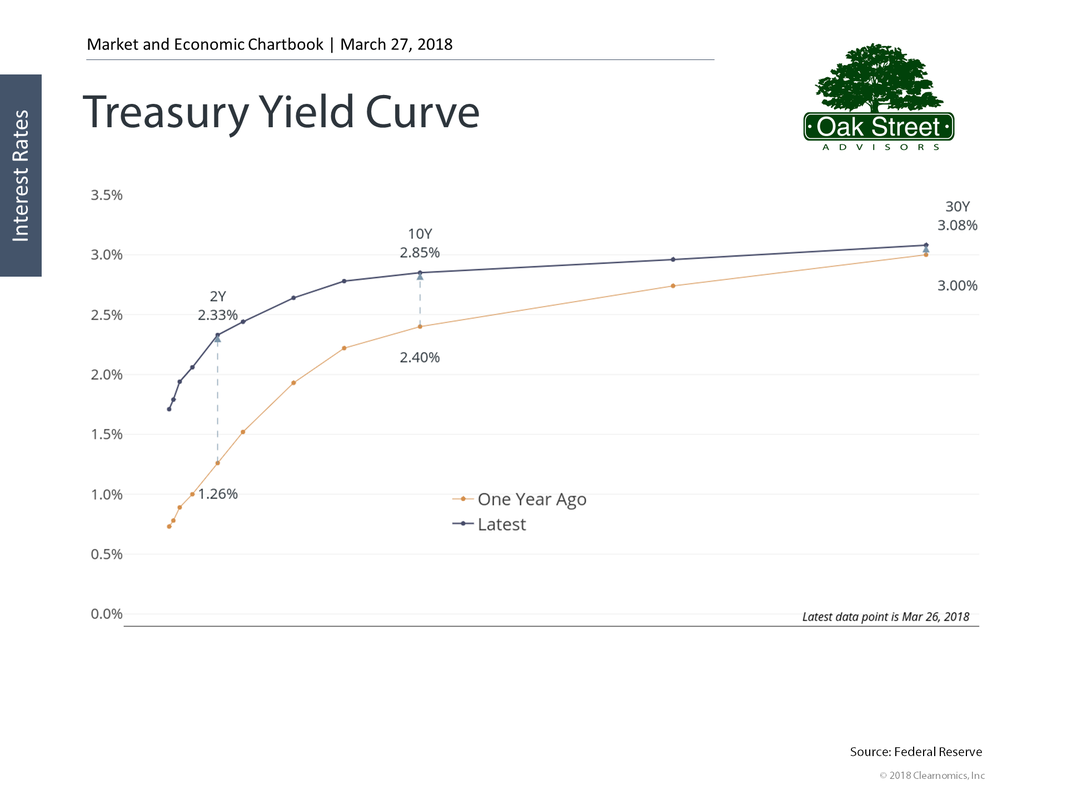

The popular press is fond of pointing out how old the bull market for stocks is. After bottoming in 2009 we have seen stocks march upward for for nearly a decade. Many of today’s younger investors, say those in their thirties, have seen the stock market fall, but never felt the pain in their own portfolio.  Yet for another class of investor, those who have invested in bonds, the bull market run has been even longer. Going back to the days of President Jimmy Carter in 1981, bond yields have fallen, year after year. Because bond prices move inversely to interest rates, bond prices have been rising for the last 36 years. That means someone who entered the workforce in the early eighties, bond prices have always gone up.  For some perspective the Certified Financial Planner Board of Standards was formed in 1985. As a group, CFP® practitioners have never experienced a true bear market in fixed income securities. Although the credit freeze that coincided with the great recession bear market for stocks, had a short, sharp panic in the fixed income markets; a long drawn out bear market for fixed income has been an experience the profession will for the most part find alien. The closest thing to the pain of a bear market in bonds experienced by this group was the 2004 to 2006 Chinese water torture of the Greenspan/Bernanke Fed. During the thirteen months that spanned June of 2005 to July of 2006, the Federal Reserve raised rates 25 basis points every time they met. Although the aggregate bond index only fell in price by about 5%, the constant barrage of interest rate increases was hard to live through. That pain was nothing compared to the Burns/Miller/Volker era where we saw the Fed raise rates from 4.75% in November of 1976 to the 20% Fed Funds rate of May 1981. That was the last true bear market for fixed income products in the United States. Although your grandfather might wistfully talk about getting 18% on his CDs, the path that led to those astronomical rates was littered with bond investors who saw the value of longer term bonds fall by 50% or more.  When I hear today’s press ask what will happen if the 10-year Treasury bond breaches 4% I am astonished. It is not a question of if, but a question of when. If we can avoid creating a trade war with the rest of the world, there are some very expansive monetary policies recently enacted by congress and the Trump administration investors can benefit from. The tax overhaul will provide a good measure of impetus to the economy, and the budget bill recently signed into law gets us away from the restrictive spending of the sequestration agreement and into a more expansive government spending era. Yet, the Federal Reserve must walk a fine line between economic growth and containing inflation. GDP growth has entered a more normal territory.  Inflation, while still subdued, has shown signs of rebounding. The uptick in inflation is related to a small increase in wage growth, which is in turn related to the continued implosion of our unemployment rate. You also will note a similar uptick in mortgage rates.  As investors search for yield in a low rate world, we have seen a compression in the interest rate spreads between high quality bonds and low quality (junk) bonds. With rates as low as they are today and with the economy growing it is inevitable that interest rates will rise. The end of the 36-year bond bull market is likely upon us. A flattish yield curve where the difference in a two-year treasury and a ten-year treasury is a mere 52 basis points, puts bond investors in a peculiar spot where an interest rate increase of just 1% could potentially wipe out three to five years of interest income.  The take away from all this is bonds are a minefield for investors today. A small misstep can be very costly and the rewards for investment are very small. Many advisors are ill-prepared for a world of falling bond prices.

Unless you or your advisor are true experts with fixed income investments, your best option in today's environment is to keep your maturities very short. That means you should be selling any bonds or bond mutual funds that have long durations. You should direct those allocations to short term treasuries, certificates of deposit, and bonds in the 1 to 3 year maturity range. Hopefully you will ladder those investments so you have new money available to invest at progressively higher rates throughout this interest rate cycle.  Stealing a page from Elliott Management, the $27 billion hedge fund founded by Paul E. Singer, who successfully sued Argentina for payment of defaulted bond issues, other hedge fund managers have been buying distressed Puerto Rican debt hoping for a similar payout.

The strategy works like this: Puerto Rico is known to be in dire financial straits. With the tax free debt of this US territory trading at large discounts hedge funds have been buying these bonds in the secondary market and hoping to convince congress to bail out Puerto Rico. Essentially they want the U.S. taxpayers to pay the full price for the bonds they bought for pennies on the dollar. Fortunately, legislation has just passed out of a house committee that would set up an oversight board to restructure Puerto Rican debt. Seeing that their gambit is slipping, the hedgies have resorted to buying ads that protest this restructuring and warning that states like Michigan could be the next to restructure their debt and pay less than 100% of bond obligations. These hedge funds conveniently forget that Puerto Rico is not a state. By remaining quietly in the shadows and using their political contributions to convince your congressional representatives to argue for them, they hope to turn your money into their money by political fiat.  You have heard of the importance of owning a diversified portfolio. For those who do not manage money professionally, the mantra to diversify by investment class is pounded into their heads by the consumer finance media and is rarely questioned.

The reason bonds are included in a balanced portfolio is usually to reduce the overall risk characteristics of a portfolio. For example, if an investor would be panicked by a short term 20% drop in the value of their holdings as reflected in their monthly statement, then we can add maybe 40% to the bond side, making it likely that a 20% drop in stock prices will only result in a 12% drop for that investors statement (.6 allocation to stocks X .2 short term drop in value). It is not that bonds offer superior returns, it is that bonds sometimes provide better returns than stocks with less volatility. The same reduction in risk can be achieved by holding cash and money market funds, but historically bonds have outperformed cash. Yet when markets enter periods of extreme turmoil like 2008 and 2009 the usual correlations of investment returns fly out the window and bonds can tank at the same time stocks tank. And when interest rates rise bond prices will fall. So my question to you is: Why do you own bonds? Are you afraid of the temporary drops in stock prices or are you just following the mantra of the popular press? With interest rates poised to rise would you be better off using cash as a buffer? Duration has a special meaning in the investment world. It is a measure of interest rate sensitivity in bond portfolios. You can calculate the duration for an individual bond or for a portfolio of individual bonds and you can derive an average duration. Why is this important? Because in a rising rate environment, like the one we are just entering, the duration will give you an idea of how much your principle will decline for a given increase in interest rates.

If your bond portfolio or your bond fund has an average duration of 6 years then you can expect the value of the portfolio to drop by about 6% for every 1% increase in interest rates. The Pimco Total Return Bond Fund with assets of around $246 billion dollars is one of the largest bond mutual funds in the United States. With an average duration of 5.26 years you could expect about a 5% drop in the funds value if interest rates rose by 1 percentage point. Or you could expect a 1.25% drop in value if interest rates rose by just 0.25%. Given that most bond funds have a yield of around 3% you can see that even small changes in interest rates can wipe out months of dividend income. So you should be aware of the duration of any bonds or bond mutual funds you own. Then ask yourself if the risk is worth the reward at this point |

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed