Not sure how to choose a financial advisor? It’s a big decision! Our guide on how to find a good CERTIFIED FINANCIAL PLANNER™ practitioner can help you ask the right questions and select someone able to help you reach your personal financial goals and find financial freedom. Do You Need a Financial Advisor?Depending upon where you are in your life, you may not have spent much time thinking about your financial future. NOW is always the best time to start! Finding a financial planner can help you focus on personal financial goals, like buying a new home, saving for a child’s college education, or retiring at a certain age. And if you have recently received a significant pay raise, come into an inheritance or trust, or need help with tax planning, a financial advisor can help you leverage and maximize those assets. Do You Need a New Financial Advisor?Have you started to wonder if your current financial advisor is right for you? Most financial advisors receive a significant portion of their pay in commissions. When they recommend that you purchase shares of stock or mutual funds from a broker, they receive a portion of the proceeds of that sale in return. They can also make money through mark-ups of bonds, CDs, or new stock issues through a broker. And because advisors paid in by commission make the most money when you purchase financial products, they may be tempted to recommend buying things you do not really need. And their interest in your financial wellbeing may not extend beyond that sale. Many financial advisors do not assist with 529 savings plans, employer benefits packages, healthcare options, or estate planning, all critical components of a good financial plan. If you have started to wonder if your current financial advisor is truly looking out for your best interests, it is time to look for a fee-only financial advisor. What is Fee-Only Financial Advising?Fee-only is a better way to get smart financial advice you can trust. Fee-only financial advisors never make money from commissions or mark-ups. We are only paid by you to give advice that we believe will work best for you. You will never need to second-guess our motives, suggestions, or strategies. You will always know that your financial future is our highest priority. Fee-only financial advisors must meet a very strict professional fiduciary standard. Fee-only financial advisors must become Registered Investment Advisors and meet the highest fiduciary standard, while other financial advisors are held to a lower suitability standard. To be sure you are working with the best and that your financial advisor has only your best interests at heart, choose a fee-only Certified Financial Planner™ Practitioner (CFP®). Research a Financial AdvisorWord of mouth can be a great way to find a financial advisor. Asking your friends, relatives, and coworkers if they have a financial advisor they trust and would recommend can be a great place to start. Online research can also help you find and look into your options. Whenever you are given or find a name, take a moment to look them up on the broker check tools maintained by the Security and Exchange Commission or FINRA. And don’t stop with the broker name! Make sure you also plug in their firm’s name. If the firm has multiple infractions that may be an indication of poor corporate culture. What to Know Before Meeting with a Financial Advisor

Questions to Ask Your Financial Advisor

Selecting a Financial AdvisorFinding a financial planner lets you start the exciting and rewarding process of creating a financial plan calibrated just for you and your personal financial goals. Abstract ideas become an action plan. You have specific instructions and ways to mark your progress. You know how to ask for help and when to ask for changes or adjustments. And you can finally see the big picture—not only where you are today, but where you want to go.

WHAT’S A DONOR ADVISED FUND?A donor advised fund (DAF) is a relatively new tool that helps both taxpayers and charities reduce taxes now while providing planned donation strategies to continue in the future. Much like a deductible IRA, assets contributed to these donor accounts produce tax savings based on specific IRS guidelines. For taxpayers who itemize deductions every dollar donated to a donor advised fund reduces the donor’s taxable income dollar-for-dollar in the year of the gift. For high earners this is one of the few strategies to reduce taxable income outside employer retirement plans and benefit packages. Once in the account, the gifted assets grow tax-free until the donor decides to distribute the funds to the qualified charities they desire. There’s great advantage in the flexibility a donor advised fund offers. Donors make contributions now to reduce taxes now, those donations then grow via investments tax-free and those appreciated assets are then distributed at some time in the future to a qualified charity. This is a good deal for everyone involved, except Uncle Sam. For those in the highest tax bracket, every $1,000 donated to your donor advised fund results in a Federal and SC state tax savings of ~$440. Donating $100,000 would save that same taxpayer $44,000 in Federal & state income taxes; you can also use a DAF to avoid taxation on appreciated assets with low cost basis altogether. GIFTING APPRECIATED STOCK TO YOUR DONOR ADVISED FUNDTo really compound the tax savings inherent with a DAF, we recommend donating appreciated stock positions from your taxable accounts. You avoid capital gains taxes, get full value of the gifted equities in the form of the tax deduction and the assets grow tax-free until distributed to a qualified charity. Be sure you only contribute shares that you have held for at least twelve months. For any shares held less than twelve months you can only deduct your cost basis. BUNDLING CHARITABLE DONATIONS TO OFFSET INCOME WINDFALLSSome taxpayers may consider bundling annual contributions to their Donor Advised Fund into a single year to avoid wasted donation dollars that the newer and higher standard deductions produce.

For example, if you plan to give $50,000 a year for the next 10 years, and you know you have a big real estate sale, sales or performance based bonus, or generally know your taxable income will be irregularly elevated in a single tax year, you may want to bundle those annual amounts into a single, large donation that year. In this scenario, you’d donate $500,000 immediately but only distribute $50,000 each year out of the DAF while the remaining principle donations continue to grow tax-free via your investments; This strategy allows a taxpayer to continue their plan of gifting $50,000 annually while realizing a tax savings of ~$220,000 in the year of the windfall. Why you might not want to rollover that old 401k

*The rollover strategies discussed also apply to 403b, 457b, 401a and other employer sponsored qualified retirement plans For many high wage earners, making contributions up to annual Roth IRA limits (6k/$7k over 50; 2020) via the backdoor Roth IRA strategy is an appealing way to generate income tax free growth and income for future years. The backdoor Roth strategy entails making a non-deductible IRA contribution and immediately converting that contribution to a Roth IRA account. If you have no other rollover tax deferred IRA accounts when you execute this strategy, then you have simply moved money from a taxable account into a tax-free account. What If I have existing Rollover IRA and/or Traditional IRA Assets?When executing the backdoor Roth strategy, if you have any tax-deferred Rollover or Traditional IRA Assets, i.e. you haven’t paid income taxes on them yet, the Roth conversion will result in at least some of those funds being taxed in the year of the conversion. For example, let’s say you have a Traditional IRA or Rollover IRA worth $60,000 and make a non-deductible contribution of $6,000 to this IRA in accordance with your backdoor Roth IRA strategy. When you convert the same $6,000 from your Traditional or Rollover IRA to Roth IRA assets, you’ll actually be taxed on ~91% of the conversion, which creates extra taxable income of $5,460 for the tax year. This overlooked tax trap results from IRS rules which mandate, for tax calculations, your tax-deferred contributions and gains and non-deductible contributions from all IRA accounts (Rollover, Traditional & Roth) are combined into a theoretical IRA pot. From this theoretical pot, the IRS requires you to calculate the ratio of tax-deferred dollars to non-deductible dollars; the percentage of tax-deferred dollars in your theoretical account is the percentage of your Roth IRA conversion that will be taxed. In this example your non-deductible $6,000 contribution to your Traditional IRA or Rollover IRA is divided by the total account value of $66,000—just roughly 9% is not subject to income taxes at the time of conversion. The aggregation rules are one of the few reasons you should carefully think about not rolling over an old 401k or other employer plan. If the funds remain in a 401k, 401a, 403b, 457b etc. they are not subject to the aggregation rules. While there’s no avoiding taxation of previously deducted personal Traditional IRA contribution assets during a backdoor Roth IRA strategy execution or other Roth conversion, there are sometimes opportunities to clean up existing Rollover IRA accounts to avoid this unpleasant tax consequence. The Difference Between a Rollover IRA and a Traditional IRAThough they’re nearly identical, there is a subtle, but significant, difference. You can roll over a 401k to a Traditional IRA or Rollover IRA. If you choose to roll funds into a Rollover IRA, rather than a Traditional IRA, you maintain the ability to roll those funds into another current or future 401k plan, if the plan documents allow. Why Does That Matter?There are 401k plans that allow IRA roll-in contributions, but they must come from a Rollover IRA, not a Traditional IRA. If your company has such a plan, you can roll your existing Rollover IRA account into your 401k plan which eliminates the tax-deferred IRA portion of your aggregate portfolio, allowing a high earner to execute the backdoor strategy completely tax-free. Without this keen planning taxes would be paid at high income brackets on the conversion, which is counterproductive to high earner’s overall tax strategy. Don’t Commingle Rollover IRA and Traditional IRA AssetsIf you commingle “regular” Traditional IRA funds and Rollover IRA funds you lose the ability to roll-in former Rollover IRA assets. It’s important to keep the Rollover IRA and Traditional IRA accounts separate. Consider opening a stand-alone Traditional IRA for annual personal IRA contributions and a separate Rollover IRA for rollover assets.

As always, things are rarely as simple as they seem. You should work with a competent Financial Planner to determine the best advice on your personal tax planning strategy. Questions about tax minimization strategies regarding your 401k rollover or rollover IRA? Click here to setup a no cost discussion with us today!  As financial planners, we meet with many parents concerned about how they will pay for their child’s college education. These parents often ask about the Future Scholar program, the 529 college savings plan for residents of South Carolina. We created our educational savings guide below to explain how a 529 program works, the benefits of a 529 plan and the disadvantages of a 529 plan, and help you determine whether or not the SC Future Scholar Program is right for your family. What is the South Carolina Future Scholar program?Paying for college can feel like a monumental task for any family, no matter how financially comfortable they may be. Although tuition inflation in higher education has slowed in recent years, the price of a four-year college degree is still very high. State governments have developed a special type of savings plan designed to help families save for this significant financial expense: the 529 college savings plan. In South Carolina, the plan is called the Future Scholar program, and it includes tax benefits designed to ease the burden of college tuition and encourage regular contributions. How does a 529 Plan work Any U.S. citizen can open a 529 savings account for a child regardless of their income level or their relationship to that child. There can even be multiple accounts for the same child as long as all combined contributions across these accounts do not exceed $520,000 in South Carolina. The maximum aggregate contribution limits vary by state. Most 529 plans allow participants to deduct part or all of their contributions on their income taxes and contributions to the SC Future Scholar Program are tax-deductible on the state level. And like any savings account, the money in a 529 account grows over time through additional contributions and interest earned. Unlike other savings accounts, however, the interest earned and the withdrawals you make are also tax-free. Money can be withdrawn from a 529 college savings plan for tuition and fees, room and board, books, computers and other supplies required to attend any eligible institution offering post-high school education: two and four-year colleges, graduate and professional programs, and even certain vocation/technical schools. Benefits of a 529 Plan

Disadvantages of a 529 Plan

How Do I Open an SC Future Scholar Program 529 Plan?The SC Future Scholar Program is managed by a group called Columbia/Threadneedle, created by the merger of Columbia Management Investment Distributors of the US and Threadneedle Investments of the UK. Columbia Management is owned by Ameriprise, a national broker/dealer and financial service firm. There are two ways to invest in the Future Scholar program. If you are a South Carolina resident, you can open and fund your accounts online directly with Columbia/Threadneedle or you can invest through the broker or your choice. See the sections on fees and expenses to understand the differences between these two approaches.

What is the Current Ranking for the SC Future Scholar Program 529 Plan?Each year, Morningstar publishes a ranking of all 529 college savings plans across the country, awarding them gold, silver, or bronze status—or below. The SC Future Scholar plan landed solidly in the middle of the pack this year with a Neutral rank for the direct option. If I Want a Gold 529 Plan, What are My Options?The younger your beneficiary, the greater the value of lower fees and better fund selections. South Carolina residents can get the biggest bang for their buck by opening and contributing to the SC Future Scholar Program to capture state income tax savings. As their child approaches college age, they can execute a custodian-to-custodian transfer to a better 529 plan, such as the gold rated Utah Educational Savings Plan. Because a custodian-to-custodian transfer is not taxable, you can have your cake and eat it, too. How Do I Get the Most Out of My SC Future Scholar Program Plan?

How Do I Calibrate My Investment in a SC Future Scholar Program Plan to Maximize My Investment or Manage My Risk?Because you can only change the investments in a 529 plan twice each calendar year, many investors choose to select an age-based or a risk-based portfolio that is rebalanced by the plan administrator. The SC Future Scholars Program plan offers the following asset allocation portfolios:

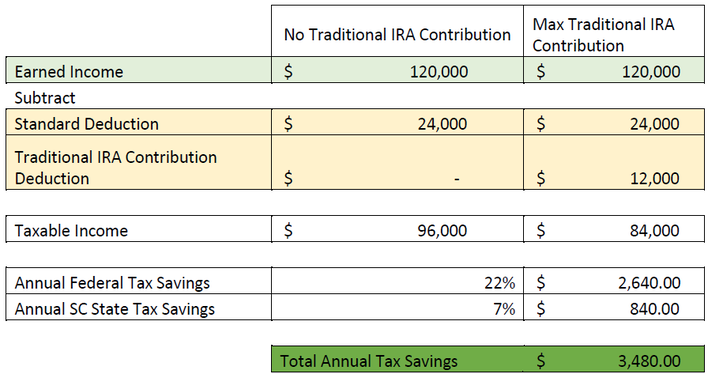

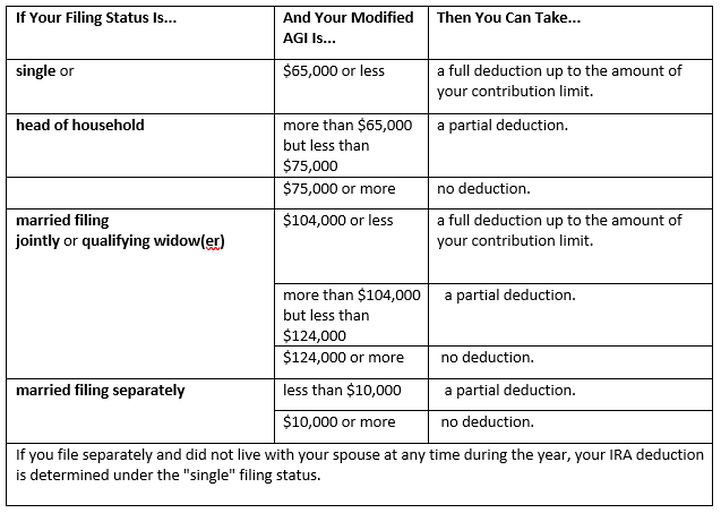

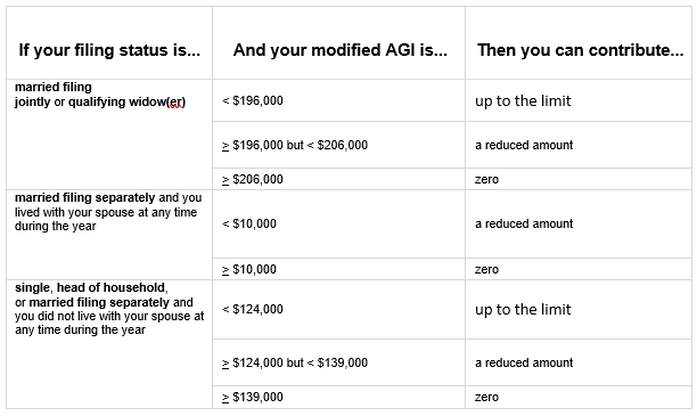

The age-based portfolios are divided into Aggressive, Moderate, and Conservative tracks. Different asset allocation portfolios can be used at different ages to create a glide path toward your child’s college entrance date. If you purchase share through a broker, there are some small differences in the allocation portfolios because they offer some actively managed fund choices not available to direct buyers. Ready to take advantage of significant state income tax savings while creating future educational opportunities for a child? Talk to Oak Street Financial Advisors about the best way to set up and calibrate your SC Future Scholars Program 529 Plan today. How High Earners Can Diversify the Taxability of Their Retirement AssetsOur fee only financial advisors often recommend executing a backdoor Roth IRA contribution strategy for high earning clients who max out their tax-deferred and/or after-tax employer sponsored plans and are seeking additional tax favorable approaches to save and grow assets. These clients often accumulate large levels of tax-deferred dollars in their 401k, 403b, or other employer sponsored plan(s). These tax-deferred contributions help save tax dollars in high brackets now and withdrawals in retirement can be structured for tax savings in the future as well. On the other end, if we can add in Roth IRA assets to our clients’ portfolios which can be withdrawn in retirement tax-free, we add another tool in the tax-planning belt. What are Backdoor Roth IRA Contributions For most wage earners, if you contribute to a Traditional IRA you receive a dollar-for-dollar tax deduction. Here’s an overly simplified look at the tax reduction provided by the combined maximum family deductible Traditional IRA contributions of $12,000 for a married couple in 2020:  Unfortunately, if you earn over a certain level of income and/or have access to an employer sponsored retirement plan (401k, 403b, 457b, etc., whether you use it or not) you lose the deductibility of your Traditional IRA contributions.  **IMPORTANT: Even if you can’t deduct IRA contributions, you can still make them.** New clients are often surprised when we tell them they’ve been missing out on these tax favorable IRA contributions. Many investors assume they can’t make IRA contributions because they make too much money or already participate and max out an employer 401k or 403b plan. In each case, you can make IRA contributions, you just can’t deduct them. Unlike Traditional IRAs, when you make contributions to a Roth IRA you pay the taxes now-- or have already paid taxes on the contributions via payroll and will simply not receive a tax deduction for the contribution. The magic of a Roth IRA is that once the assets are in the account and the account has been open for 5 years—all withdrawals of principal AND earnings are tax-free. And tax-free > tax-deferred. But high earners are not allowed to make direct Roth IRA contributions, because Roth IRAs have their own income level eligibility qualifications:  So-- if you’re single making more than $139,000 AGI or married and earn over $206,000 AGI you can’t make direct Roth IRA contributions AND you don’t get Traditional IRA contributions deducted. However, if you have little or no Traditional IRA assets to start with, we recommend executing a backdoor Roth contribution strategy. High earners can make non tax-deductible contributions to their Traditional IRAs, receiving no tax deduction for the contributions. Then they can immediately convert that contribution to their tax-free Roth IRA. Why would you want your investments growing tax-deferred when they could be growing tax-free? Not simple to do, but a no brainer…slam dunk. How are Backdoor Roth IRA Contributions Taxed? A key factor that must not be overlooked is the amount of previously tax-deferred Traditional IRA assets a high earner has while executing this strategy. It’s important because Roth conversions are taxed at the ratio of tax-deferred assets to after-tax, or non tax-deferred assets. For example, let’s say you’re a married high earner and want to start this backdoor Roth IRA strategy. You make the max Traditional IRA contributions of $12,000 ($6,000 each) for you and your spouse for 2020 and plan to immediately convert that to your Roth IRA to facilitate the lifetime tax-free growth mentioned above. At the same time, you already had $12,000 (again $6,000 each) of tax-deferred contributions from previous years where you qualified for the deduction. Or you could have rolled over tax-deferred assets from an old 401k into your Traditional IRA. Either way, half the assets in the Traditional IRAs were tax-deferred in prior years, and half are non-deductible from 2020’s contribution. If you convert the $12,000 of non-deferred contributions you made in 2020, it wouldn’t be a tax-free conversion— it would be taxed according to the Roth IRA pro-rata rule. This states you have to use the tax-deferred to non-tax-deferred ratio for taxing of the conversion assets. In this case the ratio is 50:50 ($12k tax-deferred to $12k tax-free), so half, or $6,000 of the $12,000 Roth IRA conversion would be taxed at your normal income tax rates for 2020. This is important-- because if you’re a high earner, you may want to avoid paying 32%+ Federal taxes this year on that $6,000 taxable portion of the Roth IRA conversion. It may be better to wait until retirement when you’ll likely be in a lower tax bracket, especially if you do some of the tax planning we mention in this article. The Roth IRA pro-rata rule should give pause to rolling over tax-deferred dollars from 401ks or 403bs into a Traditional/Rollover IRA when a backdoor Roth IRA strategy is recommended. The more assets added to your personal Traditional/Rollover IRA, the higher the taxable percentage of Roth IRA conversions. For these reasons, our financial advisors may recommend clients keep tax-deferred dollars in an old employer plan-- even if those plans have slightly elevated fees or lack diversified, cost-efficient investment offerings. We believe the tax-free savings of Roth IRA assets for a young high earner provide unmatched advantages in terms of investment returns and future tax planning strategies. Getting assets in a high earner’s Roth IRA early while avoiding unnecessary taxes at their currently high tax brackets provides great value to our clients. On the other hand, some clients prefer to fill up their brackets with Roth conversions to eventually get rid of all Traditional IRA tax-deferred assets, never having to worry about Roth conversion taxes again. Regardless—your taxable income level and tax bracket management must be thoroughly analyzed to make the right decision. Why Should I Build Roth IRA Assets?Saving on Pre-Medicare Health Insurance Premiums For example, let’s say a couple retires at age 60, with 5 years before Medicare eligibility. Our fee only advisors use taxable investment accounts and tax-free Roth IRA assets to strategically qualify millionaires for Premium Tax Credits under the Affordable Care Act that can offset some of the cost of healthcare insurance. Monthly private marketplace insurance premiums at age 60 are likely to be $1,000 per person—meaning if you and your spouse plan to retire at age 60, every year until age 65 you’ll fork over $24,000 alone on healthcare insurance premiums before you step foot in a doctor’s office. That can put a damper on early retirement plans. Our fiduciary advisors can situationally use taxable and Roth IRA assets to qualify even our most wealthy clients for Premium Tax Credits, which cover a portion or all of a family’s health insurance expenses. In the above example, that’s a potential savings of up to $120,000 in premiums from retirement at age 60 to Medicare eligibility at age 65—and a glaring reason everyone should invest in a financial plan. *Added Note: Recently, we’ve heard several current and prospective clients mention they’re going to beat high healthcare insurance costs during pre-Medicare retirement years with some sort of too-good-to-be-true Medi-Share plan. Please reconsider. These plans are not actually health insurance and leave your family’s wealth and health in jeopardy. One un-insured serious hospitalization could put your entire financial future needlessly at risk. Long Term Capital Gains Rates Saving  We also use taxable and tax-free assets to manage tax brackets via favorable capital gains rates, and in some cases, help our clients pay 0% on capital gains through complex tax planning strategies. For those high earners today, as tax laws are, as is, we’d be able to structure their taxable income so they can optimize favorable capital gains rates while ensuring their assets at 12% Federally. That’s a Federal tax savings of $22,000+ for every $100,000 in their IRA. Not a bad deal for someone being taxed at 24% or 34%+ today and may even pay the 3.8% Medicare investment income surcharge. Other Uses for Roth IRA Assets Tax-free income can help manage tax brackets/income in retirement and can lead to enormous tax savings if planned correctly. If you max out your employer retirement plans and are looking for even more tax diversification of your assets, a backdoor Roth IRA strategy is a good choice. There are many factors to analyze to ensure you realize the tax savings these strategies provide.

If you could use help determining the most appropriate course of action to take with your excess savings give us a call and get started with a financial plan today. There’s an old story in the investment industry that may be true or may be just a parable--but it certainly is appropriate to remember when the stock market is panicking. The story goes, a very smart advisor would tell each of the investors who opened an account with her the following:

But wait--

While that’s a good story, and one we tell often, it’s not the whole picture. If you wait for the perfect time to invest, you’ll likely miss many, many, days, weeks, months, or even years of good growth in the market. We believe a better answer to the “When is the perfect time to invest?” question is: “ASAP”. The magic of compound interest works best for you many years down the road. Every day you delay is a day you put off that magic coming to fruition. Not to get into the math, but you can imagine that 21 years of compounding growth produces a higher number than just 20 years of compound growth. If you take the time to do the math, you might be amazed at what one extra year of compounded growth means in dollar terms. And my answer of as soon as possible also comes with some conditions. Get a financial plan. Developing a real financial plan means understanding all, or at least most of, the risks equity investing presents. Knowing the correct asset allocation is paramount. Too little risk and you may have no chance of reaching your goals, too much risk and you’ll find yourself outside our window with a rock in your hand. Having a real financial plan gives you discipline, and in investing, discipline is your friend. A real financial plan gives you confidence that no matter what happens in the short-term, you will be okay in the end. A real financial plan makes life simpler. If you find yourself with extra money to add to your portfolio, you don’t have to reinvent the wheel or come up with some new idea. Your plan already shows you where your money should go. If stocks soar, your plan will tell you when to pull back; if stocks sink, your plan will force you to make the hard decision of “should I buy more”. A real financial plan provides a more tax-efficiency investment strategy, which gets you where you want to be faster-- and with less risk. Investing with poor tax planning is like driving your car with the parking brake on-- it slows you down and ruins your car. If you don’t have a plan, it’s unlikely you have done an adequate job of educating yourself about how markets and money work either. Folks often fail when they follow a “get a hunch, bet a bunch” strategy. Sure, you hear stories of someone who bet all their money on some company you have never heard of and made a fortune. You have also heard stories of folks who won the lottery and became rich overnight; that doesn’t make buying lottery tickets a sound investment strategy. So, while I love the story about the brick, I think it misses the bigger picture. Planning, and executing your plan, will create the perfect time to invest. Remember, it wasn’t raining when Noah built the Ark. This is being written as the bill is still in progress. Edits may be required as more information becomes available. Please check back for updates and be sure to consult a financial professional before implementing any of the strategies suggested in this post. The Senate has passed an emergency relief bill that is expected to pass the House later this week. The package is over $2 trillion in scope, $6 trillion if you include loan provisions, and is the largest relief bill in the history of the United States. Relief Payments Made Directly to TaxpayersLet’s start with the direct payment checks you have probably heard about. In general, individuals will receive payments of $1,200 and joint filers $2,400, plus $500 for each qualifying child. The definition of a qualifying child is already in the current Child Tax Credit Guidelines i.e. if you claim someone as a dependent child on your tax return in 2020 then they’ll qualify for the additional $500 per child payment. High income taxpayers will see these amount reduced as income exceeds $150,000 for joint filers, $112,500 for head of household, and $75,000 for single filers. For every $100 over those limits the payment is reduced by $5 until you reach zero. That means joint filers earning $198,000 or more, heads of households earning $136,500 or more and single filers earning $99,000 or more will receive nothing. The payments will be based on the most recent tax return filed. So, if you have already filed for 2019 you are stuck with those earnings. If you have not filed for 2019, then your payment will be based on 2018 return information. If your income is higher in 2019 than 2018 DO NOT FILE YOUR TAXES UNTIL LATER. On the other hand, if your 2019 income is lower than 2018 IT IS IMPORTANT TO FILE YOUR TAXES NOW. The payments will be direct deposited for taxpayers who elected to have direct deposit on their income tax forms. This could be a problem if the direct deposit instructions you provided in 2018 are to an account that has since been closed, or if you have divorced or separated since your 2018 tax filing. Within 15 days of the money being released, the IRS will send a letter informing you of the amount and where it was sent. If there is an issue with your payment, like it never arrived or went to a divorced spouse, the letter will include a phone number where you can call to resolve the issue, but unfortunately, the IRS is difficult to communicate with in general. Required Minimum Distributions from IRA Accounts SuspendedFor the tax year 2020, there are no required minimum distributions (RMDS) from IRA accounts. If you have already withdrawn your RMDs for 2020, you cannot undo that. If you haven't taken your RMD yet, consider how delaying or withdrawing your RMD will affect your income tax brackets. For inherited IRA accounts required withdrawals are also eliminated for the 2020 tax year. Corona Virus Distributions from Qualified Retirement PlansDistributions of up to $100,000 from any IRA, 401k, 403b, or other qualified plan will not be subject to the usual 10% early withdrawal penalty for those who are infected with the COVID virus, have a family member infected by the virus, or were laid off or lost wages due to the virus. The distribution is still taxable, but the income, by default, will be spread over a 3-year period. This can help you access funds without bumping yourself into a much higher income tax bracket. It could potentially be used to advance fund Roth IRA conversions. More on that as we have time to digest all the ins and outs of the legislation. The law also allows for repayment of any qualified plan distributions over a 3-year period as a qualified rollover contribution. So, if you need the funds now and are re-employed later, you will be able to replace the funds, offsetting any potential tax bracket increase in the future. Allowable loans from qualified plans, such as a 401ks, are also increased to $100,000 or 100% of the vested account balance, whichever is lower. Repayment of any loan taken in 2020 can be delayed for up to one year. Charitable Contribution DeductionAfter the recent Tax Cuts and Jobs Act (TCJA), many taxpayers found themselves using the increased standard deduction and no longer itemizing on their income tax return. That eliminated the charitable contribution deduction. One of the permanent changes the relief bill provides is a new above the line deduction for up to $300 of cash contributions to a qualified charity. This does not include contributions to donor advised funds. *Again, this is a preliminary look at the relief bill, we will provide updates and corrections as new information becomes available

I don't want to add flames to the fire regarding the new coronavirus-- COVID-19, however, the time to have a lifeboat drill is prior to the ship sinking. Investors should contemplate what this virus can do to the markets and world economies while they are still thinking rationally, rather than waiting until widespread panic clouds their judgement. The COVID-19 is the same type of virus as the common cold, but it’s definitely not common. It is a strain that is new in humans, so we, as a species, have not developed antibodies to fight it, and there is no herd immunity to slow its contagion. Rather than turn to Facebook or the popular press for answers, we recommend you visit the Center for Disease Control web site for more detailed information on what COVID-19 is and the threat it poses. Early data shows a high fatality rate-- somewhere around 2%; but keep in mind this data could well be skewed because diagnosing those infected is rudimentary at best. We are aware of nearly 100% of the fatalities but the number of cases of infection could be vastly under-reported. A coronavirus is a cold, and except in the most serious cases, likely to pass with little notice. You’re probably aware that drug companies around the world are trying to find a vaccine. We wouldn’t hold out much hope on this front as we have been trying to find a cure for the common cold for decades with zero success. In the past week, we’ve seen the US Stock market drop by about 10% as concerns over COVID-19 have swept the globe. While markets usually do a very good job of pricing risk and opportunity, there are times when rationality tips to panic, and markets no longer function as they should. The most recent example of this was the 2008-2009 period when markets lost half of their value based on panic that the world was ending. They would eventually rebound fourfold as panic subsided and rational thought came back to the forefront. So, is the pullback, so far, a rational repricing of risk/opportunity? Or is it the beginning of a panic? We believe it is too soon to tell. Some companies have already announced that the COVID-19 is having an effect on their sales and earnings. Microsoft and Apple have noted problems with their supply chains. As market participants try to peer into the future, they’ve battered the travel and energy sectors, expecting consumers to avoid travel. As fear spreads this will work its way into the restaurant sector, fear of contagion may cause consumers to avoid crowded spaces where the virus could be easily transmitted. On a more basic level missed workdays and a drop in productivity could potentially hurt businesses of every type. S&P 500 2010-Present The stock market has had an incredible run over the past 14 months, reaching new highs at almost a monthly pace. The technical indicators we follow showed the market nearing overbought levels on a short-term basis prior to the recent drop. So, a pullback was not unexpected-- with or without the COVID-19 outbreak. That doesn’t mean we expect a reversal, but it does mean we would not expect a continuation of these 2%-3% per-day drops. From a technical perspective, a pullback to around 2,600 for the S&P 500 would not be overly concerning. If markets stabilize on a short-term basis, there are gaps in index price levels that will be filled. So, in fact, we could soon have a very good buying opportunity for long-term investors with cash to allocate to stocks. S&P 500 Last 6 Months What Should a Rational Investor Do?Nothing. Rational investors know that their default position should always be to remain fully invested. It is too soon to tell if this is a normal market adjustment to new information, or the beginning of a panic. For those with reasonable investment time frames, this will be a barely noticeable blip on the long-term chart of their investment history.

In the short term there will be times when investors doubt themselves. This is normal. We believe thinking about this problem now and preparing for an uncertain future can only help long-term investors achieve their long-term goals. What's the Problem?IRAs that will be inherited by anyone except a spouse, minor children, beneficiaries with disabilities, and anyone who is ten years or less younger than the IRA owner, are now to be completely distributed over 10 years, rather than the lifetime of the heir. Why is this a Problem?With a shortened time span to distribute inherited IRAs, taxable income generated from an inherited IRA, in addition to one’s normal earned income, can cause uncharacteristically high tax bills if appropriate tax planning is not executed. In larger inherited IRAs, tens of thousands of tax dollars are at stake. What are some Solutions to the SECURE Act?

Tax Planning for the SECURE ActWith the passage of the SECURE Act, stretch IRAs became a thing of the past. Rather than allowing beneficiaries to withdraw funds based on their life expectancy, the Act requires IRA beneficiaries to make a total distribution of all funds from the IRA within 10 years, with limited exceptions for spouses, minor children, beneficiaries with disabilities, and anyone who is ten years or less younger than the IRA owner. Congress passed the Act knowing the net effect would be higher income taxes to most IRA beneficiaries. According to the Congressional Research Service, the elimination of the stretch IRA alone has the potential to generate about $15.7 billion in tax revenue over the next decade. For many beneficiaries, the inherited IRA will come during their peak earnings years when their income tax rate could be at a maximum. The effect of high earnings and additional taxable distributions from a Beneficiary IRA could cause the net value of the IRA to be reduced by 30% or more. To minimize to tax bite of an IRA inheritance, both the original IRA owner and the beneficiary will need to do diligent tax planning. How IRA Owners can Minimize Taxes from the SECURE ActRoth IRA Conversions Now, more than ever, converting Traditional IRAs to Roth IRAs should be examined. We strongly believe almost everyone should convert enough funds from a Traditional IRA to a Roth IRA to fill the 12% income tax bracket each year. 12% is a fair tax rate for most taxpayers and it’s much easier to implement effective tax planning for inherited Roth IRAs than for inherited Traditional IRAs. Having assets in a Roth IRA has advantages for the original IRA owner as well. It will reduce the amount of required minimum distributions (RMDs) when you reach age 72 (up from 70 ½, a positive from the SECURE Act), as well as provide more flexibility in managing your income-tax rate in retirement. For a free Roth conversion flow chart that will help you understand how a Roth conversion can work for you click here. While we usually don’t recommend going beyond the 12% bracket for Roth conversions, there could be certain circumstances where that might be appropriate. For example, if you don’t need the assets in your Traditional IRA for your retirement lifestyle and all of your heirs are high wage earners, it might be better for you to pay a 22% tax rate now rather than leaving the IRA to an heir who may be taxed 32-40% on those same assets. Naming Grandchildren as Partial IRA Beneficiaries If you have grandchildren, including them as partial beneficiaries of your IRA can potentially increase the net value of an inherited IRA. For example, suppose you have a $500,000 IRA, two children, and four minor grandchildren. Both children and their spouses work and earn $150,000 per year in combined taxable income, so under current income tax law that puts them in the 22% marginal Federal income tax bracket. With a Beneficiary IRA of $250,000 each, if they take equal distributions from their Beneficiary IRA of $25,000 per year for 10 years, they will be pushed into the 24% bracket and thus nearly every dollar distributed from the Beneficiary IRA is taxed at the 24% level. Or worse, say they wait to take the full $250,000 distributions in year 10 or another single year—they would jump into the 32% Federal tax bracket. To steer some IRA assets away from being taxed at those higher tax brackets you could earmark a portion of the IRA to go to each grandchild. Under current rules, any minor can have $1,100/year of unearned income with no income tax liability. This kiddie tax rate applies to children under the age of 19 and college students under the age of 24. Every year $1,100 is distributed from your grandchild’s inherited IRA tax-free, resulting in a savings of $242 each year the child qualifies. If the child has earned income during their teen years, the distributions can be increased to fund a Traditional IRA or Roth IRA for the child’s benefit. Smart tax-planning could combine Traditional and Roth IRA contributions to eliminate all taxes on the child’s earnings. Once the child reaches the age of majority, the ten-year rule begins. It is unlikely the grandchild’s earnings will place them in a top bracket fresh out of school, so the strategy of offsetting distributions with tax-deferred savings could allow your grandchild to build a nice retirement nest egg without much loss to income taxes. To accomplish this, you must be sure to name a custodian for the minor grandchildren since minors cannot make financial decisions for themselves. The custodian could be a parent, but one must be named. Another important factor in determining the dollar amount that should be allocated to a grandchild is the age of the grandchild when they receive the Beneficiary IRA. Most IRA owners will name a spouse as a primary beneficiary and that is perfectly fine. Spouses are exempt from the ten-year distribution rules. Children are generally named as contingent beneficiaries, in some equitable percentage of the account value. Most custodians only allow for simple percentage distributions to be named beneficiaries and that could create some problems. For complex beneficiary strategies, using a pass-through trust might be a better solution. Using Pass-Through Trusts Correctly If you’ve already established a trust as the beneficiary of your IRA, it is imperative that you review and update that trust. Most trusts have language that instructs the trustee to pay out the required minimum distribution (RMD) to the beneficiary each year. Under the SECURE Act, there are no annual RMDs until the end of the 10-year term, then the required distribution is 100% of the account value. This is a tax time bomb just waiting to explode. At a minimum, you must rewrite the trust to allow flexibility for distributions, which also provide flexibility for income tax planning for the beneficiary(ies) of your IRA. Realizing a $500,000 Beneficiary IRA distribution through a trust in one single year will likely subject the distribution to the maximum income tax rate of 37%, plus a 3.8% Medicare surtax on some of the recipient’s income. This is just for the Federal level taxes; add in state income taxes and the beneficiary may only end up with 50% of the original account value-- certainly not what you had in mind when you drew up the trust. Most IRA custodians do not allow for complex IRA beneficiary schemes, so the ability of pass-through trusts to manage distributions to multiple generations becomes much more important. Through a trust you can establish custodians for minor beneficiaries, name an investment and income tax counselor, and provide for flexibility in the timing of distributions during the 10-year window allowed under the SECURE Act, or even longer in the case of minor children. Although establishing the trust incurs more expense and investment of time and thought, the result can certainly provide enough benefit to owners of substantial IRA assets and their families to make it worthwhile. How Beneficiaries Can Reduce Taxes from an Inherited IRAOff-Setting Distributions with Tax-Deductible SavingsFor many Beneficiary IRA owners, the biggest tax planning opportunity will be to simply manage the distributions over the 10-year period. One strategy would be to offset the taxable Beneficiary IRA distributions with additional tax-deferred savings. To do this, simply increase savings to an employer’s retirement plan such as a 401k, 403b, or other tax-deferred plan, or establish and contribute to a separate deductible Traditional IRA or self-employed retirement plan of your own. Any form of tax-deductible contribution will reduce the impact on income realized from one’s Beneficiary IRA dollar-for-dollar. Let’s go back to our previous example with the $500,000 IRA. If the IRA owner’s children in this illustration are like most investors, they only contribute about 5% of their salaries to an employee retirement plan in order to maximize the company matching formula-- a.k.a get the free money. This means the parents are likely contributing much less than the $19,500 maximum salary deferral allowed by the IRS. Let’s assume the decedent’s children can defer an additional $15,000 for each spouse in their employer 401k plans. If they defer the additional $30,000 in one year, they can distribute another $30,000 from their Beneficiary IRA(s). This results in a wash for $30,000 of distributions from the Beneficiary IRA as it would swap funds from one tax-deferred account to another and fulfill the original IRA owner’s estate planning intent. Inherited Roth IRAsWhile inherited Roth IRAs are easier to manage from an income tax perspective, you should put some thought into the options. The most obvious option is to do nothing until the final day of the ten-year withdrawal period and then take a distribution of the entire account. This maximizes the tax-free growth of the inherited Roth IRA and because the distribution is tax free, has no effect on the recipient’s tax rate. If the beneficiary is not making maximum retirement plan contributions when they inherit the Roth IRA, taking distributions along the way and using those funds to fund their own Roth IRA, or even better-- make contributions to a Roth 401k-- could mean you really do get to stretch the inherited Roth IRA over your lifetime. Non-deductible 401k contributions, up to the annual $19,500 limit, will work as well. When you retire, the non-deductible contributions, but not the earnings, can be rolled over into your own Roth IRA. Taking money from one pocket and moving it to the other pocket, that has no hole in it, (i.e. tax-free) makes a lot of sense. The Role of Your Financial Planner The SECURE Act makes working with a financial planner more important than ever before. Earning an 8% or even 10% return on your investments pales in comparison to shielding 30% or more of your assets from the ravages of our income tax system. To get started on a plan to preserve your IRA assets, click HERE.

With the end of the year approaching, now is the time to look for opportunities to save on income taxes. Here are some items you should look for:

|

Archives

September 2023

Categories

All

|

RSS Feed

RSS Feed