With the end of the year approaching, now is the time to look for opportunities to save on income taxes. Here are some items you should look for:

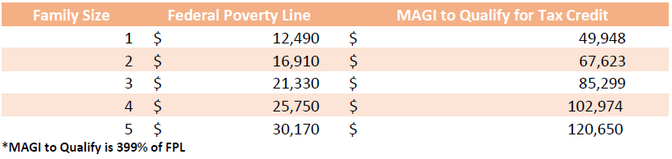

In Charleston and Myrtle Beach, clients and potential clients often assume the Affordable Care Act (ACA) only helps low earning individuals and families. This is far from the case. When using proper financial planning strategies, some families can make up to $239,000 and still qualify for the healthcare subsidy. Over 10 million Americans utilized Affordable Care Act (ACA) healthcare insurance in 2018, 87% of which received some sort of subsidy to help them pay for that insurance. Many receiving that subsidy don’t understand the how and why of the program; and many who aren’t receiving the subsidy don’t realize just how close they may be to pocketing thousands in tax relief via the Premium Tax Credit. We’re going to walk you through a broad overview, without getting into too much detail, so you may determine if you can qualify for the Premium Tax Credit and what strategies you can implement to help you qualify. Who qualifies for tax relief from the Affordable Care Act in 2020?  How do you determine your Modified Gros Income (MAGI)? Start with Gross Income which, for simplicity, is any income you receive throughout the year. Next, you’ll need to determine your Adjusted Gross Income (AGI). You’ll do this by subtracting:

Finally, to determine your MAGI, add-back to your AGI:

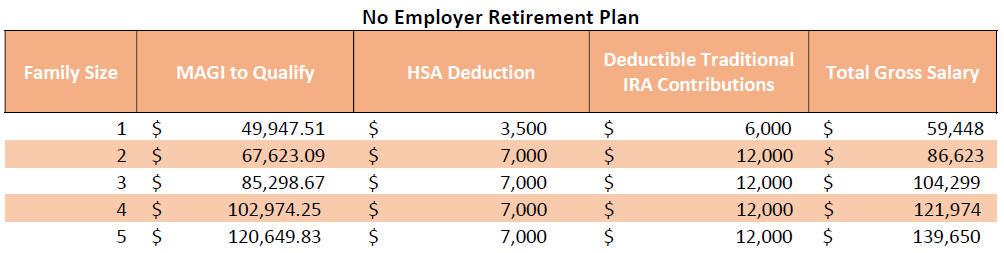

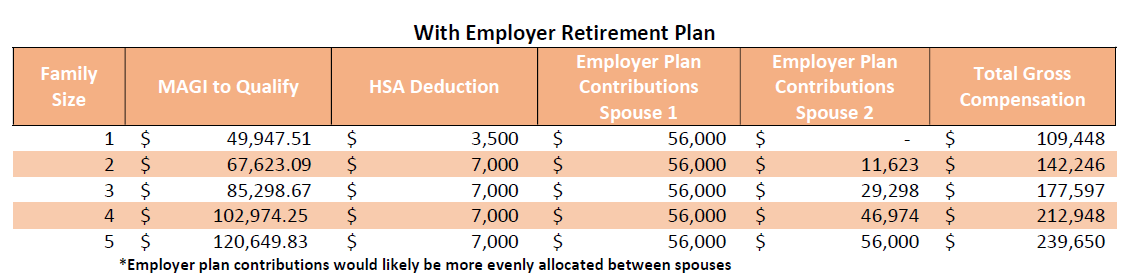

We see that for most people, the only way to lower your MAGI number is to increase the deductions that calculate your AGI, such as 401k (or any qualified employer plan), IRA (SEP, SIMPLE, Traditional) and HSA contributions—therefore we use these deductions in our general example below. Theoretically, the following gross compensations can be earned with corresponding contributions reducing overall MAGI:   Often families cannot afford to, or choose not to, dedicate the maximum amounts to these accounts. We recommend establishing a strategy each year for qualifying for the Premium Tax Credit that matches your personal and financial goals.

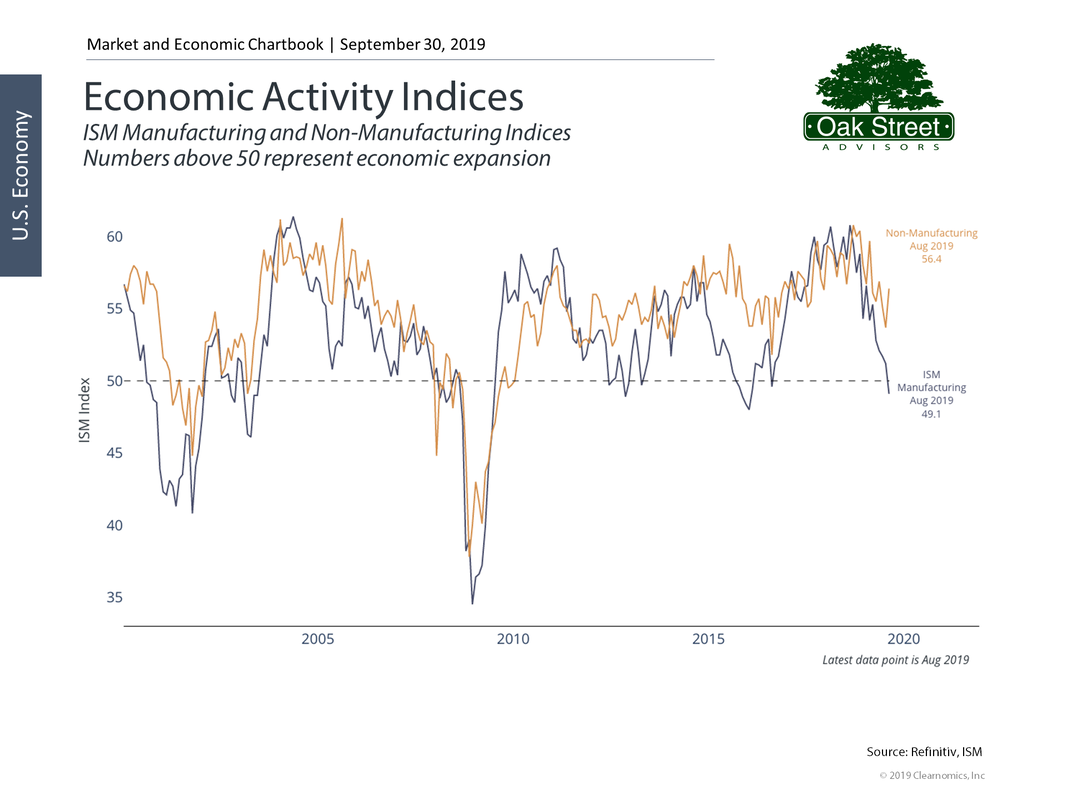

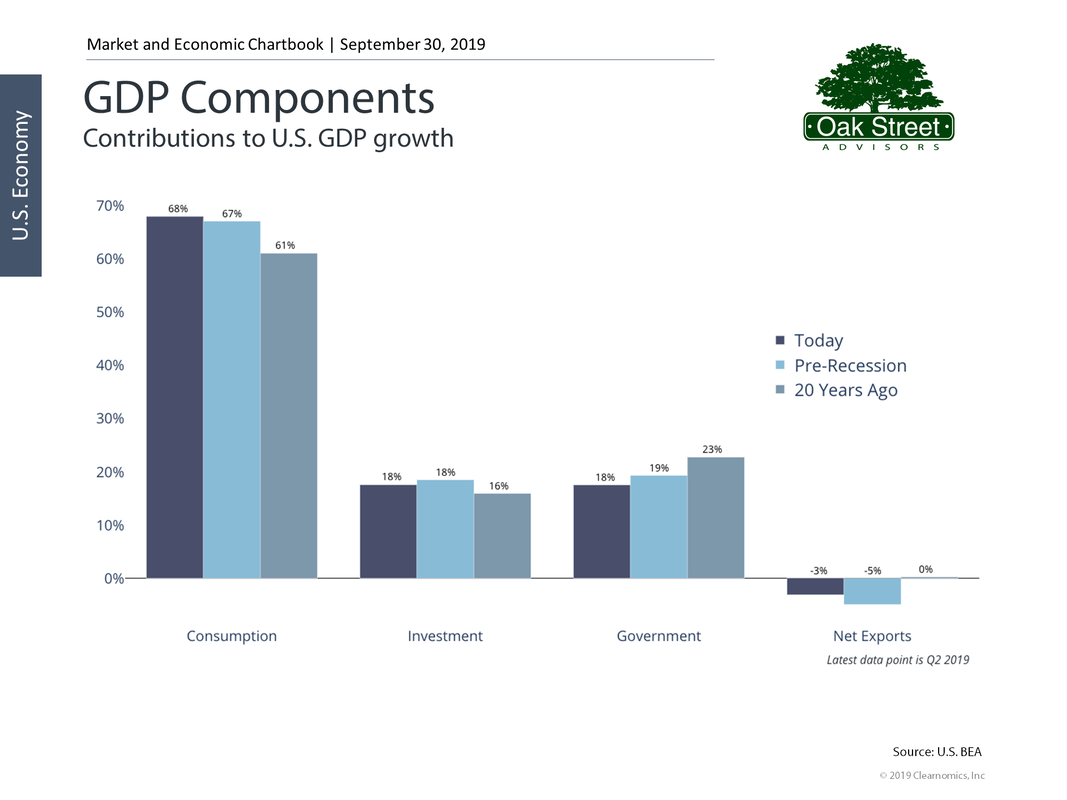

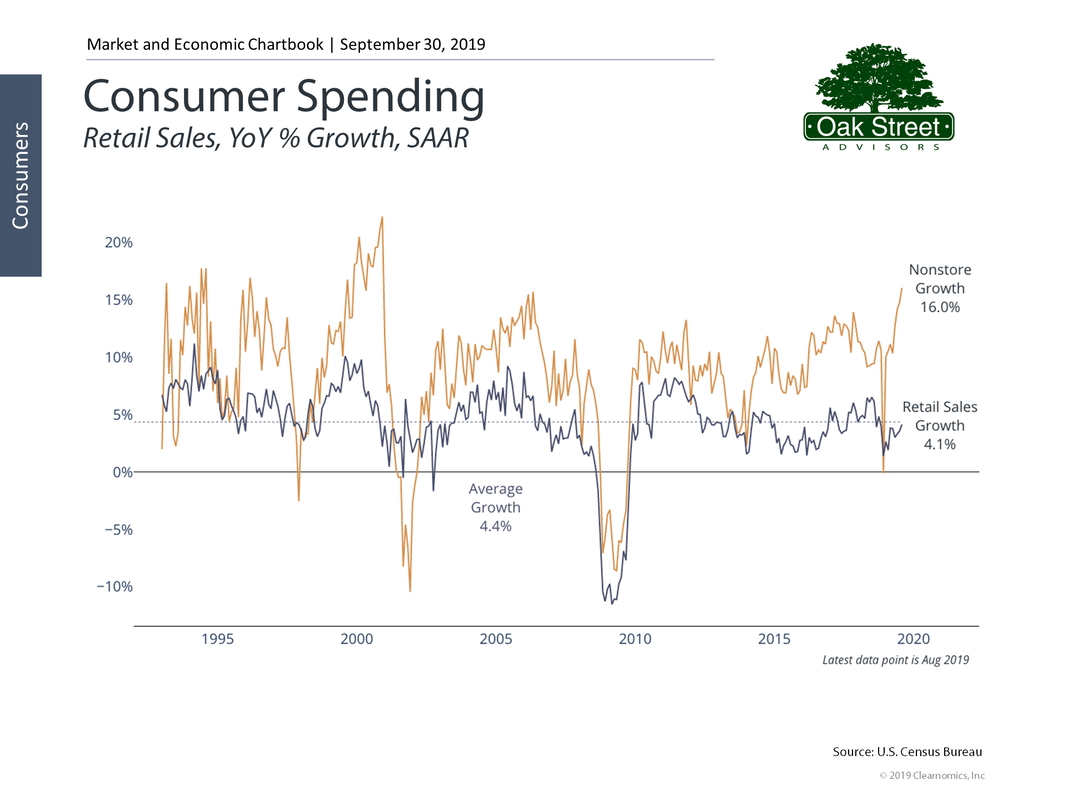

Keep in mind, this is a general overview. There are many other rules that can change these calculations, such as non-working Spousal IRA contributions which phase out at certain income levels and the catch-up provisions afforded to anyone over the age of 50 for IRAs and 55 for HSAs; The goal of this article is to give a broad overview so you may pinpoint exactly where your family sits in reference to the Premium Tax Credit eligibility. If you’d like a CERTIFIED FINANCIAL PLANNER™ to help create and manage a tax strategy that will aims to qualify your family for the Premium Tax Credit click here. By James Liu, CFA Some investors and economists have been worried about a recession for some time. This is only natural after over a decade of steady economic growth and the spectacular rise of both stocks and bonds. On the one hand, the economy is still quite healthy by many measures, especially based consumer spending and the labor market. On the other hand, there are clear signs that industrial and corporate activity have slowed. One important measure of economic activity, the ISM manufacturing index, suggests that manufacturing activity has been slowing over the past year and actually shrank last month for the first time in three years. However, this alone is not a reason for investors to panic. First, manufacturing activity is directly affected by the on-going global trade disputes. Uncertain and reduced demand for U.S.-made goods will continue to be a drag on industrial activity until firm trade agreements are in place. Second, the corresponding non-manufacturing index has also slowed but is still expanding at a strong pace. This suggests that business activity overall would still be healthy if not for these global effects. From the perspective of GDP growth, the contribution from corporate investment has fallen since the financial crisis. This is partly because investment spending by many companies has been weaker than in past cycles. The underlying reasons for this are unclear, but they likely include slower economic growth trends compared to previous business cycles and improvements in technology. Regardless, what has increased over time is the share of GDP growth from consumer spending. Not only do consumers (on average) have strong balance sheets, with total net worth at record levels, but their spending has maintained a healthy pace. Of course, not all consumers are doing as well as they were one or two decades ago. But from the perspective of corporate profits and the stock market, the consumer is still the cornerstone of the economy. Thus, while the overall economy may be slowing, this is because we're now in the eleventh year of the business cycle and global trade disputes have created an environment of uncertainty. Manufacturing activity has decelerated but consumer spending is still strong. Here are three charts on this important topic: 1. U.S. manufacturing activity shrank last month  The chart above shows the ISM manufacturing index. This is a "diffusion index" which means that values above 50 represent expansion while those below 50 imply contraction. Thus, the index shows that manufacturing activity shrank in August for the first time in three years. While this index has been slowing for over a year, on-going trade uncertainty has dragged it down further. Fortunately, the non-manufacturing index still shows healthy expansion. 2. Investment spending has fallen over the past decade GDP Components  Investment spending by companies has fallen as a share of U.S. GDP growth over the past decade. This is in contrast to consumer spending which has increased. 3. However, consumer spending is still healthy Consumer Spending  Consumer spending continues to be healthy despite economic uncertainty. Non-store sales (i.e. online retailers) has increased at an even more rapid pace, a sign of shifting consumer trends over the past two decades.

What's the bottom line? The economy is slowing in part due to shrinking manufacturing activity, driven in no small part by trade disputes. Despite this, other parts of the economy are still quite healthy. Investors should maintain a broader perspective on economic growth. With nursing home care running north of $68,000 per year, many families who have a "comfortable retirement" could find themselves facing the prospect of spending down a large chunk of their savings and investments should the need for nursing home care arise. Without long-term care insurance some will find their only option may be to apply for Medicaid assistance.

While Medicaid rules vary from state-to-state, typically a person needing long-term care benefits must spend down their assets to $5,000. If there is a surviving spouse, they can usually keep the family home (but states can consider home equity in excess of $500,000), a prepaid burial plan, and between $50,000 and $100,000 in resources. Cost For couples aged 60, the average cost of long-term care insurance runs about $3,500 per year. For many this is expensive; some alternatives you might consider are long-term care annuities and life insurance policies with long-term care riders. Regardless of cost, you should shop for a policy from a company with the financial stability to pay a claim if it becomes needed. Limiting your coverage and extending the waiting period can help reduce costs as well. You should choose a policy that meets your needs and include in-home care and policy triggers that are reasonable. A report from the American Association for Long-Term Care Insurance suggests that for the majority of policy owners, three years of coverage is sufficient. With high cost of coverage, the primary reason for not having coverage this study suggests that some coverage is better than none, and for most, is all that is needed. What Triggers Your Long-Term Care Benefits? Most companies will pay benefits if you are unable to complete two of the six activities of daily living, which include:

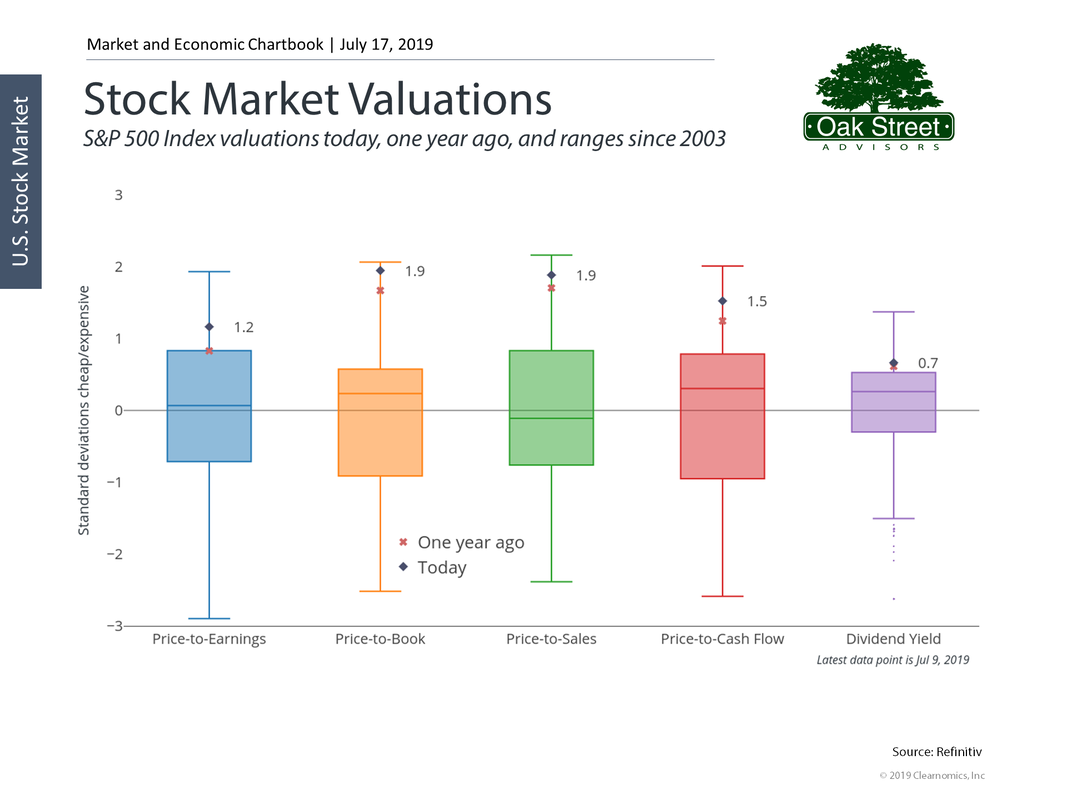

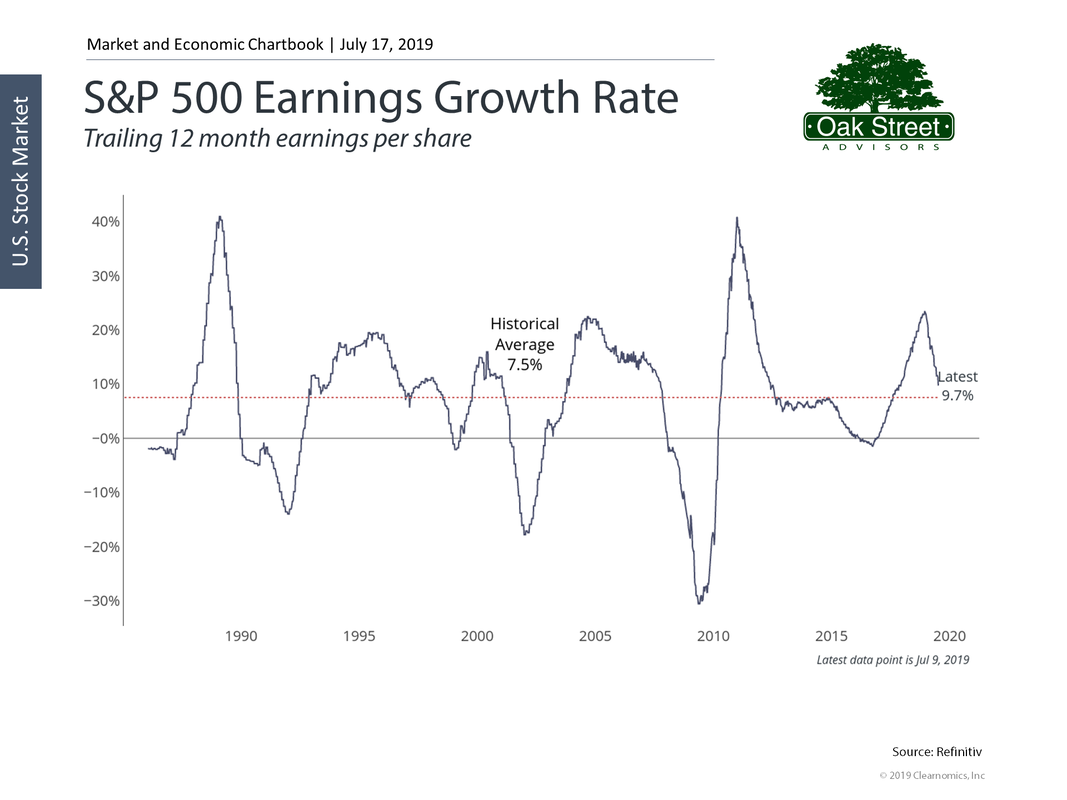

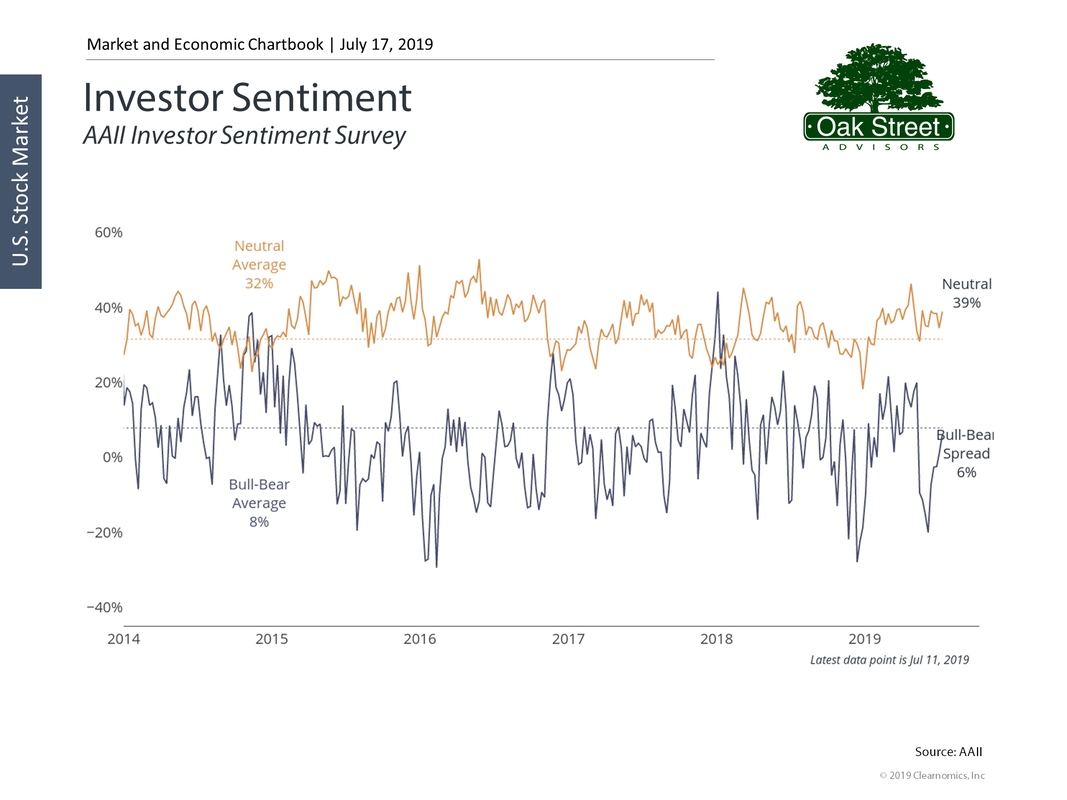

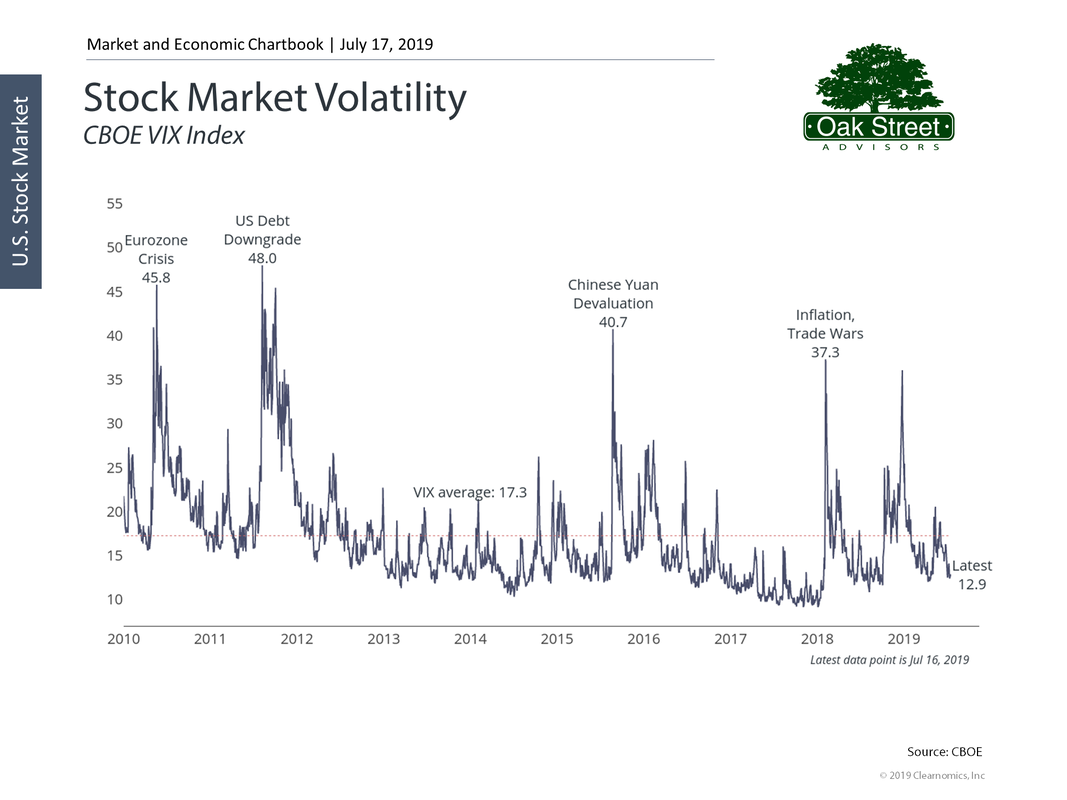

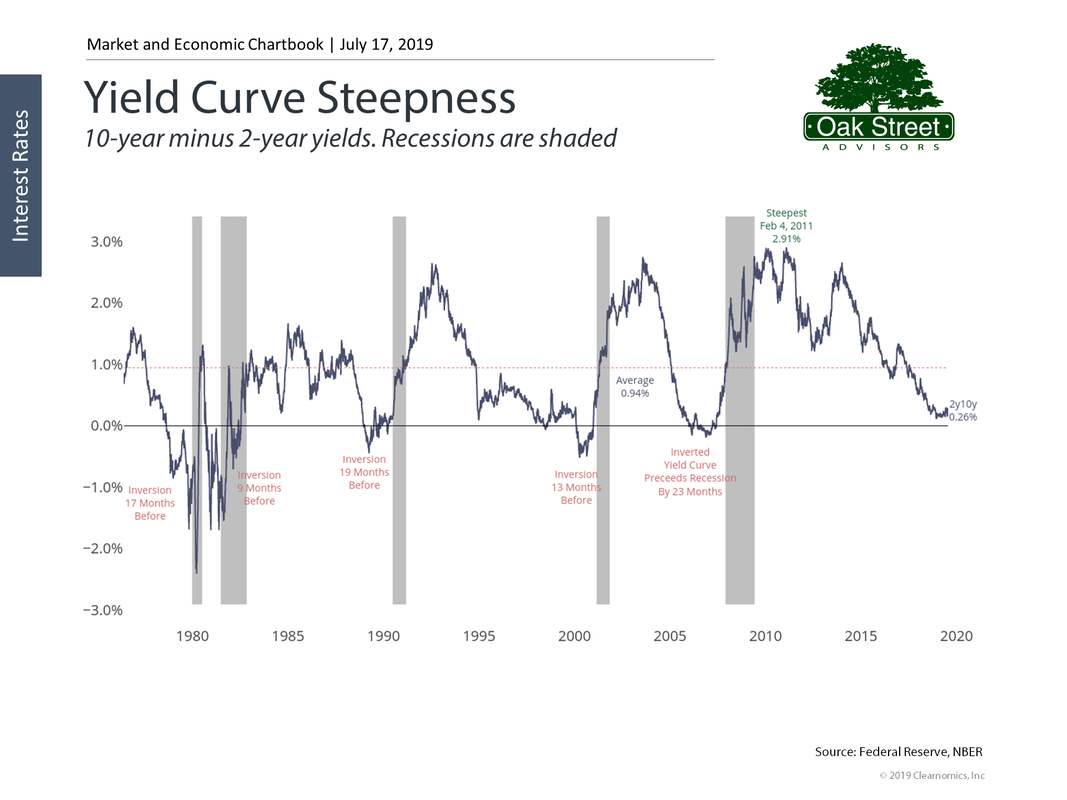

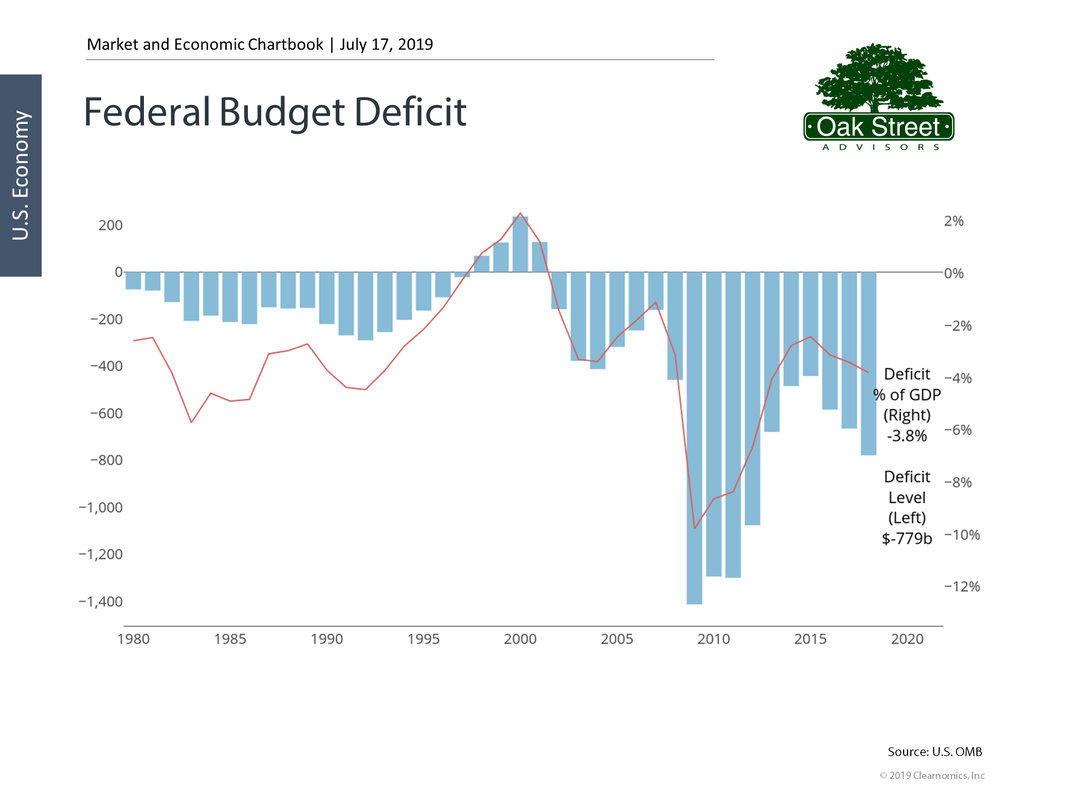

Or if you have severe cognitive impairment. When Do Benefits Begin Often long-term care policies have an exclusion period before benefits will begin. There can be some flexibility here if you have the resources to pay for some expenses yourself, for a few months. The most common exclusion period is 90 days. That means you would pay the first 90 days of expenses out of your pocket. This is reasonable and ties in with Medicare, who will generally cover the first 90 days of care if you are in a nursing home for something you are expected to recover from, such as surgery or a stroke. What Long-Term Care Insurance Covers Virtually all policies are comprehensive plans, which cover care provided in many settings: at home, adult daycare centers, assisted living facilities, nursing homes, and Alzheimer’s facilities. A home care benefit will typically cover skilled nursing care and occupational, speech, physical, and rehabilitation therapy. Most importantly, it can help with personal care, such as bathing and dressing. Where to find Long-Term Care Facilities You may at some time in your life be involved in selecting a nursing home facility for a loved one. The US Department of Health and Human Services Medicare site now has a feature called Nursing Home Care Compare. You can use this site to find and compare nursing homes by state, zip code, county or name. Once you have found nursing homes in your area you can view information on the quality of care provided. Each home is compared to the state and national averages for each category; for example, the number of nursing staff per-resident, per-day; or the percentage of residents who are physically restrained. Although the grading is measured against negatives and a little confusing (it seems a lower score is better), it is an excellent resource and a good place to start should you ever need nursing home facilities. It’s been a stellar start to the year. The S&P 500 has risen nearly 20%--crossing the 3,000 mark for the first time on June 12th, 2019.  Stock market valuations are getting a bit high and investor confidence remains unchecked.   While corporate earnings growth is slowing.  And as a contrarian indicator, investors remain very upbeat about the market…  …while volatility remains low.  The Fed seems to be caving to political pressure and markets believe we’ll get one or two rate cuts during the second half of 2019. The yield curve has avoided a major inversion as short-term rates have continued to fall.  Other things that we find worrisome: Treasury Secretary Mnuchin indicated the government may run out of funds by early September. However, Congress is scheduled for a summer recess and politicians seem to be more divided than ever so the Federal budget could become a big deal.  Although the markets seem to have priced-in an easing of trade tensions, there may be no quick end to the US trade war with China  Here’s What Oak Street Advisors is Doing Now:

When making any decisions we need to ask ourselves “Can I afford to be wrong?”. The long-term lesson of the markets dictates that our default position should be fully invested. The markets may go down-- but they do not stay down-- and the price of the permanent ups is the short-term downs. With that said, and knowing we may be wrong, we have made some changes to our stock portfolios. We’ve taken about 10% out of the stock allocation in the equity portion of your portfolio and are holding those funds as extra cash positions. This means if the stock market were to gain an additional 10% from now until year-end, we would only achieve a 9% gain. However, if the market were to pull back from here by 10%, we would only fall the same 9% and would have cash available to reinvest at lower prices. Only time will tell if our caution is justified. Note. This information does not constitute investment advice. It is merely posted so clients can understand the thought process that goes into managing their portfolios. Each individual’s circumstances and needs are unique. No one can predict the future or the valuation of any financial market with accuracy. Often, navigating the Social Security Administration’s rules can be complex and confusing. None more so than trying to determine a surviving spouse’s social security benefit. Nearly every couple will face this problem at some point.

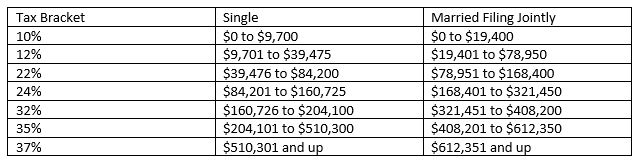

Timing is everything regarding social security surviving spouse benefits. The filing date alone—when you decide to claim social security and when your spouse does—ultimately determines how much you both will receive in Widow or Widowers benefit. Getting your initial claiming strategy right is paramount to maximizing this important benefit. If the deceased spouse has not begun receiving social security income at the time of death, the survivor’s benefit is based upon the decedent’s primary insurance amount (their social security income at Normal Retirement Age) plus any delayed retirement credits up to the date of death. Delayed retirement credits add about 8% to the social security income received for each year you delay taking your social security benefit beyond your normal retirement date, up to age 70. If this is the case the surviving spouse’s decision to claim social security benefits will be based on their age at the time they file. What this means is if the survivor decides to receive social security income before they reach their normal retirement date, there will be a reduction in income for each year of early filing, even if the deceased spouse had earned delayed retirement credits. If the deceased spouse had been receiving social security income before their normal retirement date, their benefit and the widow(er)’s benefits are reduced forever, depending on when the initial benefit claim was filed. Generally, you would lose about 8% of social security income for each year you receive social security payments prior to reaching your Normal Retirement Age (NRA). A widow(er)’s benefit is limited to the larger of 82.5% of the deceased spouse’s death primary insurance amount or the reduced income benefit the deceased would have been eligible for if they had lived. The Social Security Administration provides the following example: “Mr. B, age 64 on August 3, received reduced retirement income benefit of $350 (primary insurance amount $374.90) for August and September. He died in October. Mrs. B, age 66, comes in, to file for widow's benefits. The retirement income benefit if Mr. B were alive would be $350. 82 1/2 percent of the death primary insurance amount is $309.20 ($374.90 X .825). The life and death primary insurance amounts are the same. The widow’s income benefit will be the higher of the two, $350 in this example.” Your widow or widower can get benefits at any age if they take care of your child younger than age 16 or disabled, who’s receiving Social Security benefits. If the surviving spouse is disabled, benefits can begin as early as age 50. Unmarried children, younger than age 18 (or up to age 19 if they’re attending elementary or secondary school full time), can also get benefits. Children can get benefits at any age if they were disabled before age 22. Under certain circumstances stepchildren, grandchildren, step-grandchildren, or adopted children may also be eligible for benefits. These circumstances are exempt from the deemed filing rules and do not affect future claims made under their own work record. There is a family maximum to survivor benefits that will vary between 150% and 180% of the deceased worker’s benefit amount. For divorcees who had been married for ten years or longer, the survivor benefit is available if they have not remarried before age 60. An ex-spouse’s survivor benefit has no effect on the family maximum benefit, so a new spouse and any children can still be eligible to receive survivor benefits based on the same wage earner. Although a widow may be eligible for benefits based on their own work record, if they file for social security benefits, they will receive the highest benefit they qualify for at the time they file. Some benefits are calculated independently with the larger benefit being paid or the smaller benefit being paid plus the excess amount of the larger one. Other types of benefits are calculated with a carry-over reduction amount from the first benefit to the second. Although the loss of a loved one is a terrible time to assess and compare your social security filing options, it is important that you choose wisely. If possible, delay the decision until you have had the time to be emotionally ready to face the problem and consult with a trusted financial planner. Part of Oak Street Advisors’ 10 Financial Commandments for Millennials series, we discuss how lifestyle creep can lead to poor financial decisions and possibly ruin; and how keeping what really matters to us in life in the forefront of our financial lives can steer you away from conspicuous consumption. “Money has never made man happy, nor will it, there is nothing in its nature to produce happiness. The more of it one has the more one wants.”- Benjamin Franklin I agree with the last sentence, but there is no doubt that money can buy some happiness. Studies show that earning $75,000 annually buys happy; and $95,000 annually buys really happy. Taking that into account, the final financial commandment to conquer is a self-assessment of the way you spend your money. Do you spend more on the things that really matter in life-- providing protection for your family, ensuring you have enough assets in retirement, and making memories with the ones you love? Or do you spend more on that new car payment, credit card debt or eating out every night?  Keeping up with the newest trends, cars, boats—you name it, is expensive. You need a safe car your family can rely on, but does it need to have 8 temperature-controlled zones, leather seats with warmers and a sporty trim package? Your family will always need clothes on their backs, but a shirt from Target or Costco provides the same warmth as the one in the mall that costs over $200. Some of the wealthiest families somehow find a way to spend every penny earned with little to show for it in the end. When you reach the final commandment it’s time to take an honest introspective look at yourself and your household to make sure you’re spending your money in a deliberate way, on things that really matter and build your wealth into the future. You can control your money, or your money can control you.  Okay-- you just completed your income tax return for last year. You want to file it away and not worry about taxes until next year, but before you do-- take a look at your completed return to identify ways you can save tax dollars next year. Income tax planning can add to your future net worth and your future income streams. Here is a line by line view of some of the things that good income tax planning can do to improve your financial life. Taxable Income Line 10 on your new 1040 return shows your taxable income after all deductions. Knowing your marginal income tax rate is the first step to efficient income tax planning. Lowering your income taxes in the current tax year is not always the best long-term strategy, lowering your lifetime income tax liability is often much more important.  For 2019, the federal income tax brackets for individuals are:  Your marginal income tax rate is the amount you would pay on your last dollar. For example, a single person with taxable income of $84,201 would pay a 24% rate on only one dollar of income, not their total taxable income. They would in fact pay 10% on their first $9,700 of taxable income, then 12% on the next $29,775, then 22% on the next $44,725, and finally 24% on the last dollar of taxable income. It is important to remember that the current income tax rates for individuals are scheduled to revert to the pre Tax Cuts and Jobs Act rates in 2025. Barring tax changes passed by Congress in the interim, you have six years to utilize the current brackets to your benefit. Managing Your Income Tax BracketDepending on your income level, managing the income tax bracket you fall in may mean realizing extra income to take advantage of a favorable rate; or you may want to lower your taxable income to qualify for a lower tax bracket or other income tax benefits (such as Obamacare). In my opinion the 12% bracket is extremely valuable. Married couples can have up to $78,950 of taxable income and pay no more than 12% in federal income taxes. Less than 25% of American households have taxable income above this level and I believe the odds of their marginal income tax rate falling is quite small. If you are among the many that fall into the 12% rate, you should look for ways to pay taxes on as much income as you can without moving into the 22% bracket. Some of the things you should consider are: Contribute to a Roth IRA or Roth 401k rather than a Traditional IRA or standard 401k account

Convert existing Traditional IRA funds to a Roth IRA

Higher marginal income tax payers will want to take the opposite approach. They’ll want to defer more income unless they anticipate being in an even higher bracket in future years. High bracket individuals will want to:

The absolute worst taxable income numbers are $200,000 for single filers and $250,000 for joint filers; along with $157,500 for single filers and $315,000 for joint filers who own their own business. The first range, $200,000 single and $250,000 joint subjects a taxpayer to the 3.8% net investment income tax. The second range for self employed filers of $157,500 for single and $315,000 for joint are the cutoff for the pass-through business income deduction. Taxpayers at those levels should take aggressive steps to lower their taxable income. Investment IncomeMoving back up your return, line 2 and line 3 deal with investment income.  Note that these lines have been subdivided into an A and B column. The column on the left is better than the column on the right for income tax purposes. Tax-Exempt Interest On the left you have tax-exempt interest, which is income generated from municipal and state government entities. Municipal bond interest is generally income-tax free, although there are some taxable municipal bonds, and some municipal bond interest is subject to the Alternative Minimum Tax. Tax-exempt interest is also added to your Adjusted Gross Income (AGI) for purposes of calculating how much of your Social Security benefits are taxed. The higher your marginal income-tax rate, the more valuable tax-exempt interest is. To determine the taxable equivalent yield of a tax-exempt security, you divide the tax-exempt yield by 1 less your marginal income tax rate. For an investor in the 12% marginal income tax bracket, a municipal bond yielding 2.5% gives them the same after-tax return as a taxable security that yields 2.8% (.025/ (1-.12)). For an investor in the 32% tax bracket the same 2.5% yield from a municipal bond equates to a 3.6% taxable yield. Qualified Dividends Again, the column on the left is more valuable than the column on the right. A qualified dividend is a dividend from a company that: a) trades publicly on a US exchange and b) is incorporated in a US possession or c) is eligible for the benefits of a comprehensive income-tax treaty with the US. The advantage to generating qualified dividend income is that these payments are taxed at your capital gains rate, which is generally much lower than the rate on your ordinary income Dividends from REITs, MLPs, employee stock options, tax-exempt organizations, money market accounts, and shares used for hedging are not eligible for qualified dividend status. Make sure to also consider the treatment of preferred stock dividends. Although ranked below bondholders in the event of financial difficulty, preferred stock pay yields that are similar to long-term bonds. All taxpayers should consider these securities against table bond holdings for the tax advantages alone. IRAs, Pensions, and Annuities Income received from pensions and some annuities are absolute, in that you receive the income and you pay the taxes; however, income from an IRA and certain types of annuities are somewhat discretionary. You can plan the timing and the amount you withdraw to achieve the best income-tax outcome for your personal needs. If you are over 70 ½, you are required to take some distributions from your traditional IRA accounts (required minimum distributions/RMDs), but even then you can take advantage of the Qualified Charitable Distribution rules to lower the amount that is reported to the IRS. Income derived from variable annuities can be problematic for some. All income from variable annuities is considered ordinary income until you have spent down those assets to your cost basis. At that point, the withdrawals are deemed to be return of principal and are no longer subject to income taxes. Although we prefer to use IRA to Roth IRA conversions to manage income tax brackets for those in the 12% marginal tax bracket, you can certainly use variable annuities in a similar fashion. If you are in a higher marginal tax bracket, you can also consider exchanging your variable annuity for an immediate annuity. Doing this will change the deemed ordinary income rule to a pro-rata distribution rule, where some of your distribution is considered ordinary income and some of it is considered a return of principal. Social Security You probably will pay taxes on some of your Social Security benefits. If your total income is more than $25,000 but less than $34,000 for individuals; or $32,000 but less than $44,000 for joint filers, you will pay income tax on 50% of your Social Security benefit. If you are above those ranges, you’ll pay income tax on 85% of your Social Security benefit. Sadly, I have to say I have seen cases where an individual is less than 70 years old, in a 30%+ marginal income-tax bracket, saving money, and still insists on claiming their Social Security benefit. It would be a simple fix to suspend Social Security benefits, reduce their taxable income, and accrue delayed filing credits to their future social security income. Yet some will still continue those benefits because they feel they have paid in all their life and want to see some return on their money. Yes, you could die, but throwing away money paying needless taxes is hard to understand. Additional Income and Adjustments In trying to make the form 1040 look simpler, the IRS added this line. It refers to a Schedule 1 and is attached to your 1040. Alimony  Under the old tax rules, alimony was deductible to the payer and taxable to the payee. No more--Congress has managed to shift the income tax burden for alimony payments to what is likely the higher earner with the higher marginal income tax rate. If you are divorcing it is important that the income tax liability of alimony payments be considered in developing an equitable settlement. Business Income/Loss  This has become a much more important item than in years past, as owners of any business that uses a pass-through entity can receive a 20% reduction to taxable income generated through that business. Assuring you maximize this important benefit is essential. See our previous post ‘Big Savings for Self-Employed and Business Owners’. Capital Gains and Losses  For all taxpayers, it is important to use tax-efficient strategies for taxable investment accounts. High yield stocks and bonds are more efficient being owned in tax advantaged accounts (401ks, IRAs, Roth IRAs etc), while investments that mostly appreciate in value are a better fit for taxable accounts. Still, capital gains rates are attractive relative to the tax rates on ordinary income.  You can use capital losses to offset any capital gains you receive, plus $3,000 of ordinary income. Capital losses are never a good thing, but at the end of each year you should review your investments to look for opportunities to offset gains. Rental Real Estate, Royalties, Partnerships, S-Corps, trusts, etc.  If you own rental properties you know how helpful depreciation can be for your income tax liability. Yes, some of the depreciation will be needed to maintain the property, but some of it will also reduce your taxable income, and if you sell, will result in more income being taxed as capital gains at currently favorable rates. If you own a property that has been fully depreciated you might consider using a tax-free exchange to like property to increase your basis and start the depreciation process all over again. Adjustments to Income Health Savings Accounts  Many American’s are now covered by high-deductible health insurance plans either through their employer or purchased directly from insurers through the Affordable Care Act Marketplace. Contributing to an HSA will reduce your current income tax liability, and if the funds are used to pay for qualified medical expenses the distributions are tax-free as well. See our post on ‘Hacking Your Health Savings Account’. Self Employed SEP, SIMPLE, and Qualified Plans  An easy way to reduce your current year income tax liability is to contribute to a retirement plan. IRA contributions are reported on line 32, but if you’re self-employed you can defer taxes on even more money. You can establish a SIMPLE retirement plan before October 31 of the current tax year and defer up to $13,000 ($16,000 if you are over age 50) annually. A SEP retirement plan allows an even bigger tax deferred contribution of up to $56,000, plus a catch-up contribution of $6,000 if you are over age 50. Another useful benefit is you have until your income tax filing deadline, plus any extension, to establish and fund a SEP for the previous tax year. If you’re a business owner who still needs to reduce your previous years taxable income-- this is your chance! Self Employed Health Insurance Deduction  If you’re self-employed, this is where you get to reduce some of your taxable income for health insurance expenses. If you’re not self-employed and are not covered by an employer health insurance plan, this is motivation for starting a side gig.

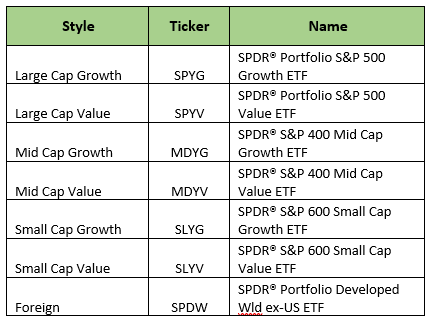

For example, the mechanic that works on cars after hours, or maybe the carpenter that does an occasional job on the side. Formalize your business to take advantage of this deduction. In Conclusion While this is far from an exhaustive list of ways to reduce your income tax liability both now and in the future, you can see there are opportunities for almost everyone to benefit from income tax planning. Take some additional time to review the tax forms you just filed or see a financial planning professional-- there is a lot at stake. Part of Oak Street Advisors’ 10 Financial Commandments for Millennials series, we discuss when to open a taxable investment account and how to strategize the location of your investment vehicles based on account taxability characteristics. Once you’ve filled up all your tax-deferred and tax-free investment accounts, it’s time to start paying Uncle Same (now) to invest. The 9th Financial Commandment for Millennials is to open a taxable investment account, while keeping tax management a key feature of this aspect of your portfolio. Investors need not worry about dividends, interest, or gains in a 401k, 403b, 457, SEP or Traditional IRAs because those will be taxed when you decide to have them taxed (or an annual portion is taxed when the government says so via Required Minimum Distributions at age 70 ½). Gains, dividends and interest in Roth IRAs are tax-free if you meet certain qualifications. For this reason, its best to have growth, dividend, and other income producing investment held inside these accounts. Now that you’re opening a taxable investment account, any growth, dividend, interest or other income is taxed in the year the gains are realized or the dividend and interest is paid (usually…i.e. phantom income). While you can use long-term capital gains tax rates to your advantage on investments held over a year, the ideal goal for a taxable account is to participate in investment growth while also not being taxed left and right for gains and income produced.  To accomplish this, we recommend using a portfolio made up of Exchange Traded Funds (ETFs). ETFs offer broad diversification that reduce the need for trading, minimize taxable distributions, and provide the long-term growth you want in a tax-efficient manner. Here’s an example of Oak Street Advisors’ FatPitch ETF Portfolio investments:  Even better-- our clients experience $0 trading cost because of our relationship with TD Ameritrade as custodian. However, any DIYer can implement a similar ETF strategy on their own for a minimal $5-$8 per trade. In general, investors can see less return drag from investment and tax expenses by utilizing this strategy in their taxable investment accounts. The relationship of the taxability of an investment and the taxability of the account it is held matters, and can keep dollars in your pocket. As with any investment, making sure you’re sticking to your strategy via rebalancing and reacting to market conditions, or paying someone to do so on your behalf, is crucial.  Part of Oak Street Advisors’ 10 Financial Commandments for Millennials series, we go through the advantages of paying down common and often necessary consumer debts such as car loans, mortgages, and student loan obligations. If you’ve made it to the 8th Commandment congrats, you have established a strong financial foundation; we also know you’ve paid off your high interest credit card debt—but now it’s time to start pecking away at the larger consumer debts weighing down your net worth. I’m referring to debt typically considered “necessary” for most Americans—student loans, your mortgage, car loans, business loans etc. These are loans with normally reasonable interest rates and longer payoff schedules. Paying them down may seem almost unattainable but be assured, if you commit to doing so you will save a lot of money. For example: adding $100/month to a $500,000 mortgage at 4.5% interest will save $36,240 over 30 years. That seems abstract, like you will never really see that savings—but your net worth doesn’t lie.  What Should You Start Paying Down First? We discuss the two different debt payoff methods in Getting Out of Credit Card Debt: The 2nd Financial Commandment for Millennials. Our advisors tend to favor the Snowball Method, so we’d recommend starting with the smallest loan first. The thinking is as follows; Paying off a car note early not only saves interest but also increases monthly cash flow by eliminating the monthly car payment. The money that would have been allocated to the car payment can now be used to pay down student loans or add monthly principle additions to the mortgage. Paying down your mortgage or student loans is not sexy financial planning advice—but doesn’t saving tens of thousands of dollars and eliminating all debt down sounds pretty awesome?  |

Archives

September 2023

Categories

All

|

RSS Feed

RSS Feed