Whether you’re trying to buy a home, looking to refinance or hoping to get a lower interest rate on an automobile loan - your credit score matters. Clients often ask me how they can improve their scores and the answer is the same regardless of which stage of life you’re in.

1) Increase Your Limits This is pretty easy to do, yet most clients don’t realize it. Here’s how it’s done: Call up your credit card company (all of them) and simply ask them to increase your limits. Some will simply increase it without any hesitation, but often this method produces only a minimal increase. When they say they’ll increase your limit by $2,000, tell them you want it upped by a significantly greater amount. What’s that amount? I recommend something unlikely to be granted- say 10-20 times your current limit. The point here is that they’ll type in your request, which will likely to be denied, and then give you the maximum increase allowed by their computation. Why? This will improve your credit to debt ratio. The basic tenet here is that your credit score is positively impacted when you increase your credit to debt ratio. Here’s an example: You have a $15,000 limit on your credit card. You carry a $3,000 revolving balance on said credit card. Your credit to debt ratio is: $3,000 ÷ $15,000 = 0.20 or a 20% ratio. By adding all your limits and debts and using the above equation, you can determine your ratio. So, even with not paying your debt down, increasing your credit limits by making a few phone calls will improve your score and cost you nothing. Even if you pay off all your cards every month, your score will increase still if you increase your credit limits. Having the ability to borrow more but not doing so helps your score. 2) Don’t Close Old Credit Card Accounts If a card is paid off and you don’t use it anymore, just shred it but do not close the account. Again, you want to keep your credit to debt ratio low. Having that credit line but keeping a $0 balance only helps. Further, the longer you have had a credit card open, the better for your score. 3) Pay Off All Cards Each Month or as Much as Possible Duh, right? Everyone understands this, but I put this point here to again discuss your credit to debt ratio. Larger credit limits combined with less debt equals a better ratio- simple! 4) Spread Your Credit Card Debt Out If you already have several cards, I don’t recommend opening another account, but you don’t want to over utilize any of your cards. You should use no more than 30% of a card’s credit limit and of course, the less the better. 5) Don’t Open a Bunch of Cards While you want to work on decreasing your credit to debt ratio, this will actually hurt your score. 6) Pay Your Bills on Time Everyone knows this, but if you have missed a payment make sure you get current on those bills. Use these strategies and your score will go up. I’ve seen it happen both for myself and clients. If you’d like to know more about other strategies that can help you establish a strong financial foundation, check out our Financial Fitness program. FinFit is built to help our clients do just that!  As a financial planner, when a potential client comes to me with money to invest they often ask, “How should I start investing my money?” They know that they need to invest and have extra capital on hand to do so, but they’re putting the cart before the horse. Before even speaking with them about their risk tolerance, current investments, potential strategies for future investing etc. I always ask, “How much is in your emergency fund?” The answers can range from “What’s an emergency fund?” to having hundreds of thousands in a savings account. But more times than not, they don’t know exactly how much they should have in savings. An emergency fund is a savings account dedicated to bailing you out when unforeseen financial troubles arise. This fund is for repairing your HVAC unit, fixing your car, unexpected medical bills, and especially loss of wages. The emergency fund shouldn’t be so small that you aren’t able to cover a financial crisis without going into debt; but not so large that you have too much capital allocated in cash. General guidelines for an emergency fund say it should be around 3 months of expenses for two incomes, 6 months of expenses with one income- for both single and married investors. This is a baseline, but your Emergency Fund should be dictated by your individual circumstances. You and your financial planner should collaborate to determine the amount that is right for you. Once the proper amount is determined, your emergency fund should be moved into a high yield savings account. Most of us keep our savings at a big bank and receive terrible interest rates for parking our money there. While it may not seem like a lot of extra money, going from an account producing 0.01% interest vs. 1.0% interest just makes sense. Why not let your money earn the most it can for you? For example, say you have $10,000 in your Emergency Fund: Interest Rate Amount You Earn/Year Bank A 0.01% $10 Bank B 1.0% $100 I know, this is not a huge difference, right? But over 10 years, you have received $900 more by utilizing Bank B. While you will have to pay more in taxes with Bank B, you will still come out well ahead. I encourage you to look at the current return on your savings account, then go here to compare it to other options available. You may be pleasantly surprised what this simple move can do to increase your earnings on the money you have already saved.  Roth IRA accounts have been available since 1997. In a traditional IRA, you contribute pretax dollars that grow tax deferred, but are taxable upon withdrawal. Roth IRAs are for after tax contributions that provide tax free growth and distributions upon retirement.

The magic of compounding means, the earlier you start, the greater the tax-free growth within the account. If you are 20 when you start making contributions, you could be looking at four doubles of your original contribution by the time you retire at age 60. That means a $6,000 contribution this year could grow to $96,000 allowing you to potentially create a constant flow of tax free income for your retirement years. Another reason to open a Roth IRA is the flexibility it can provide to fund emergencies that may arise over your lifetime. The Five-Year Rule You can always withdraw any Roth IRA contributions without taxes, after all, you paid income tax on the money prior to making the contribution. However, if you haven’t had the Roth IRA open for at least five years, your distribution could still be subject to a 10% tax penalty, similar to the early withdrawal penalty for traditional IRAs. The five years for withdrawals begins when you open the account, not when you make subsequent contributions. There is also a five-year rule for Roth IRA conversions that start in January of the year you make a conversion. This additional rule was enacted to prevent someone from using a Roth IRA conversion to avoid early distribution penalties from traditional IRA withdrawals. Who qualifies for a Roth IRA If you have a modified adjusted gross income of less than $124,000 and are single or less than $196,000 if married filing jointly, you can make Roth IRA contributions of 100% of your income up to $6,000 if younger than age 50 or $7,000 if age 50 or older. Back-door Roth IRAs Because there are no income limitations for converting traditional IRAs to a Roth IRA, many who are disqualified for income resort to the back-door method for funding a Roth IRA. This works because anyone may open and contribute to a non-deductible traditional IRA, even if you are covered by a qualified retirement plan. Once the funds are deposited into the nondeductible traditional IRA, they can then be converted to a Roth IRA. This has the same net income tax effect as contributing directly to a Roth IRA. The Early Bird Gets the Worm Tax free growth and tax free distributions are very enticing especially for those with many years until retirement, so start today. The more time your account has to grow tax free, the better.  I often get the question of what to do with an old 401(k) or 403(b) sitting with a former employer. In short, there are only a few circumstances where you would want to leave it be, but in those circumstances it can be extremely advantageous to do so.

So, when should you leave the money in an old 401(k) or 403(b) rather than roll it over to an IRA?

Other than these scenarios, I recommend rolling over your nest egg to an IRA with a reputable fiduciary. Just some of the reasons are:

This is one of the walls in the reception area of my office. You can see I like to hang lots of little items there. The items were picked with some care, they are meant to convey to clients and prospective clients a sense of who I am and what I believe in. They are also there to remind me of what I aspire to. If you came to my office you would find that none of the items on the wall relate directly to money or wealth in the traditional way you might expect at an investment advisor’s office (though there are other places where you could find some of that).

The items on the wall are there to remind me that money is just something that allows us to live fuller lives. It is not a goal in and of itself. One of the plaques reads “Enjoy the little things in life because one day you will look back and realize they were the big things”. That is a reminder that everyday I have the chance to enjoy something. It may not be a big new shiny thing, but that is not important, what is important is for me to be mindful and grateful for all that comes my way. One of the cards reads “You are what you eat…I need to eat a skinny person” That is there to remind me to have a sense of humor and to laugh once in a while. Life is meant to be fun. Another reads “Success is getting what you want, happiness is wanting what you get” That’s a reminder that I am as wealthy as I allow myself to be, by being happy with what I have. Maybe you have a wall of your own. Maybe it exists only in your head. What do you hang on your wall?  It is important to understand all the risk you face as an investor. Risk comes in many forms and some risks are higher than others at different stages of market cycles. Understanding the risks that could hurt you the most and how you can offset or reduce that risk is important to your long term success as an investor.

There is company specific risk. That is the risk that you will own a company like Enron or MCI or Kodak or any other of a myriad of companies that have fallen by the wayside. The cure for market risk is broad diversification. If your portfolio had a 1% exposure to Enron when they imploded it didn’t really hurt, the other 99% of your portfolio likely bailed you out. But if Enron was 20% or more of your portfolio it hurt a lot and took a long time to recover from. There is interest rate risk. That is the risk that interest rates will rise. This is generally bad for dividend paying stocks, but is really, really bad for bonds, as bond prices fall when interest rates increase. I would venture that interest rate risk is higher in most portfolios today than at any time in the last 25 years. There is inflation risk. The risk that the falling value of a currency will lead to lower purchasing power per unit of currency. Inflation is really bad for bond holder as they are repaid with currency that purchases less goods and services than the currency they originally loaned out. You can offset inflation risk to a degree by investing in inflation protected bonds or by investing in companies that pay dividends that go up over time. There is political risk. That is risk that an act of the government could adversely affect an industry. Energy policy can mean millions of dollars of extra business for oil companies or millions of dollars of extra business for renewable energy firms. Tax policy can benefit some industries more than others. Political risk is hard to avoid because it changes so often and is so capricious in its implementation. Here, diversification is once again your friend. Finally, there is obviously, market risk. Which is will the market prices of the securities you own go down in value over some arbitrary time frame. I say some arbitrary period of time because over the long run this risk has always disappeared. Over the last decade, we have seen markets go down by 50% or so, only to see them rebound by more than double that number. In your lifetime, you will likely see over two dozen times when stocks will retreat by at least 15%. Yet over your lifetime the stock market will almost certainly be a one-way street with the bias to the upside. Maybe we should call this the risk of missing out rather than market risk, because the fear of short term dips could prevent you from profiting from the permanent ups of stock ownership. Understanding the risks you face and the ways you can offset that risk will help you become a better investor. Invest some time to contemplate the risks you are facing today.  It’s that time again. The time when we make resolutions for the New Year. Resolutions are things we want to change. I resolve to…

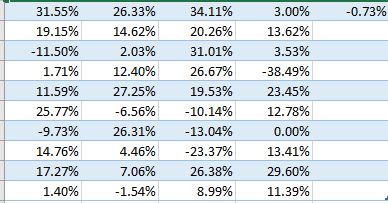

Resolutions are your goals for the coming year. Write them down on paper – in ink. Committing goals to paper makes them more concrete than goals we merely hold in our head. And don’t stop with just writing them down, stuff that piece of paper in your wallet or purse. Tape it to the visor in your car. Put them somewhere so you will see them on a regular basis. When you see your goals think of one thing you can do that day that will bring you closer to reaching that goal, and do it. Do something, do anything…everyday.  Over the last 80 years the stock market has advanced an average of 10% each year, but average is not normal when it comes to the stock market. The table pictured on the left shows the actual returns for the S&P 500 each year since 1975. How many of those returns were 10%? How many fell between 9% an 11%? Not many were even close to average.  So while you may be hoping for your investments to look like this.  You will likely experience something like this.

Bob Clark, a columnist for Investment Advisor magazine, recently said, "...the role of advisors is to protect their clients from the financial services industry". Many times the products pushed by the large financial service firms do more harm to investors than good. The "hot" product du jour is currently the Equity Index Annuity.

While the equity index Annuity itself is not an evil thing, the way they are presented to investors is many times misleading, and they are often pushed to be a much larger part of a portfolio than prudence would justify. In brief, an equity index annuity, provides returns that a related to some stock market index. As such they can be viewed as an equity derivative (remember those?). Investors typically receive a return that is some portion of the return of an index like the S&P 500 (for example 90% of the point to point return of the price increase of the index, not including dividends), the average monthly return of the index over a predetermined period (again not including dividends), or the monthly gain of the index with a predetermined cap (often 2-3% per month cap). The big draw is that you receive a guarantee that your account will not have a negative return over some period of time. Often touted as "heads you win, tails you don't loose". On the face that sounds enticing. It is only if you kick the tires that problems become apparent. First, like most annuities there is a long period of time where you a charged a surrender charge if you want or need to withdraw more funds than allowed in the contract (I have even seen instances where the surrender charge is applied to any withdrawal except in the case of annuitization). Second, any gain from annuities is considered to be distributed first, and taxed as ordinary income (you do not get favorable dividend of capital gain rate when you file your taxes), and any distribution before age 59 1/2 could be subject to a 10% premature distribution tax penalty. Worst of all the returns investors receive will likely not measure up to expectations. The pitfalls of monthly caps and averaging returns requires some contemplation to understand. Let's say you are credited with any market gains up to 2% each month. That means if the index you participate in goes up by 2% you are credited with the full 2%, if the index goes up 3%, sorry, you are still only credited with 2%. Okay, you say, that's not so bad, I can still earn a whopping 24% in a year! In theory yes, in practice, no. See sometimes, even in a very good year, markets will fall back some months. And you equity indexed annuity lets you participate fully in the monthly market drops, as long as the account moves no further than 0% in a year. If the index you participate in rises by 3% one month, the 1% the next month, but falls by 3% the following month, your account earns zero, nada, zilch. You were credited with 2% the first month, then 1% the second month, but got dinged for the full minus 3% in the third month. It's all very confusing, and people hear what they want to hear. That is what the insurance companies and agents who sell equity index annuities are counting on. Heads the insurance company wins, tails, you lose.  Individuals with special needs and families that seek to help, have long been hamstrung by the Catch 22 of public assistance. If a family provides too much financial assistance, the beneficiary loses access to government assistance. If the family does not help the individual may suffer from lack of access to housing and education. For special needs individuals to receive an inheritance they needed a special needs trust or the inheritance was quickly depleted until the special needs individual once again attained poverty level to qualify for public assistance.

In 2014 congress passed the ABLE act to allow special needs beneficiaries’ families to establish a savings vehicle funded with up to $14,000 per year (adjusted for inflation) to supplement public assistance. The account may be used to pay for needs such as housing, education, transportation, and other expenses that improve the quality of life for those with disabilities. Similar to 529 college saving plans, ABLE accounts are established by the states, but you can participate in the plan of a state other than your home state if you choose. The account may not hold more than $100,000 of assets without running afoul of the Supplemental Security Income rules, but still this is an improvement over the expense and complexity of using a special needs trust. For many families this account will prove invaluable. To qualify for an account, the individual must have significant disabilities and the age at onset of the disability must be prior to attaining age 26. At the death the state where the beneficiary resides may be able to claim any balance remaining in the account under the Medicare payback rules. Currently ABLE plans have been established by Florida, Nebraska, Ohio, and Tennessee. If you are not a resident of one of these states non-residents are allowed to establish accounts in Nebraska, Ohio, and Tennessee. For more information, you can visit the ABLE National Resource Center online. |

Archives

September 2023

Categories

All

|

RSS Feed

RSS Feed