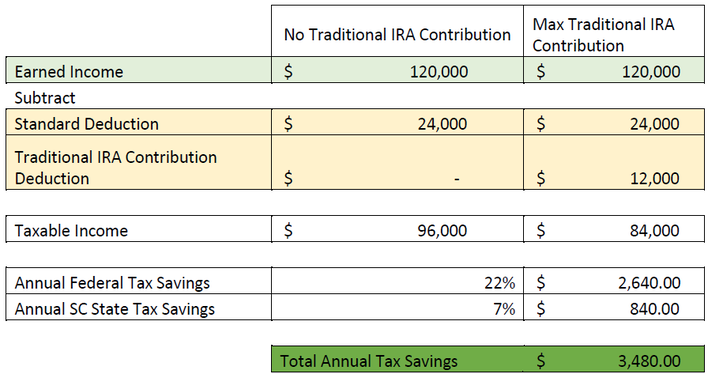

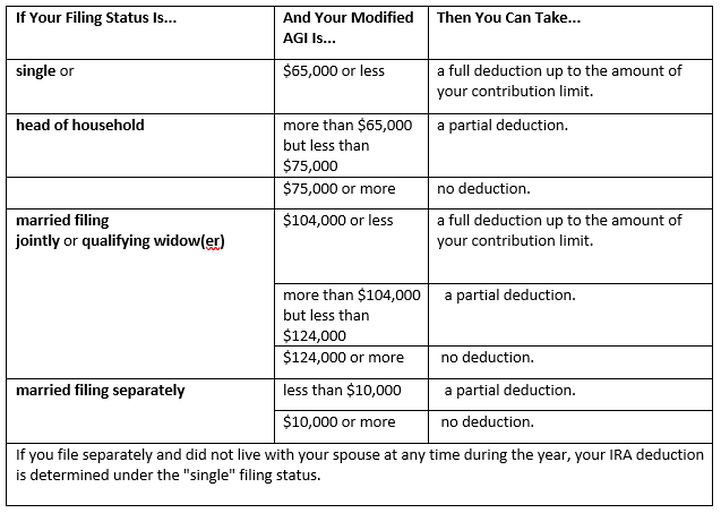

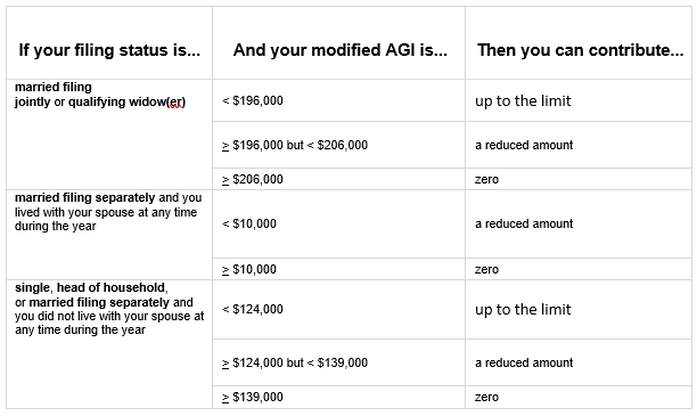

How High Earners Can Diversify the Taxability of Their Retirement AssetsOur fee only financial advisors often recommend executing a backdoor Roth IRA contribution strategy for high earning clients who max out their tax-deferred and/or after-tax employer sponsored plans and are seeking additional tax favorable approaches to save and grow assets. These clients often accumulate large levels of tax-deferred dollars in their 401k, 403b, or other employer sponsored plan(s). These tax-deferred contributions help save tax dollars in high brackets now and withdrawals in retirement can be structured for tax savings in the future as well. On the other end, if we can add in Roth IRA assets to our clients’ portfolios which can be withdrawn in retirement tax-free, we add another tool in the tax-planning belt. What are Backdoor Roth IRA Contributions For most wage earners, if you contribute to a Traditional IRA you receive a dollar-for-dollar tax deduction. Here’s an overly simplified look at the tax reduction provided by the combined maximum family deductible Traditional IRA contributions of $12,000 for a married couple in 2020:  Unfortunately, if you earn over a certain level of income and/or have access to an employer sponsored retirement plan (401k, 403b, 457b, etc., whether you use it or not) you lose the deductibility of your Traditional IRA contributions.  **IMPORTANT: Even if you can’t deduct IRA contributions, you can still make them.** New clients are often surprised when we tell them they’ve been missing out on these tax favorable IRA contributions. Many investors assume they can’t make IRA contributions because they make too much money or already participate and max out an employer 401k or 403b plan. In each case, you can make IRA contributions, you just can’t deduct them. Unlike Traditional IRAs, when you make contributions to a Roth IRA you pay the taxes now-- or have already paid taxes on the contributions via payroll and will simply not receive a tax deduction for the contribution. The magic of a Roth IRA is that once the assets are in the account and the account has been open for 5 years—all withdrawals of principal AND earnings are tax-free. And tax-free > tax-deferred. But high earners are not allowed to make direct Roth IRA contributions, because Roth IRAs have their own income level eligibility qualifications:  So-- if you’re single making more than $139,000 AGI or married and earn over $206,000 AGI you can’t make direct Roth IRA contributions AND you don’t get Traditional IRA contributions deducted. However, if you have little or no Traditional IRA assets to start with, we recommend executing a backdoor Roth contribution strategy. High earners can make non tax-deductible contributions to their Traditional IRAs, receiving no tax deduction for the contributions. Then they can immediately convert that contribution to their tax-free Roth IRA. Why would you want your investments growing tax-deferred when they could be growing tax-free? Not simple to do, but a no brainer…slam dunk. How are Backdoor Roth IRA Contributions Taxed? A key factor that must not be overlooked is the amount of previously tax-deferred Traditional IRA assets a high earner has while executing this strategy. It’s important because Roth conversions are taxed at the ratio of tax-deferred assets to after-tax, or non tax-deferred assets. For example, let’s say you’re a married high earner and want to start this backdoor Roth IRA strategy. You make the max Traditional IRA contributions of $12,000 ($6,000 each) for you and your spouse for 2020 and plan to immediately convert that to your Roth IRA to facilitate the lifetime tax-free growth mentioned above. At the same time, you already had $12,000 (again $6,000 each) of tax-deferred contributions from previous years where you qualified for the deduction. Or you could have rolled over tax-deferred assets from an old 401k into your Traditional IRA. Either way, half the assets in the Traditional IRAs were tax-deferred in prior years, and half are non-deductible from 2020’s contribution. If you convert the $12,000 of non-deferred contributions you made in 2020, it wouldn’t be a tax-free conversion— it would be taxed according to the Roth IRA pro-rata rule. This states you have to use the tax-deferred to non-tax-deferred ratio for taxing of the conversion assets. In this case the ratio is 50:50 ($12k tax-deferred to $12k tax-free), so half, or $6,000 of the $12,000 Roth IRA conversion would be taxed at your normal income tax rates for 2020. This is important-- because if you’re a high earner, you may want to avoid paying 32%+ Federal taxes this year on that $6,000 taxable portion of the Roth IRA conversion. It may be better to wait until retirement when you’ll likely be in a lower tax bracket, especially if you do some of the tax planning we mention in this article. The Roth IRA pro-rata rule should give pause to rolling over tax-deferred dollars from 401ks or 403bs into a Traditional/Rollover IRA when a backdoor Roth IRA strategy is recommended. The more assets added to your personal Traditional/Rollover IRA, the higher the taxable percentage of Roth IRA conversions. For these reasons, our financial advisors may recommend clients keep tax-deferred dollars in an old employer plan-- even if those plans have slightly elevated fees or lack diversified, cost-efficient investment offerings. We believe the tax-free savings of Roth IRA assets for a young high earner provide unmatched advantages in terms of investment returns and future tax planning strategies. Getting assets in a high earner’s Roth IRA early while avoiding unnecessary taxes at their currently high tax brackets provides great value to our clients. On the other hand, some clients prefer to fill up their brackets with Roth conversions to eventually get rid of all Traditional IRA tax-deferred assets, never having to worry about Roth conversion taxes again. Regardless—your taxable income level and tax bracket management must be thoroughly analyzed to make the right decision. Why Should I Build Roth IRA Assets?Saving on Pre-Medicare Health Insurance Premiums For example, let’s say a couple retires at age 60, with 5 years before Medicare eligibility. Our fee only advisors use taxable investment accounts and tax-free Roth IRA assets to strategically qualify millionaires for Premium Tax Credits under the Affordable Care Act that can offset some of the cost of healthcare insurance. Monthly private marketplace insurance premiums at age 60 are likely to be $1,000 per person—meaning if you and your spouse plan to retire at age 60, every year until age 65 you’ll fork over $24,000 alone on healthcare insurance premiums before you step foot in a doctor’s office. That can put a damper on early retirement plans. Our fiduciary advisors can situationally use taxable and Roth IRA assets to qualify even our most wealthy clients for Premium Tax Credits, which cover a portion or all of a family’s health insurance expenses. In the above example, that’s a potential savings of up to $120,000 in premiums from retirement at age 60 to Medicare eligibility at age 65—and a glaring reason everyone should invest in a financial plan. *Added Note: Recently, we’ve heard several current and prospective clients mention they’re going to beat high healthcare insurance costs during pre-Medicare retirement years with some sort of too-good-to-be-true Medi-Share plan. Please reconsider. These plans are not actually health insurance and leave your family’s wealth and health in jeopardy. One un-insured serious hospitalization could put your entire financial future needlessly at risk. Long Term Capital Gains Rates Saving  We also use taxable and tax-free assets to manage tax brackets via favorable capital gains rates, and in some cases, help our clients pay 0% on capital gains through complex tax planning strategies. For those high earners today, as tax laws are, as is, we’d be able to structure their taxable income so they can optimize favorable capital gains rates while ensuring their assets at 12% Federally. That’s a Federal tax savings of $22,000+ for every $100,000 in their IRA. Not a bad deal for someone being taxed at 24% or 34%+ today and may even pay the 3.8% Medicare investment income surcharge. Other Uses for Roth IRA Assets Tax-free income can help manage tax brackets/income in retirement and can lead to enormous tax savings if planned correctly. If you max out your employer retirement plans and are looking for even more tax diversification of your assets, a backdoor Roth IRA strategy is a good choice. There are many factors to analyze to ensure you realize the tax savings these strategies provide.

If you could use help determining the most appropriate course of action to take with your excess savings give us a call and get started with a financial plan today. Comments are closed.

|

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed